Meta announced the launch of the Quest 3 headset on June 1. To be retailed at just under $500, it will be released in autumn. The Quest 3 will have both VR and MR capabilities.

The Quest 2 has also received a $100 price cut, with the entry-level variant available at $299 starting June 4.

Together with its newly discounted predecessor, the Quest 3 is expected to help the company maintain market dominance for now.

Meta’s announcement came days ahead of WWDC, where Apple will reportedly announce its own MR headset.

London, San Diego, New Delhi, Beijing, Buenos Aires, Seoul, Hong Kong – June 5, 2023

The announcement of Meta’s Quest 3 headset at $499.99 and the Quest 2’s $100 price cut to $299 just before the rumoured launch of Apple’s first mixed reality (MR) headset shows the social media parent’s determination to lead the extended reality (XR) headset market.

Meta described the Quest 3, which will have both VR and MR capabilities, as its “most powerful headset yet”. The announcement of a successor to the best-selling XR model in history after three years of no consumer-grade headset launches by Meta is an important step forward for the company as well as for the industry.

In line with the season’s flavour, mixed reality, the Quest 3 features the next generation of Qualcomm’s Snapdragon chipset and yet to be disclosed but likely superior display resolution, memory, battery life and weight.

The Quest 3’s launch in autumn, together with the price cut of the Quest 2, will be enough to maintain Meta’s market dominance in terms of shipments for the foreseeable future.

Apple’s expected announcement of a $3,000 MR headset during this year’s Worldwide Developers Conference (WWDC) on June 5 will create the biggest challenge to Meta since its entry into the segment through the acquisition of Oculus VR in 2014. If Apple succeeds in bringing the cost down and gaining a foothold in the market through successive iterations of the $3,000 headset, it may supplant Meta as the biggest revenue generator in the market which Meta has dominated thus far both in terms of revenue and shipments.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Feel free to reach us at press@counterpointresearch.com for questions regarding our latest research and insights.

In Q1 2023, China’s smartwatch shipments declined both YoY and QoQ.

HLOS* smartwatches’ share increased when compared to that in 2022.

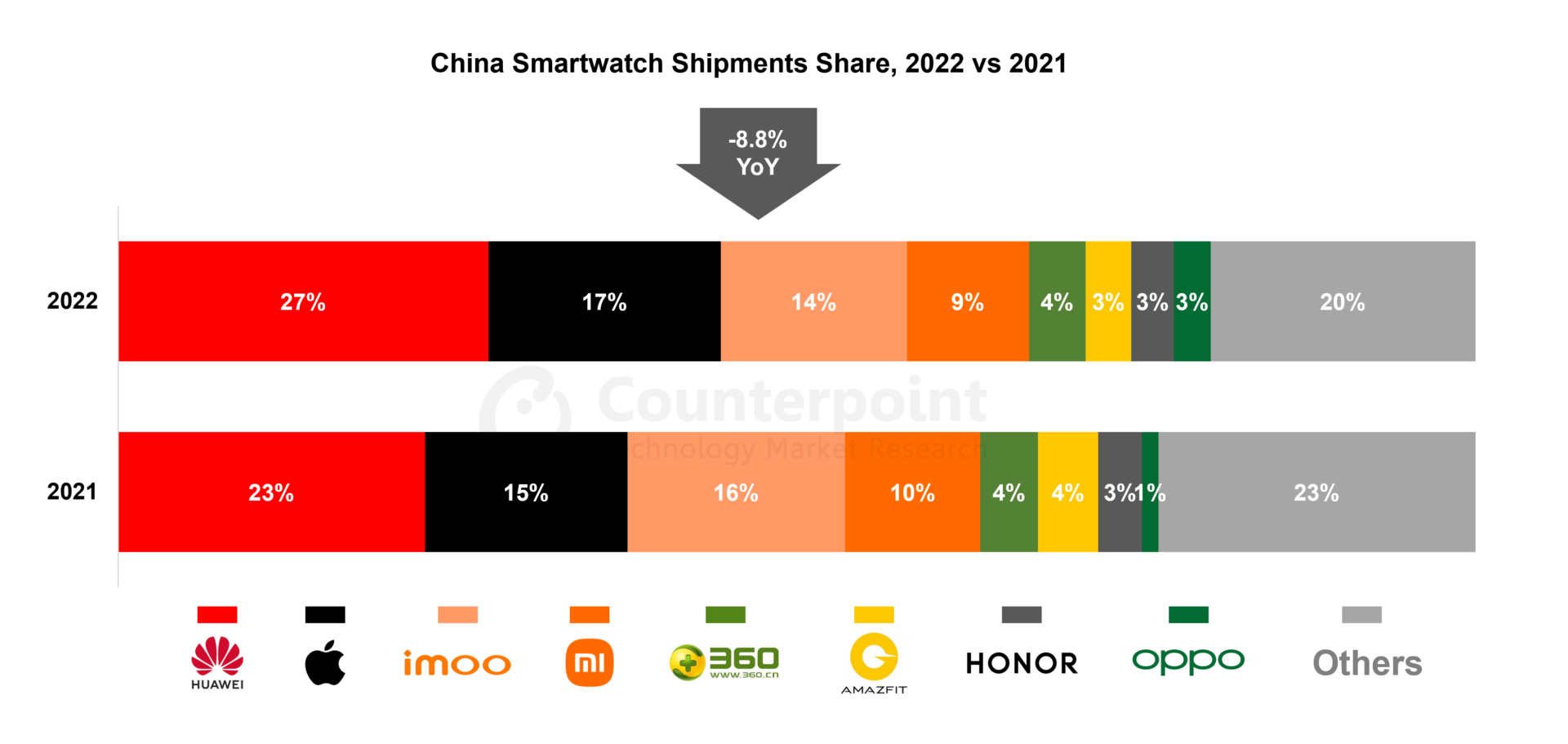

Despite its shipments falling 15% YoY, Huawei ranked first in Q1 with more than a quarter of the market share.

Apple’s Watch Series 8 was the best-selling model in Q1 even as the brand’s shipments fell 27% YoY.

Beijing, New Delhi, Seoul, Hong Kong, London, Buenos Aires, San Diego – May 30, 2023

China’s smartwatch market did not fully recover in the first full quarter after the country’s reopening. According to Counterpoint Research’s latest Global Smartwatch Model Tracker, China’s smartwatch shipments declined 28% YoY and 16% QoQ in Q1 2023 to reach their lowest level in 12 quarters.

Senior Analyst Shenghao Bai said, “Although the Spring Festival can boost consumption generally, the demand for smartwatches was still weak in Q1 2023. This was similar to what we saw in China’s smartphone shipments. The market needs more time to recover.”

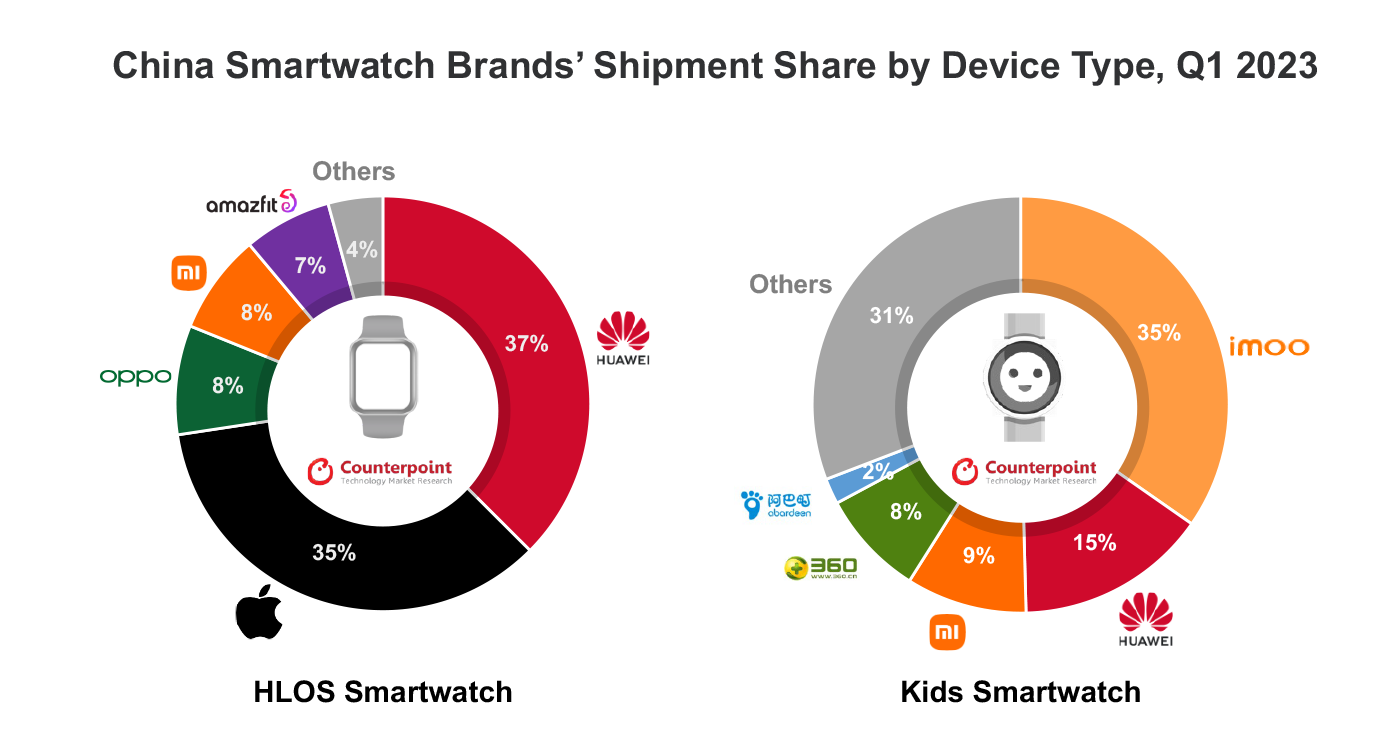

The top three brands were Huawei, Apple and BBK (imoo). They accounted for nearly 60% of China’s smartwatch market in Q1 2023. Among the types of smartwatches, the HLOS* smartwatch’s shipments saw the smallest YoY drop even as its share increased to 45% from 39% in Q1 2022. Meanwhile, China’s ‘kids smartwatch’ shipments decreased 31% YoY. The country is the world’s biggest kids smartwatch market.

Chart-China-Smartwatch-Q1-2023

Source: Counterpoint’s Global Smartwatch Model Tracker

Note: Figures may not add up to 100% due to rounding

Commenting on the market trends, Research Associate Alicia Gong said, “Despite the overall demand for smartwatches dropping in Q1, the demand share for HLOS smartwatches rose. These are advanced watches offering users more customization and independence. Though BBK (imoo) still dominated the kids smartwatch market with a 35% share, its shipments of the watch remained flat YoY amid a shrinking kids segment.”

Market summary

Huawei was the biggest winner in China’s smartwatch market with a 27% share, thanks to its strategy of having multiple portfolios. Though the brand’s overall shipments dropped 15% YoY, it ranked first in all price bands from $101 to $400. The Huawei Watch GT 3 was the second best-selling model in Q1 2023.

Apple took the second largest share, mainly driven by its Apple Watch Series 8 and Apple Watch SE 2022. The two models were the first and third best-selling models in Q1 2023. However, Apple’s shipments decreased 27% YoY due to shrinking demand. Focusing on HLOS smartwatches helped the brand take an 87% share in the above-$400 segments.

BBK (imoo)’s Q1 shipments were generally flat YoY thanks to the back-to-school season. The brand benefited from its multiple-models strategy. Its Z6A series contributed the most to its shipments.

Xiaomi’s shipments saw a 42% YoY drop but a 31% QoQ increase in Q1 2023. The brand ranked first in the <$50 segment.

OPPO was the only one among the main brands to see its shipments increase both YoY and QoQ. The performance was driven by the OPPO Watch 3 and OPPO Watch 3 Pro. OPPO’s market share increased to 4% in Q1.

Qihoo 360 recorded a 35% YoY drop. It had fewer models on sale compared to Q1 2022.

Amazfit has a variety of models in China but lags behind in having popular models. The brand’s shipments declined 34% YoY in Q1 2023.

*HLOS smartwatch: Electronic watch running a high-level OS, such as Watch OS (Apple) or Wear OS (Samsung), with the ability to install third-party apps.

*All the prices mentioned in the article are wholesale prices.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

The global smartwatch market continued to contract in Q1 2023 following an 8% YoY decline in Q4 2022.

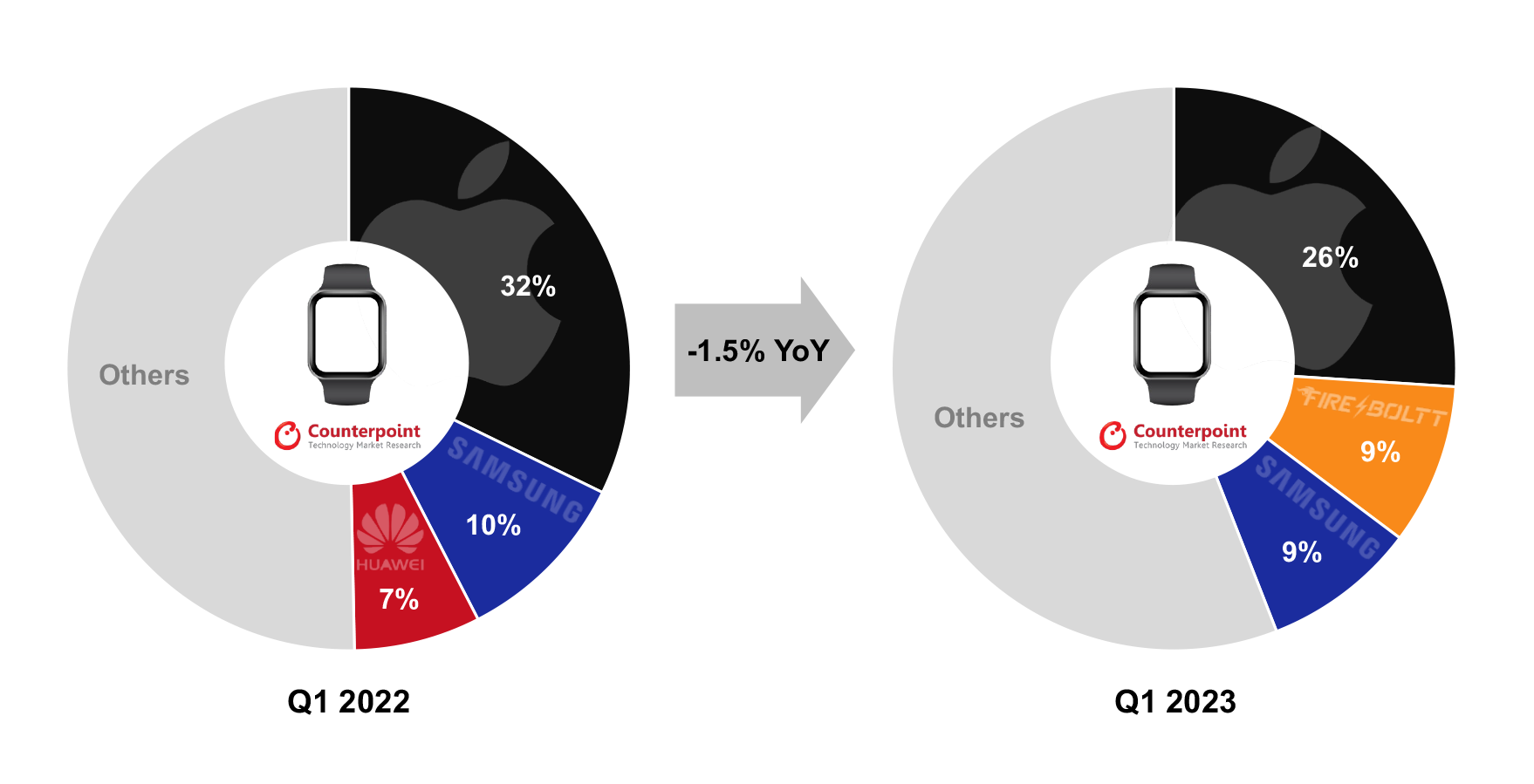

Fire-Boltt surpassed Samsung for the first time in the global smartwatch market, capturing the second spot.

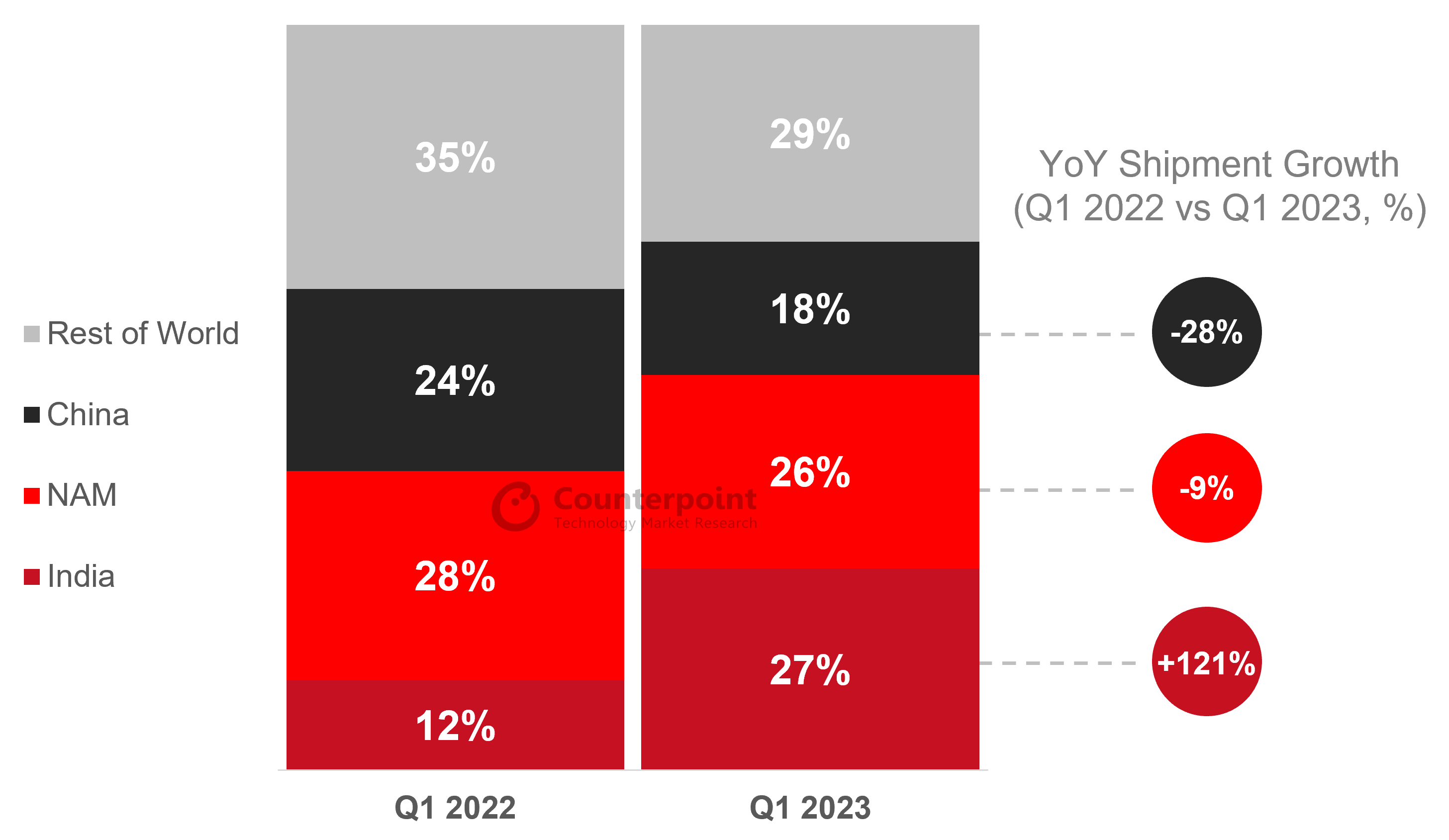

All regions except India witnessed a YoY decline in shipments in Q1 2023.

Seoul, New Delhi, Hong Kong, Beijing, London, Buenos Aires, San Diego – May 25, 2023

Global smartwatch shipments contracted 1.5% YoY in Q1 2023, according to Counterpoint Research’s latest Global Smartwatch Model Tracker. The 121% growth in India’s shipments managed to restrict the decline. This was the second consecutive quarter of a YoY decrease in global shipments, which were hit by the seasonal decline in demand for products from major players like Apple and Samsung, along with consumer sentiment dampened by global financial pressures.

Research Analyst Woojin Son said, “The global smartwatch market, which had been experiencing steep growth for several years, has entered a period of stagnation since the end of last year when it declined 8% YoY in Q4 2022. Amid a global slowdown in demand for tech devices, the smartwatch consumption trend has also undergone a transformation. The market share of high-price and high-performance HLOS smartwatches*, primarily released by Apple and Samsung, decreased from 60% in Q1 2022 to 53% in Q1 2023. On the other hand, the market share of Basic smartwatches* significantly increased from 23% to 34% driven by rapid growth in the Indian market. Although the overall smartwatch shipment volume declined slightly compared to last year, affordable products that offer a certain level of performance generated substantial demand based on their price accessibility. These low-end smartwatches are also absorbing or replacing the existing smartband market.”

Global Top 3 Smartwatch Brands’ Shipment Share, Q1 2023 vs Q1 2022

Source: Counterpoint Global Smartwatch Model Shipment & Revenue Tracker, Q1 2023

Market summary

Apple’s shipment volume fell 20% YoY in Q1 2023. This was the first time in three years that its Q1 shipments fell below 10 million units. As a result, Apple’s market share, which was 32% in Q1 2022, dropped to 26%. This can be attributed to the ongoing macroeconomic crisis, which has led to decreased accessibility to relatively higher-priced Apple Watches. Despite the Apple Watch Series 8’s release about a month ahead of its predecessor, it did not achieve the same level of success as the previous model.

Indian brand Fire-Boltt surpassed Samsung for the first time and reached the second position in the global market. Its shipments increased by approximately three times compared to the previous year and saw a 57% growth compared to the previous quarter. This reflects the rapid growth of the Indian market, just like other local brands such as Noise and boAt.

While Samsung experienced a 15% increase in shipments in its key market North America, it witnessed a decline in shipments in other major markets. As a result, its overall global shipments declined by 15% compared to the previous year and 21% compared to the previous quarter.

Huawei, the most influential Chinese OEM, saw a 14% YoY decline in its shipments in the Chinese market, which is a key market for the company. However, Huawei saw increased shipments in India, LATAM and MEA, limiting its overall decline in global shipments to 9%. Huawei has been employing a strategy of relaunching models previously released for the Chinese market in the international market.

Smartwatch Shipment Share by Region, Q1 2023 vs Q1 2022

Note: Figures may not add up to 100% due to rounding

Source: Counterpoint Global Smartwatch Model Tracker, Q1 2023

In terms of the regional markets, India surpassed North America, reclaiming its position as the top region with a 27% share of global smartwatch shipments. Senior Analyst Anshika Jain said, “India’s smartwatch market grew 121% YoY in Q1 2023 driven by affordability, rising customer demand and availability of a wide variety of options in the budget segment. Around 40% of the total shipments were driven by the <INR 2,000 (<$25) price band, its highest proportion ever. The share of India-based players crossed 90% for the first time as they were quick in terms of upgrading their portfolios and adapting their products to customer needs at a reasonable price point.”

China’s smartwatch market experienced a significant contraction of 28% compared to the previous year, as the country’s economy showed a slower recovery than expected. This decline represents the sharpest contraction among the major regional markets and the lowest quarterly shipments since the outbreak of COVID-19 in Q1 2020.

*Types of smartwatches:

HLOS smartwatch: Electronic watch running a high-level OS, such as Watch OS (Apple) or Wear OS (Samsung), with the ability to install third-party apps.

Basic smartwatch: Electronic watch running a lighter version of an OS, with no ability to install third-party apps.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

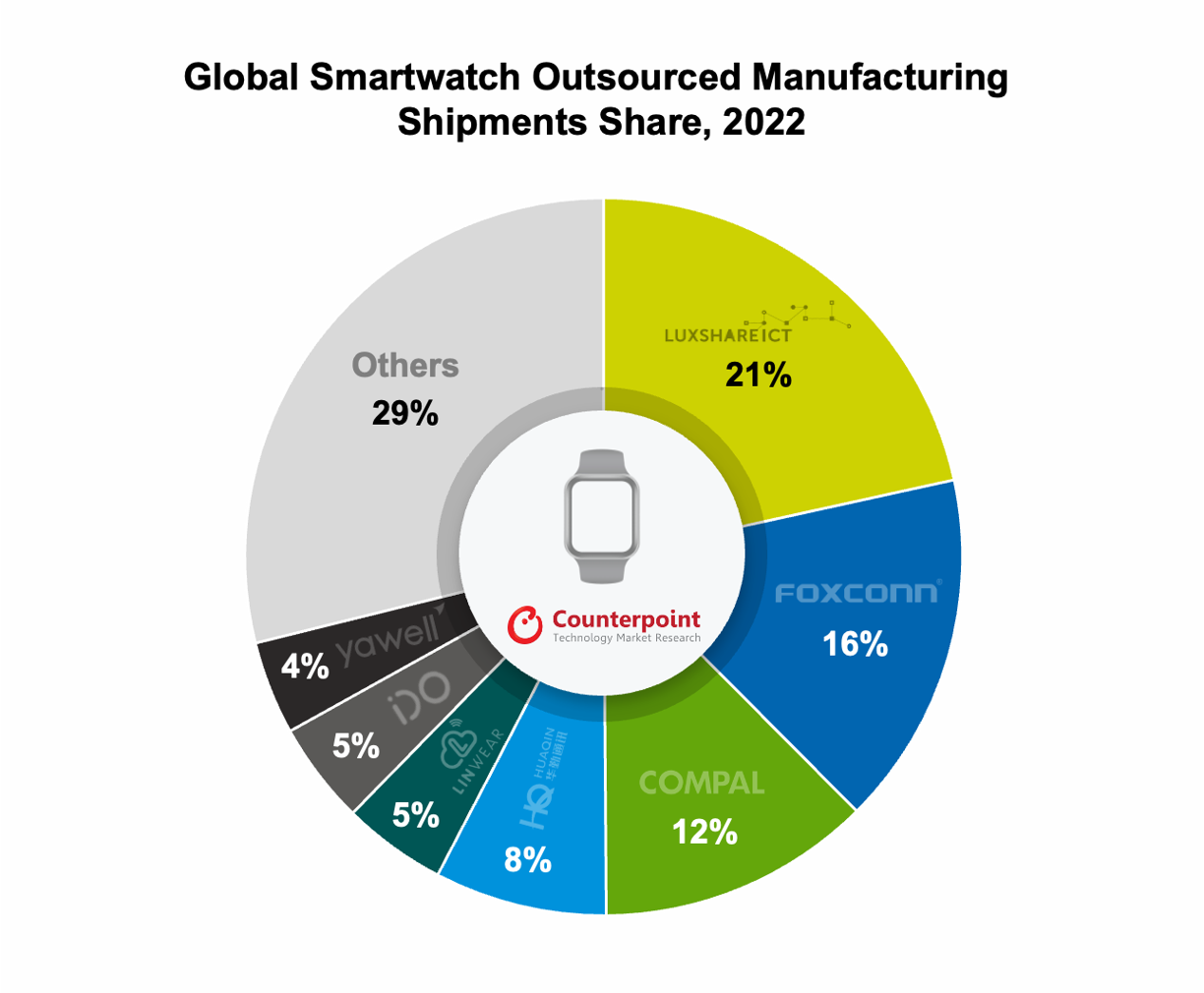

Luxshare was the top outsourced smartwatch manufacturer in H2 2022 as it undertook around 40% of Apple Watch production.

In Tier-2, Huaqin ranked first as it produced smartwatches from a variety of brands. Meanwhile, LINWEAR, I DO and Yawell benefitted from the stellar growth of Indian brands.

The share of outsourced manufacturing shipments is expected to continue to grow as the global smartwatch market expands.

Beijing, New Delhi, Hong Kong, Taipei, Seoul,San Diego, Buenos Aires, London – May. 2023

Senior Research Analyst Shenghao Bai said, “The YoY increase in outsourced smartwatch shipments in H2 2022 was driven by the strong performance of Indian brands Noise, Fire-Boltt and boAt. The outsourced manufacturers who offered production services for these brands benefited in H2 2022.”

Bai added, “As global smartwatch shipments continue to grow, the contribution of outsourced manufacturing sources has also increased. 69% of global smartwatches were produced by ODM/EMS in H2 2022, compared with 63% in H2 2021.”

Luxshare, Foxconn and COMPAL were the top three outsourced manufacturers in H2 2022. The three players were responsible for half of the global smartwatch outsourced shipments during the period. Luxshare ranked first in H2 2022 as it undertook around 40% of Apple Watch orders. Among Tier-2 players, Huaqin, LINWEAR, I DO and Yawell displayed strong performances in their smartwatch production businesses.

Source: Counterpoint Global Smartwatch Outsourced Manufacturing Tracker, H2 2022

Commenting on the performance of the leading players, Senior Research Analyst Ivan Lam said, “The top three manufacturers mainly benefited from Apple Watch orders in H2 2022. Luxshare’s smartwatch shipments were flat compared with that in H2 2021. Foxconn’s shipments in H2 2022 rose due to the orders from Apple, helping the company rank second in terms of shipments. Meanwhile, COMPAL reduced orders from Apple in pursuit of a higher profit margin.”

Lam further added, “In Tier 2, Huaqin’s shipments increased slightly following the company’s partnership with Samsung. Huaqin also continued its cooperation with Huawei, HONOR and OPPO. Manufacturers like LINWEAR, I DO and Yawell increased their shipments by cooperating with multiple brands, especially those from India which mainly focus on the <$50 segment. Yawell received a large share of orders from Noise and Fire-Boltt in Q3 2022.”

ODMs and EMSs have started playing more important roles in the smartwatch industrial chain as the global smartwatch market continues to grow. The share of shipments from outsourced manufacturers is expected to rise to about 70% in 2023 from 68% in 2022 all year. Commenting on the trend, Bai said, “The competition is getting tighter as well. There are increasing requirements for OEMs to be mindful of cost, deliverability and reliability.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

China’s smartwatch shipments declined 8.8% YoY in 2022,mainly due to the COVID-zero policy’s impact on consumption. The global shipments grew 9.0% YoY during the same period.

Huawei and Apple dominated the China smartwatch market in 2022, raising their combined share to almost 50%.

Growth in the high-to-premium segment (>$200) was driven by increasing consumer demand for premium features like health monitoring and professional sports guidance.

The top three best-selling models were the Huawei Children Watch 4 Pro, BBK Q1A and BBK Z6A.

Beijing, New Delhi,London, San Diego, Buenos Aires, Hong Kong, Seoul – March 23, 2023

China’s smartwatch shipments fell 8.8% YoY in 2022, mainly due to the COVID-zero policy’s impact on demand, according to Counterpoint Research’s latest Global Smartwatch Model Tracker. The year saw the country’s smartwatch market size shrinking to pre-COVID levels, with only Q1 2022 registering a quarterly YoY growth in shipments. The global smartwatch shipments grew 9% YoY during the same period.

Huawei and Apple dominated the China smartwatch market in 2022, with their combined share rising to almost 50%. Only OPPO (105% YoY), Apple (4% YoY) and Huawei (9% YoY) grew YoY among key brands.

Source: Counterpoint Global Smartwatch Model Shipments & Revenue Tracker

Note: Figures may not add up to 100% due to rounding

Senior Analyst Shenghao Bai said, “China’s strict anti-COVID policies impacted consumer sentiment in 2022. Curbs on movement and remote education regulations further impacted the demand for kids’ smartwatches in the country, the world’s biggest kids’ smartwatch market, and their shipments fell 25% YoY. From key brands’ perspective, only Huawei, Apple and OPPO achieved YoY growth, driven by the success of their new launches.”

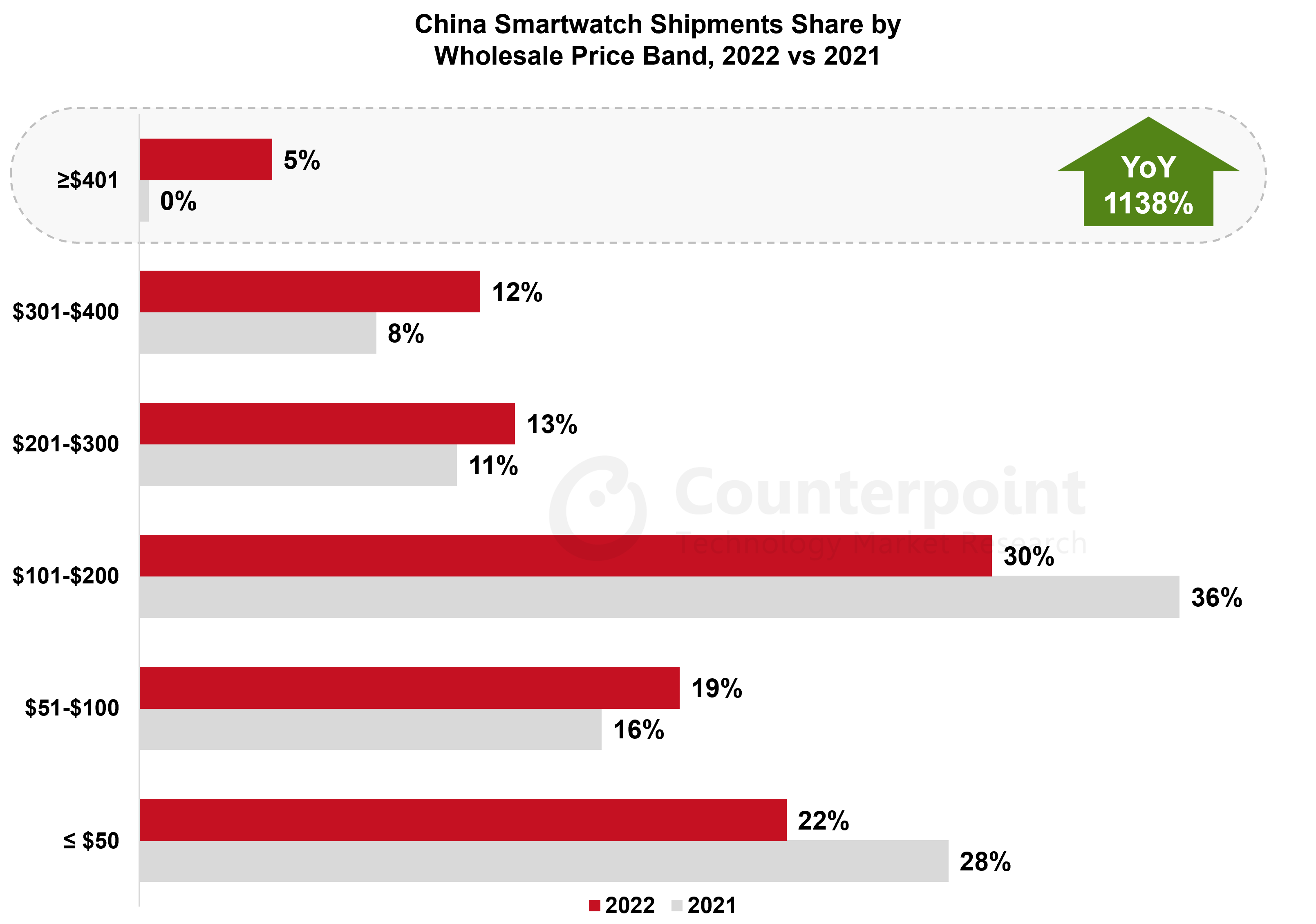

The biggest standout feature of the year was the high-to-premium segments’ (>$200) share rise. Shipments in the $301-$400 segment grew 31% YoY, while shipments in the ≥$401 segment grew a whopping 1138% YoY. The ≤$50 segment’s share dropped to 22%, with a 28% YoY decrease in shipments compared to the previous year.

Source: Counterpoint Global Smartwatch Model Shipments & Revenue Tracker

Senior Analyst Ivan Lam said, “The demand for high-end and premium segments remained relatively strong in 2022, despite the decline in consumer sentiment and global macro headwinds. This shift to the high-end segment is similar to the shift witnessed in the smartphone market in 2022. High-end smartwatch consumers usually have higher demands for health detection, communication and system features. Such consumers are also more loyal to the brand. In recent years, Apple and Huawei’s marketing efforts have led high-end consumers to view their smartwatches as professional-grade devices with advanced sports and health monitoring capabilities. These watches are also appreciated for their sleek and stylish designs, making them suitable for everyday wear.”

Research Associate Alicia Gong added, “As Chinese consumers’ expectations for smartwatch features and experiences continue to rise, entry-level models’ (≤$50) share is falling gradually.”

Brands summary

Huawei enjoys a good reputation among Chinese consumers. Driven by price cuts, its Children Watch 4 Pro ranked first in the bestseller list for the market in 2022. The Watch 3 Pro and GT 3 (46mm) were the other two top-three models for Huawei. The brand benefited from its relatively more focus on HLOS smartwatches, with its HLOS smartwatch shipments doubling in 2022 to support Huawei’s 9% YoY growth in 2022.

Good sales of Apple’s Watch Series 7 models, coupled with the newly released Watch Series 8 and Ultra models, helped Apple register 4% YoY shipment growth in China. Continued innovation in health monitoring functions, as well as the perfect data and interaction experience, drove Apple’s growth. Meanwhile, the Ultra has created a new segment of professional smartwatches, which helped Apple dominate the premium segments.

BBK (imoo) recorded a double-digit shipment decline YoY. BBK relies more on offline channels, which were impacted by the strict COVID policy in 2022. Although the brand’s Q1A and Z6A models ranked second and third respectively in the China smartwatch market in 2022, its newly launched Z8 and D3 models failed to overtake previous annual sales leaders Z3 and Z5.

Xiaomi’s smartwatches mainly belong to the <$200 segments. Its annual sales in the China market dropped 18% YoY in 2022 as demand shrank in the $101-$200 and ≤$50 segments.

OPPO saw a 105% YoY gain in 2022, mainly driven by its newly released Watch 3 Series. Its market share also increased to 3%.

Outlook

China’s smartwatch market is expected to rebound due to an active volume push by OEMs such as Huawei, Xiaomi, HONOR and OPPO against the backdrop of post-COVID reopening in 2023. The market’s ASP (average selling price) is also expected to rise due to the continuous demand for more professional models.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

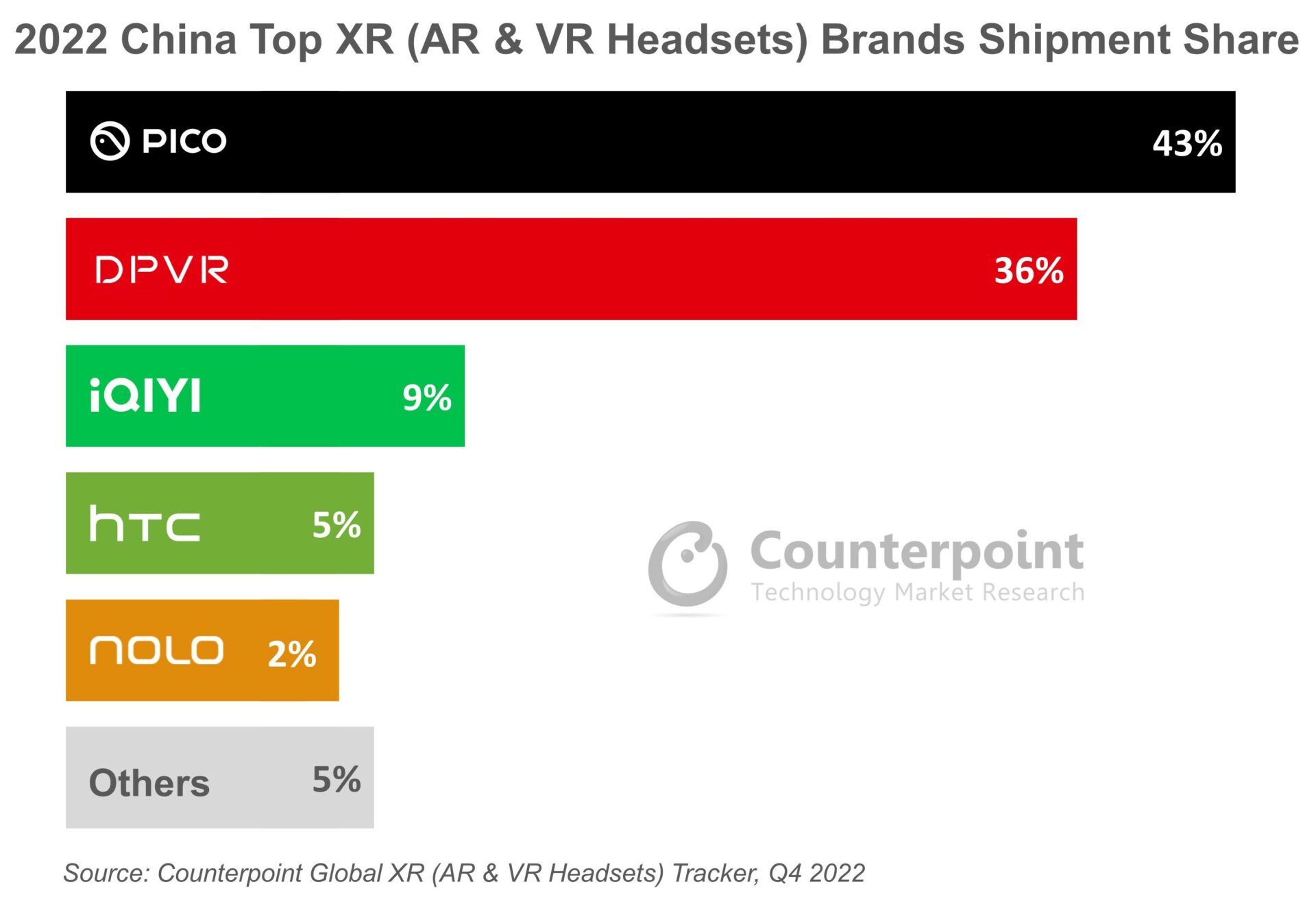

XR shipments crossed 1.1 million units in China in 2022.

VR remains the dominant segment, contributing more than 95% to overall shipments in 2022.

Pico is the number one brand with a shipment share of 43%, followed by DPVR at 36%.

iQIYI, HTC and NOLO, each captured a single-digit share.

London, San Diego, New Delhi, Beijing, Buenos Aires, Seoul, Hong Kong – March 15, 2023

Extended Reality [XR: Augmented Reality (AR) and Virtual Reality (VR) headsets] shipments crossed 1.1 million units in China in 2022 according to Counterpoint Research’s XR Model Tracker. VR remains the dominant segment within XR, contributing more than 95% to overall shipments in 2022. The Chinese market has considerable untapped potential but is growing slowly because available headsets do not offer enough value in the consumer domain for mass consumption.

While the consumer segment did not see a major shift, volume growth was produced by enterprise deals, mostly in the education and training sectors. The potential for further volume growth is limited in the enterprise segment which remains niche as the currently available headsets are not yet advanced enough to offer enticing use cases. So, brands have started to focus more on the consumer segment, particularly gaming. However, Chinese brands are offering few and mostly simple VR games. Brands must develop high-quality games to increase consumer traction.

Pico is the number one brand in China’s XR market with a shipment share of 43% in 2022, followed by DPVR at 36%. iQIYI, HTC and NOLO, each of which captured a single-digit share, also made it to the top five.

Pico, since its acquisition by TikTok’s parent, ByteDance, has gained greater global as well as local prominence. The additional financial, human and soft resources that ByteDance is pouring into Pico helped it to become a major player. Since the acquisition, Pico’s strategy has been to establish itself as a major player in the consumer XR segment. For this, it has priced its recent Pico 4 headset at close to $400, similar to Meta’s Quest 2.

DPVR shipped the next highest number of XR headsets in China and is the biggest player in the enterprise segment. Existing partnerships and growing regional prominence will ensure a healthy growth rate for DPVR, but it has a limited opportunity for volume growth in the enterprise segment. It is therefore betting big on its E4 gaming headset.

iQIYI, with a focus on VR content and streaming, took the third spot on the list while HTC’s volumes continued to be driven by Vive Flow. However, HTC is facing difficulty to sell its headsets owing to their high price points. NOLO also made it to the top five list thanks to its consumer-grade headsets targeted at gamers.

China’s market has a large base of home-grown content producers who benefit from a largely common language. We expect these players to increasingly invest in content for VR leading to a virtuous circle of increasingly capable hardware supported by content from multiple producers. The adoption of XR in sectors ranging from education and healthcare to industrial and supply chains will also enable more holistic growth represented by both the consumer and enterprise segments.

China is also expected to benefit from the early adoption of 5G since telecom operators see VR content as a driver of data consumption.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

The market showed decent YoY growth in 2022, though it dropped 8% YoY in Q4

Quarterly shipments turned to a YoY decline after seven consecutive quarters of growth.

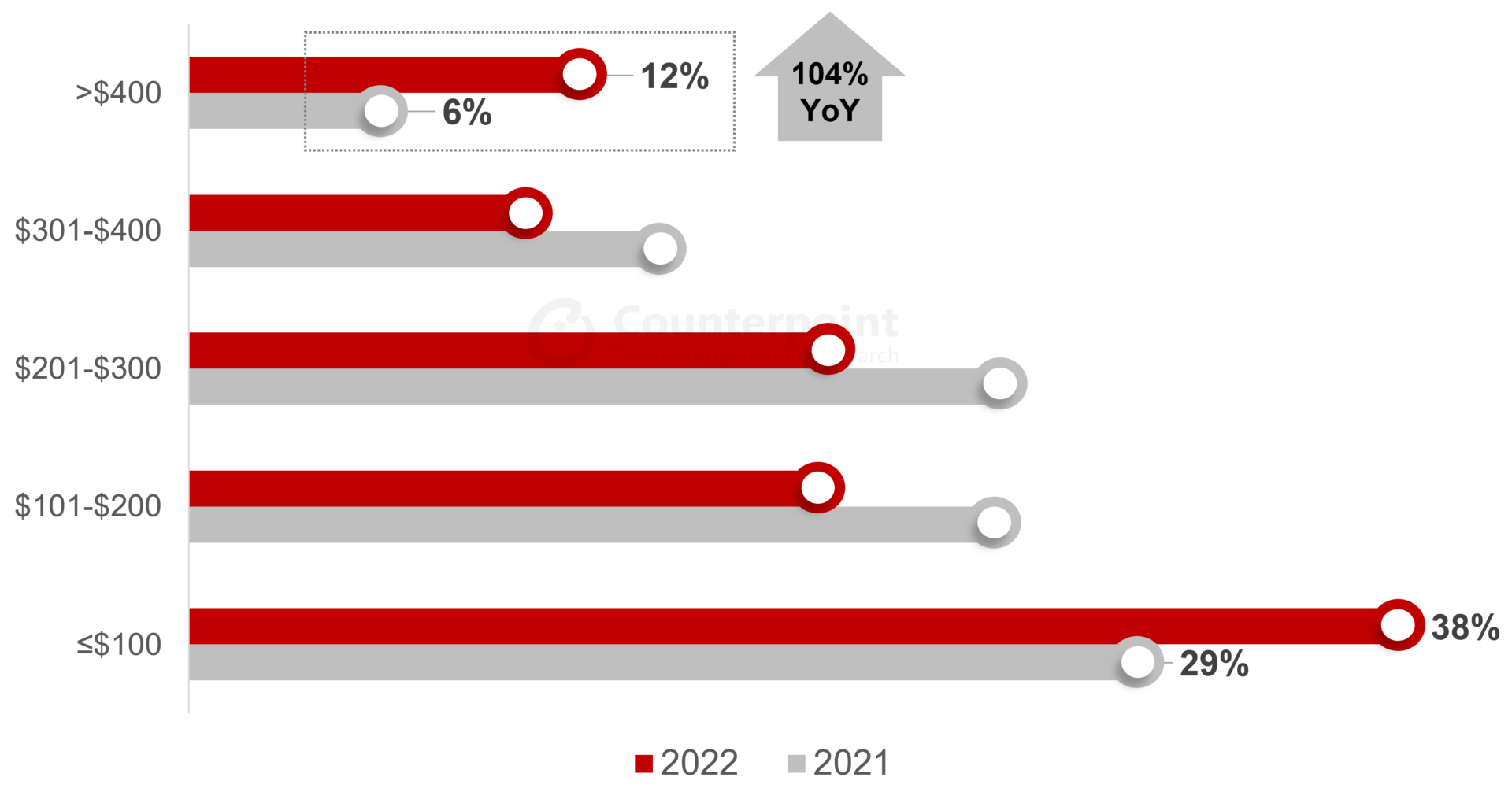

Shipments in the >$400 price band more than doubled in 2022, while the mid-price range saw a YoY drop.

Indian brands such as Noise and Fire Boltt found spots in the global top 5 sellers’ list thanks to the rapid growth of their domestic market.

Seoul, New Delhi, Hong Kong, Beijing, London, Buenos Aires, San Diego – February 22, 2023

The global smartwatch market shipments grew 9% YoY in 2022 due to the strong YoY growth witnessed in the first three quarters of the year, according to Counterpoint Research’s recently published Global Smartwatch Model Tracker. But the shipments fell 8% YoY in Q4 2022 amid inflationary pressures and slow India growth. This was the market’s first negative growth in eight quarters since the pandemic hit the world in 2020.

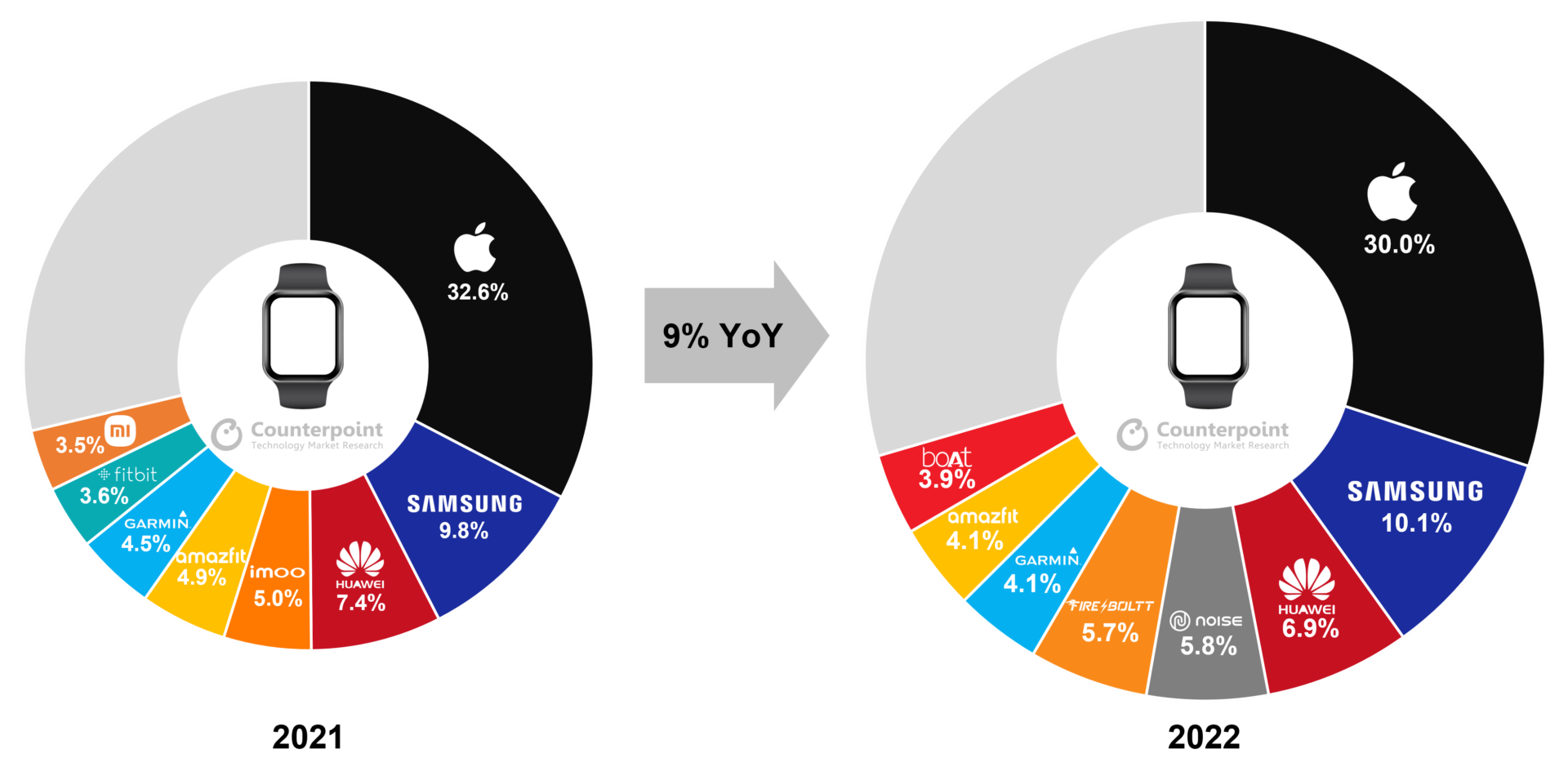

Global Top-selling Smartwatch Brands’ Shipment Share, 2022 vs 2021

Source: Counterpoint Global Smartwatch Model Shipment & Revenue Tracker, Q4 2022

The most striking feature of the year was price polarization in demand. Shipments in the mid-price range decreased while those in the >$400 and ≤$100 segments increased 104% and 41%, respectively, compared to the previous year.

Research Analyst Woojin Son said, “Apple strongly drove the average selling price (ASP) rise in the global smartwatch market in 2022, especially in the >$400 price band. There are two main reasons for this ASP rise – a diversified Apple smartwatch line-up and a rise in the exchange rate. This year, Apple released its first premium model, Ultra, at a release price of $799 in the US. In addition, as the exchange rate rose, the local price of Apple Watch in various countries changed. The demand for the premium segment remained relatively strong despite the decline in consumer sentiment at the end of 2022.

Son added, “On the other hand, we must be cautious about the low-price band of sub-$100. While this segment expanded in 2022 along with the remarkable growth of India’s market, it showed a large withdrawal in Q4 when compared to Q3.”

Global Smartwatch Shipment Share by Wholesale Price Band, 2022 vs 2021

Source: Counterpoint Global Smartwatch Model Shipment & Revenue Tracker, Q4 2022

Market summary

In 2022, Apple’s global market share decreased by 2.6%p with shipments remaining almost flat year on year. In terms of revenue, however, it grew 15% YoY, accounting for 56% of the global smartwatch market revenue and further widening the gap with No. 2 Samsung.

Samsung’s yearly shipments increased by 12% to account for more than 10% of global smartwatch shipments in 2022. Although sales of the newly released Galaxy Watch 5 series in the year were positive, its revenues only increased by less than 1%, which seems to be largely due to a slight drop in the ASP compared to the previous year.

Huawei‘s market share fell 0.5%p YoY due to the Chinese smartwatch market losing momentum to India in 2022. However, the brand’s revenue increased by 20% thanks to its relative focus on HLOS* smartwatches.

Noise and Fire Boltt, the Indian brands that supported the rapid growth of their home market, showed excellent growth in 2022. The two brands surpassed 5% of the global market share to rank fourth and fifth, respectively. Although the makers failed to beat Huawei as the Indian market’s growth slowed in Q4, they are attracting discussions on whether they will be able to threaten Samsung’s position beyond Huawei next year.

Fitbit and Xiaomi’s rankings fell to 10th and 11th in 2022 from 7th and 8th in the previous year. The strength of Indian brands was also affected, but these two brands failed to defend their share in their main markets like North America (Fitbit) and China (Xiaomi). Their shipments were decreased or flat compared to the previous year.

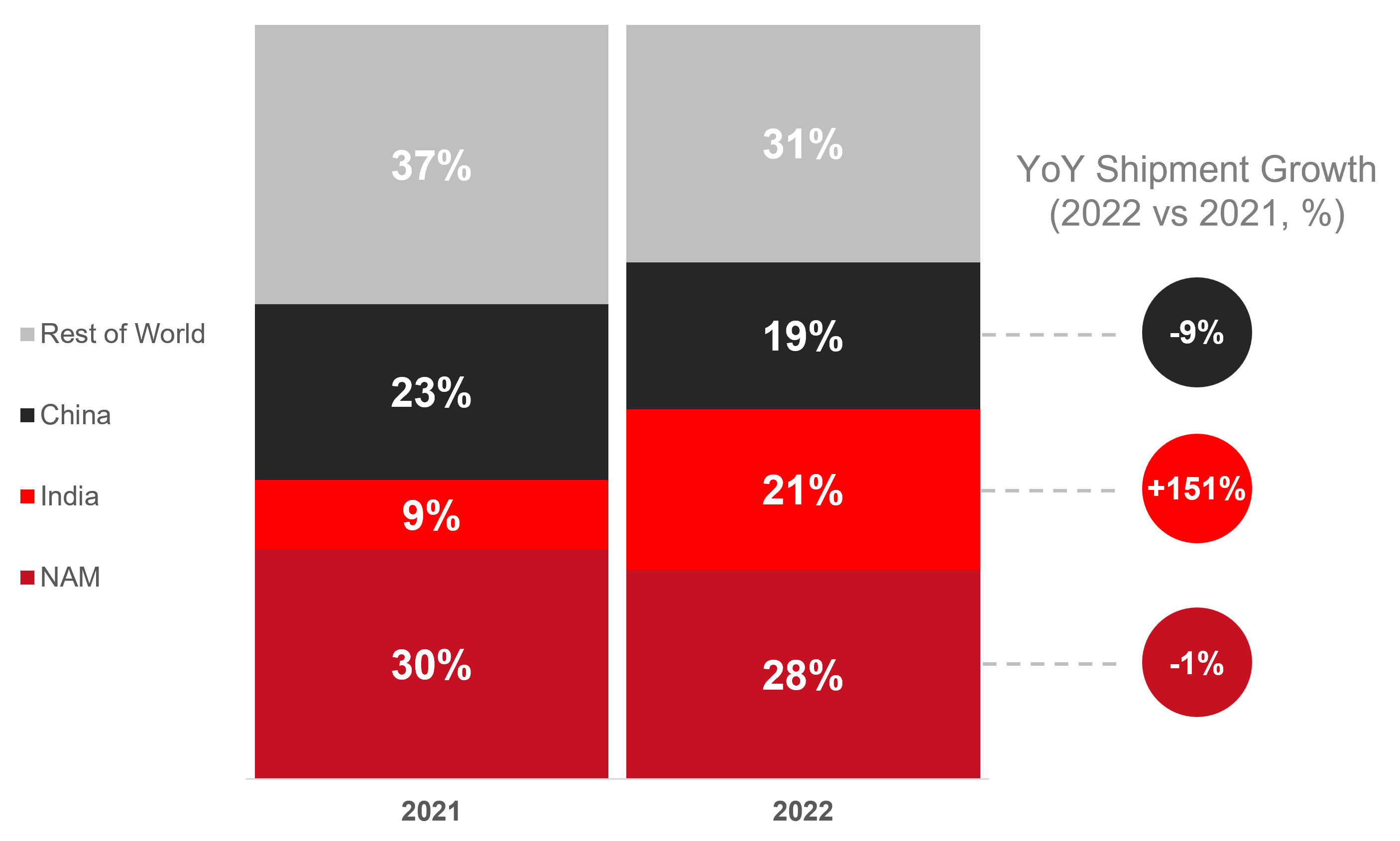

Smartwatch Shipment Share by Region, 2022 vs 2021

Note: Figures may not add up to 100% due to rounding

Source: Counterpoint Global Smartwatch Model Tracker, Q4 2022

In terms of regions, North America recovered as the largest smartwatch market in Q4 2022, which also allowed it to remain in first place for a full year again. The Apple’s home market showed a significant increase in shipments QoQ, despite the sales of Apple Watches being lower than expected in the fourth quarter. However, North America’s share decreased slightly as India emerged as another core region in 2022.

India’s market more than doubled compared to 2021. It grew steadily until Q3 2022 but fell 36% QoQ in Q4. Senior Analyst Anshika Jain said, “The third quarter of 2022 saw a big rise because most of the brands pushed high inventories into the channel ahead of the festive season. Therefore, we saw a decline in shipments in the fourth quarter.”

In the fourth quarter of 2022, China’s shipments rebounded for the first time in the year as the COVID-zero policy was eased, and both Huawei and Apple are received a positive response with their more diverse products.

*Smartwatch type definition

HLOS smartwatch: Electronic watch running a high-level OS, such as Watch OS (Apple) or Wear OS (Samsung), with the ability to install third-party apps.

Basic smartwatch: Electronic watch running a lighter version of an OS, with the inability to install third-party apps.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

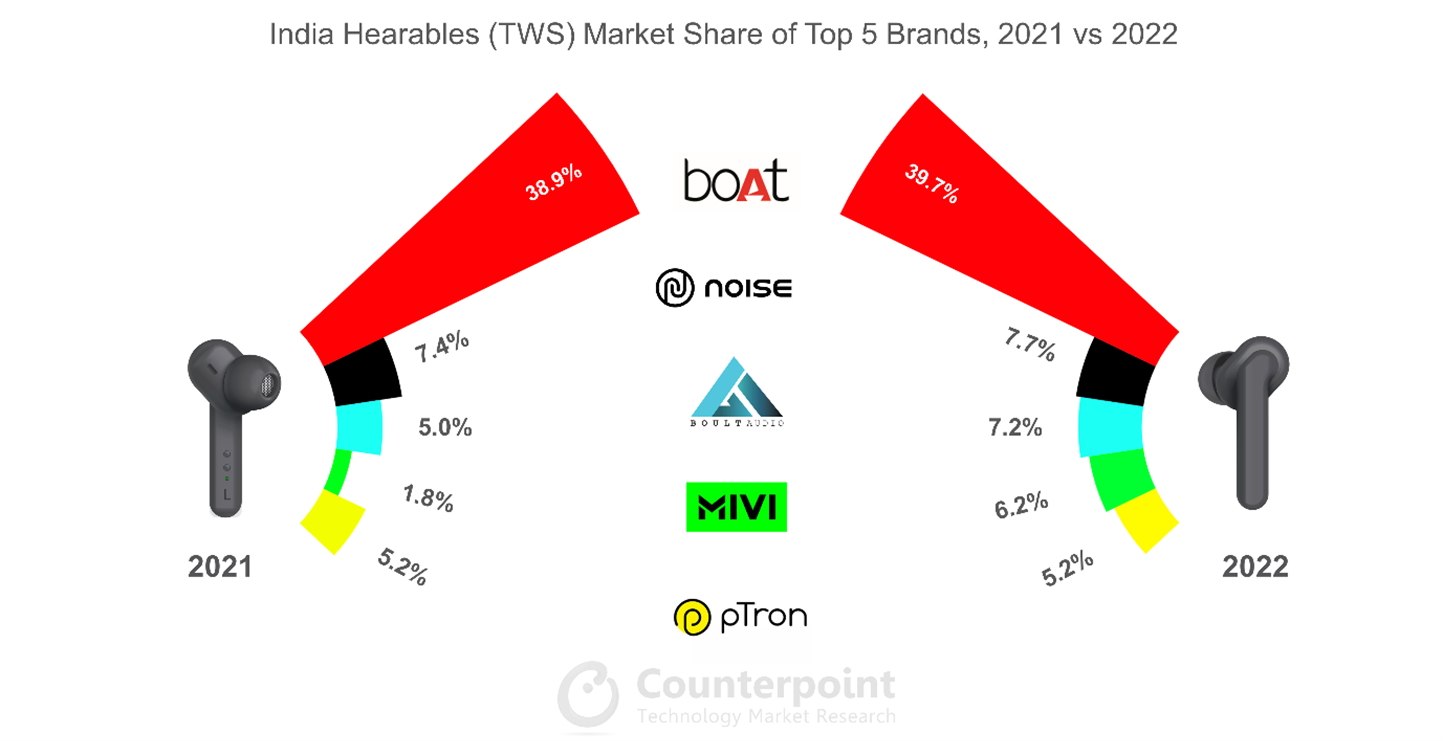

Leading player boAt posted 89% YoY growth, contributing two-fifths of the total shipments.

For the first time, the top five spots in the India TWS market were captured by local brands.

Indian brands reached their highest ever share of 80%.

Domestic manufacturing captured a 30% shipment share in 2022, compared to just 2% in 2021.

The average selling price dropped by 20% YoY in 2022.

New Delhi, Beijing, Hong Kong, Seoul, London, San Jose, Buenos Aires – February 21, 2023

India’s TWS market shipments registered 85% YoY growth in 2022, according to the latest research from Counterpoint’s IoT service. Increasing local manufacturing helped drive the shipments, apart from timely sales events, frequent affordable offerings, and entry of new players.

Commenting on TWS brands’ performance in 2022, Senior Research Analyst Anshika Jain said, “Four-fifths of the total market was captured by Indian brands, their highest-ever share. For the first time, the top five spots were taken by local brands, which captured two-thirds of the total TWS shipments in India. Moreover, the majority of the new entrants this year were local brands. Further, Mivi, with its entirely locally produced TWS portfolio, grew 544% YoY and grabbed a position in the top five for the first time.

Evidently, Chinese and global brands lost some of their share to the Indian players this year. Chinese brands captured a 13% share in 2022 driven by the good performance of OnePlus’ feature-rich devices Nord Buds and Nord Buds CE. realme and OPPO also supported the growth of Chinese brands. Global brands took an 8% share led by Apple, Samsung and JBL.”

Talking about the local production scenario, Associate Director Liz Lee said, “Domestic manufacturing saw rapid growth, contributing 30% of the total shipments in 2022, compared to just 2% in 2021. Key homegrown brands boAt, Mivi and pTron ramped up their local manufacturing capabilities to account for 73% of the domestic shipment volume in 2022. Other key players like Noise, Truke, Boult Audio, Wings, Gizmore and Play also manufactured made-in-India devices for the first time this year. Moreover, this increase in the shipment share of local production largely led to a drop in the ASP (average selling price) by 20% in 2022. More new launches in the low-price band (INR 1,001-INR 2,000 or around $13-$25) also contributed to the drop.”

Source: India Hearables (TWS) Shipments, Model Tracker, 2021 vs 2022

Market Summary for 2022

boAt took the lead for the third year in a row with 89% YoY growth driven by increased penetration in domestic manufacturing, multiple affordable launches, and aggressive promotions. It captured seven spots in the rankings for top-10 best-selling models. The Airdopes 131 remained the top-selling model for the second consecutive year with a 10% share of the total TWS market shipments.

Noise rose to the second spot with 2x YoY The brand focused on its VS series which caters to the <INR 2,000 (or $25) price band. It added many new devices to the series in this period. Moreover, it opened the year 2022 with its expansion towards local production. As a result, it became the third-largest brand to offer made-in-India TWS devices.

Boult Audio grabbed the third spot with a 7% share and 167% YoY growth driven by aggressive marketing strategies and multiple new feature-rich offerings below INR 2,000 (<$25). It also entered the domestic manufacturing space for the first time in 2022. The majority of its volume was driven by the INR 1,001-INR 2,000 (or around $13-$25) retail price band. The Airbass XPods was the best-seller in its entire TWS portfolio.

Mivi grew 544% YoY this year and took the fourth position in the rankings for top-five brands for the first time, driven by its full-fledged made-in-India TWS portfolio, a good number of launches and huge presence in the entry-level price band (<INR 1,000 or around <$13) and low-price band (INR 1,001-INR 2,000 or around $13-$25).

PTron again took the fifth spot with a 5% share of the total TWS shipments. In addition, it was the largest brand in the entry-level price band (<INR 1,000 or around <$13).

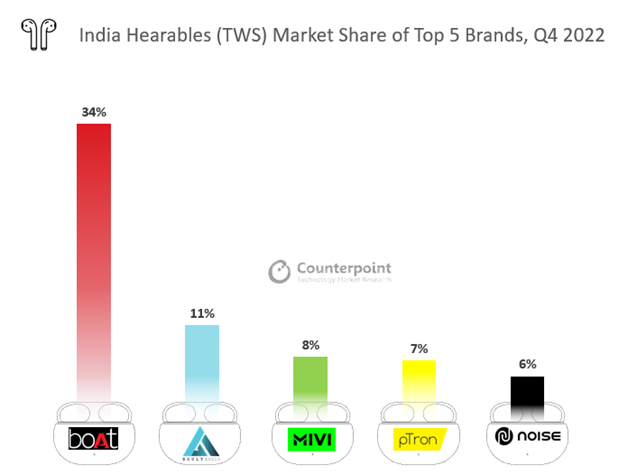

Source: India Hearables (TWS) Shipments, Model Tracker, Q4 2022

Market Summary for Q4 2022

India’s TWS shipments saw 44% YoY growth in Q4 2022 driven by festive season sales and promotions and growing local production.

boAt grew 3% YoY to mark its tenth consecutive quarter of lead in Q4 2022, while Boult Audio stood second for the first time with an 11% share.

The top five TWS brands in India were all local brands – boAt, Boult Audio, Mivi, Ptron and Noise. They accounted for two-thirds of the total shipments.

In Q4 2022, Indian brands captured a record 84% share driven by boAt, Boult Audio, Mivi, Ptron and Noise.

With a 4% share, the boAt Airdopes 131 remained the top model for the seventh consecutive quarter in Q4 2022.

The INR 1,001-INR 2,000 retail price band (or around $13-$25) continued to fuel the TWS demand in India during Q4 2022 with an increased shareof 75% in the overall shipments. boAt mainly drove the volume for this price band with a 45% share, followed by Boult Audio, Mivi, Noise and Wings.

The premium segment (>INR 5,000 or around >$60) captured a 4% share this quarter, driven by Samsung followed by Apple and JBL.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

At CES 2023, which was held in early January, interest in XR was hot, and the number of innovation awards related to virtual/augmented reality surged to 25 in two years. Several startups and manufacturers also showcased new XR-related technologies along with their products at the show.

Here, we will focus on two of the XR-related technologies showcased at CES 2023 – a transparent display with XR and hands-free controllers. These technologies are the foundation for XR to expand into various areas such as health and education.

1. Transparent display with XR technology

Transparent display categories include HUD (head-up display), HMD (head-mounted display), transparent OLED, and more. HUD is often used as a display for vehicles. However, until now, commercialized HUD for vehicles has taken up only a part of the front glass. But at CES 2023, several automakers introduced AR HUD with more advanced forms and expanded areas.

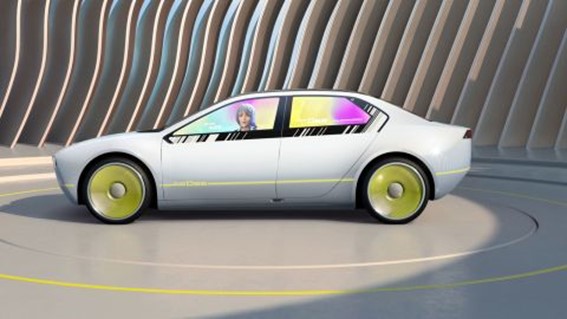

Most prominently, BMW unveiled ‘BMW i Vision Dee’ and announced its plan to commercialize by 2025 advanced HUDs that use the entire front glass. Also, BMW will expand its personalization experience by allowing the driver’s avatar to be displayed in the side window. This advanced HUD is combined with the MR slider to set a range of information displayed on the HUD. The range varies from driving-related information to virtual/augmented reality information.

BMW i Vision Dee

Source: BMW

However, in the future, if the transparent OLED introduced by LG Display at CES 2023 is commercialized, it could replace HUD that transmits images to the windshield. LG Display introduced a concept car equipped with a 55-inch transparent OLED at CES 2023. The transparent OLED serves as a window, provides content such as advertisements and news, and provides information on places outside the window in real-time through AR technology. This means that AR technology can expand opportunities to provide various experiences to all occupants, not just driver assistance features.

LG Concept Car With Transparent OLED

Source: LG Display

2. Hands-free tracker

Among the CES’ innovation awards in the virtual/augmented reality category, controllers were included to highlight how they allow users to have various experiences hands-free.

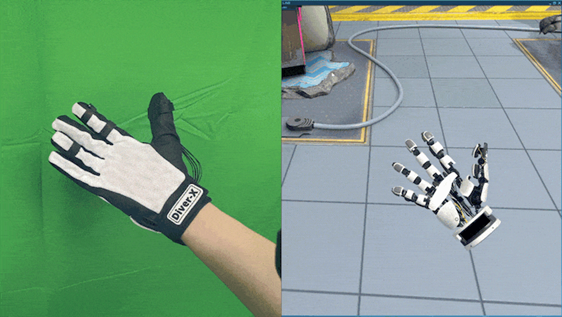

Contact Glove of Japanese company Diver-X is a haptic VR controller in the form of gloves. The glove is a tactile controller compatible with all SteamVR games, allowing VR gamers to enjoy an in-depth gaming experience. In addition, the device can capture the user’s hand movements and manipulate buttons and sticks with only finger movements.

Contact Glove by Diver-X

Source: Kickstarter

Another innovation award-winning Surplex, a body tracker in the form of shoes, was announced by the Chinese company Shenzhen Qianhai Xiangfang Future Technology. The device, with its 480 embedded pressure sensors, has the advantage of not being space constrained. Also, it is compatible with all SteamVR-compatible headsets such as the Oculus Quest 2. Such hands-free controllers are expected to be of great help in expanding the use cases in the industrial segment as well as the experience of general consumers in virtual/augmented reality.

Surplex Full-body Tracking Shoes

Source: CES

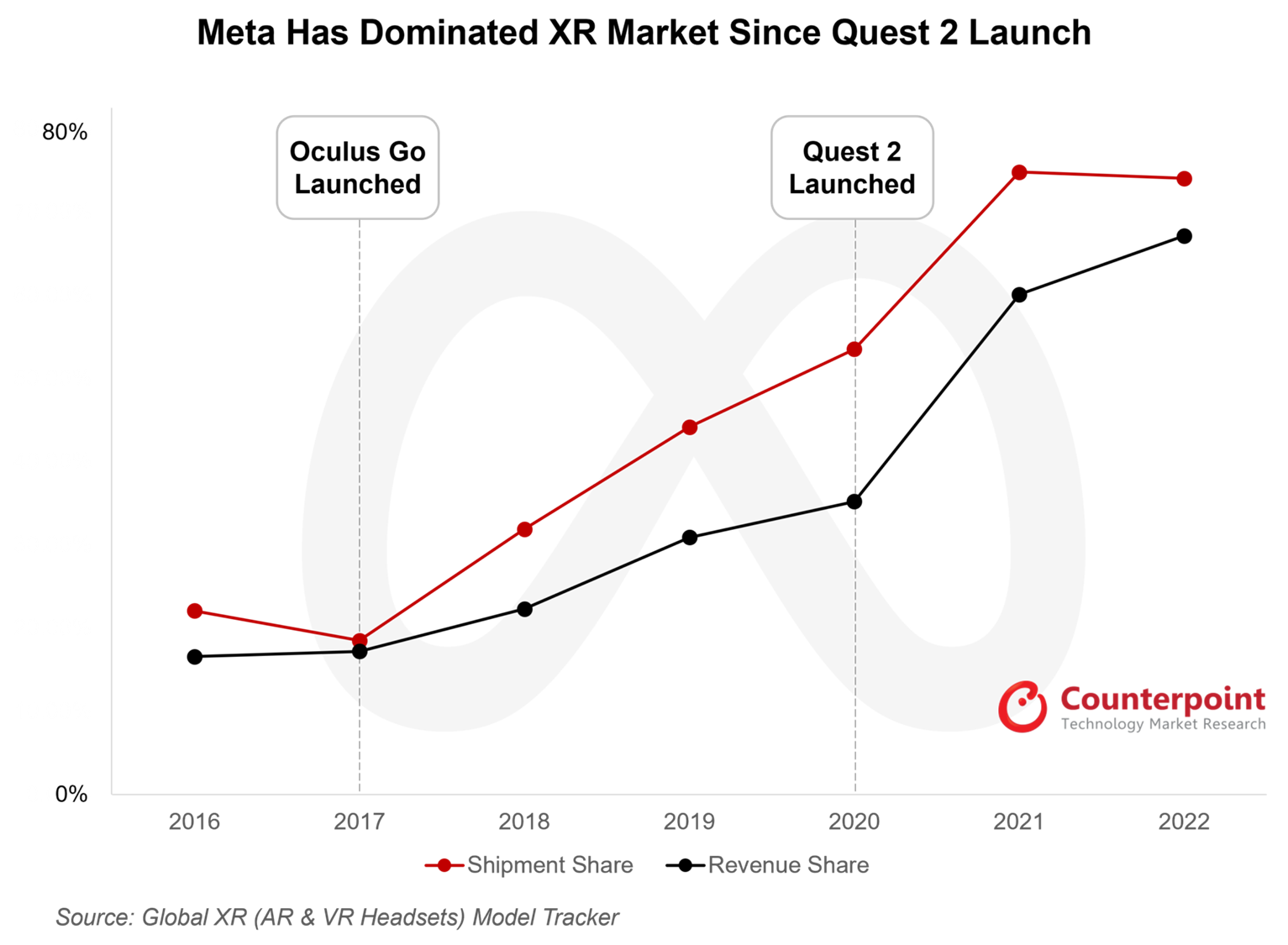

In 2021, the total XR market size was about 11 million units and Meta was the main player with about 75% market share. According to the latest Counterpoint Global XR(VR/AR) Forecast, the XR market is expected to grow to about 63 million units by 2027. However, Meta is expected to lose its market share as new players such as Apple will enter the market. Therefore, competition in the XR market is expected to intensify, and manufacturers will constantly diversify the use of XR devices to defend market share. Accordingly, it is anticipated that new technologies related to XR will continue to pour in.

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Source: Counterpoint Global Smartwatch Model Shipment & Revenue Tracker, Q1 2023

Source: Counterpoint Global Smartwatch Model Shipment & Revenue Tracker, Q1 2023