At CES 2024 in Las Vegas, our Research Director, Peter Richardson sat down with RayNeo’s Global PR Manager, Dongyao Nie to deep-dive into their AR offerings. Dongyao spoke about the RayNeo X2, the world’s first microLED AR glasses that offer clear, bright, and transparent displays. She highlighted features like live translations, 3D navigation, and interactive 3D avatars. She also spoke about the new and improved RayNeo X2 Lite, a lighter version powered by Qualcomm’s Snapdragon AR1 Gen 1 platform and RayNeo AI assistant. The company is also promising significant advancements in AR glasses for convenient daily life integration.

Coverage: Emerging Tech

Counterpoint Conversations: Spatial AI, The Next Frontier in Extended Reality (XR) Experiences

At the Snapdragon Summit 2023, our Research Director, Neil Shah, had a quick chat with Hugo Stewart, the XR guru at Qualcomm, about the advancements in Extended Reality (XR) technology. Hugo discussed recent chipsets, including the XR2 Gen 2 that powers the Meta Quest 3, while highlighting its improved graphics, AI capabilities, and video pass-through for Mixed Reality (MR). Additionally, Qualcomm also introduced the AR1 Gen 1 SoC for smart glasses, emphasizing its role as an AI device with cameras serving as eyes for immersive experiences. Hugo also spoke about distinctions between smart glasses and AR glasses, highlighting the potential applications such as translation, navigation, and fitness. The conversation extends to the development side, covering Qualcomm’s Spaces developer platform, supporting over 5,000 developers in creating content and applications for XR. Lastly, Neil and Hugo also explore the concept of Spatial AI, envisioning immersive experiences like watching sports from different angles, and virtual meetings as key applications for the future of XR technology.

The Interview:

Related Posts

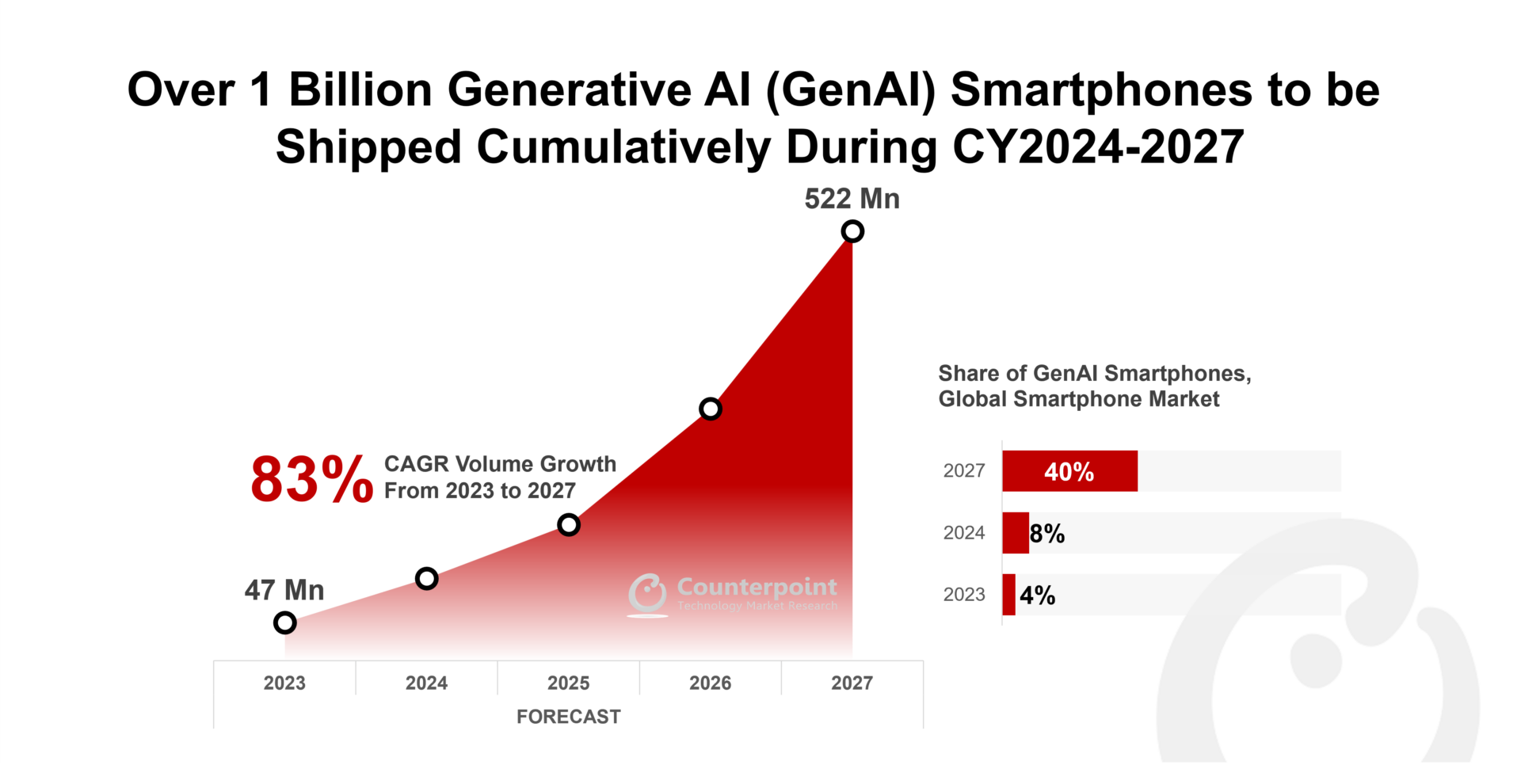

Over 1 Billion Generative AI (GenAI) Smartphones to be Shipped Cumulatively During CY2024-2027

Our analyst interviews

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

![]()

Guest Post: OpenAI Reboot: Ecosystem Still in Trouble

OpenAI has been put back the way that it was, but the governance will be very different and the damage that has been done to its ecosystem aspirations could greatly impact its long-term future.

- Altman and his crew have been reinstated at OpenAI and a new board has been formed. But how the non-profit part of OpenAI’s mission has changed is not clear at this stage.

- The previous structure of OpenAI was a non-profit company with a subsidiary that would be able to make money. It is in this subsidiary that most of the investments have been made.

- The problem is that OpenAI’s mission to develop artificial general intelligence (AGI) has a rapacious appetite for compute resources which is where the vast majority of the over $11 billion that Microsoft has invested has been spent.

- This is where the non-profit and for-profit ideologies bump against each other as Microsoft has a fiduciary duty to make money for its shareholders and shoveling $11 billion into a black hole with no prospect of a return is a breach of that duty.

- This is why there is an unusual situation in the for-profit subsidiary where Microsoft’s return is capped at 100x, which for all intents and purposes is perfectly fine.

- The problem is that the board that oversaw OpenAI (and the for-profit subsidiary) was only supposed to care about AI benefitting humanity, which also means capping AI that it thinks could trigger the machine takeover of the human race.

- I am pretty sure that this was the source of the conflict that led to the firing of Altman, but I suspect that it was rumors of a breakthrough in AI that were the catalyst for the recent events.

- This “breakthrough” in AI, which has been termed Q*, appears to have been enough to make the board nervous and it may have something to do with reasoning.

- I suspect that this “breakthrough” will be an enhancement of GPT models that makes them appear to be better at reasoning.

- So far, I have seen no evidence whatsoever that any deep learning system is capable of reasoning.

- Instead, what they are very good at is learning from examples and then applying that learning in a controlled setting.

- The minute the setting becomes uncontrolled, deep learning systems go off the rails and start making things up or hallucinating or making horrible errors on the road that force the humans to take over.

- This is because they have no causal understanding of the tasks that they are performing and instead only understand the correlation.

- If this “breakthrough” involves reasoning and is real, then this would represent a step along the way to AGI.

- However, all of the evidence I have seen suggests that while the machines can simulate reasoning, they always fall over the minute that they are put to a real test on data that they have not seen before.

- This would also not be the first time that a heralded breakthrough from OpenAI turned out to be a red herring (Robotic Rubik Cube solver).

- Hence, I suspect that all of the fuss about a robot apocalypse may have damaged OpenAI’s long-term outlook and greatly aided its competitors.

- OpenAI launched its play for the AI ecosystem just this month and to make it successful, everyone needs to have complete confidence in OpenAI as a going concern as they will be basing their apps and services upon its foundation models or GPT itself.

- The recent antics have shattered that confidence and now OpenAI will have to work much harder to shore up developer confidence that it will be around for the long term.

- To make matters worse, it will now be much easier for rivals to lure developers, meaning that the whole ecosystem proposition has taken a large hit.

- OpenAI is out of the woods and has a future, but its valuation and the prospect of dominating the AI ecosystem remain in disarray.

(This guest post was written by Richard Windsor, our Research Director at Large. This first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

Related Posts

OpenAI Saga: UNO Game and What it All Means For AI

Guest Post: Meta’s Instagram Fee Proposal Priced to Fail?

Meta doesn’t expect anyone to pay for Instagram.

Meta’s proposal to charge $10.5 per month for Instagram looks deliberately priced to fail, creating a strong incentive for users in the EU to explicitly allow targeted advertising which will also test just how valuable the service is to its users.

Meta Platforms is currently embroiled in negotiations with the EU with regard to its business model where the regulators’ view is that just because users clicked “Agree” to an agreement, this does not give Meta the right to target them with advertisements. This is an ongoing issue as Meta was fined €390 million by Ireland’s Data Privacy Commissioner for precisely this activity and was told it had to think of something else.

The monetization model for digital ecosystems can have three methods – hardware, advertising and subscription. Advertising and subscription are mutually exclusive and the option for users to choose one or the other is now commonplace across many types of digital services.

RFM Research conducted a study in 2018 that examined the viability of digital ecosystems switching from advertising to subscription as their source of revenue. The results of the study indicated that while X and Snap could probably make the switch without risking damage to their revenue base, the same was not true for the larger players such as Google and Meta Platforms. This is because although they generate an average revenue per user (ARPU) of around $3.00-$3.60 per month, the distribution of ARPU within the user base is very large.

For example, even though the US makes up a small portion of the user base, it often accounts for as much as 50% of revenues, indicating that US users generate far more advertising revenues per user than non-US users. This creates a pricing problem for subscription because in order to ensure that revenue is not lost, the price would have to be so high that no one would ever pay it.

The $3.00-$3.60 ARPU includes all of Meta’s properties and so it is easy to deduce that ARPUs for Instagram in the EU are likely to fall well short of $1 per user per month. Hence, a price of $10.5 per user per month represents a price increase of more than 950% and it’s pretty clear that no user in the EU will be willing to pay it.

It seems that this is precisely what Meta Platforms is aiming at. In order to keep the regulator happy, it provides an option that no one will want, and assuming that the users still want to use Instagram, they will sign up for targeted advertising in a way that satisfies the EU.

The risk of this strategy is that users decide that Instagram is actually not that important and stop using it entirely, although its engagement and user metrics indicate that this is a very small risk. Instead, what can be expected is that Meta makes this offer and almost all of its users sign up for targeted advertising and life returns to normal.

Hence, there doesn’t seem to be any meaningful implications from this issue, although there may be another fine in the works for infractions that Meta may have committed in the past.

(This guest post was written by Richard Windsor, our Research Director at Large. This first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

Related Posts

Guest Post: OpenAI Haymaker?

OpenAI makes hay while the sun shines.

When a company that has issues with making profits can raise money at a valuation of $85 billion, it becomes abundantly clear that investors in generative AI have taken leave of their senses.

Open AI is reportedly raising money at a valuation of $80 billion to $90 billion. This looks like an opportunistic event for two reasons.

First, doubts over whether Open AI actually needs the money. It was only nine months ago that Microsoft invested $10 billion in OpenAI, meaning that if it has run out of money already, then it has a cash burn of $1.1 billion per month. This is Reality Labs’ levels of cash burn which with 400 employees amounts to $2.75 million per employee per month.

The vast majority of this spend will be going to compute costs where even with 100 million users making 30 requests per day this is an uneconomic level of spending. This would mean that ChatGPT and generative AI generally can never become a viable business or generate a positive ROI and so one suspects that OpenAI has in fact got plenty of money left.

Second, virtually free money. In the market’s mind, OpenAI is the leading generative AI company in the world (which is debatable). Furthermore, generative AI is the hottest theme in the technology sector by a wide margin, meaning that OpenAI sits at the pinnacle of what the market wants to own. This in turn means that OpenAI can sell far fewer shares for the money it wants to raise, and its existing shareholders can also register large unrealized gains on their balance sheets. Consequently, I think that this raise is opportunistic in that the market has given OpenAI an opportunity to capitalize on its fame and popularity.

However, most telling of all is that employees will also have an opportunity to sell some of their shares as part of this transaction. Insider stock sales are often an indicator of the insiders’ view that the valuation of the shares has hit a peak. At $85 billion, this is pretty hard to argue against.

OpenAI is supposed to earn revenues of $250 million this year and $1 billion next year, putting the shares on over 80x 2024 revenues. This is very high even in the best of times, but the plethora of start-ups and the thousands of models being made available for free by the open-source community leads one to think that competition is on the way.

Hence, price erosion is likely which in turn could lead to OpenAI missing the $1-billion revenue estimate for 2024 and burning through even more cash than expected. OpenAI will not be alone, and many start-ups will suffer from price erosion that will cause their targets to be missed. This could well be the pin that pricks the current bubble, causing enthusiasm to wane and valuations to fall.

OpenAI may not be worth $85 billion but the timing of the raise is perfect.

(This guest post was written by Richard Windsor, our Research Director at Large. This first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

Related Posts

Podcast #69: ChatGPT and Generative AI: Differences, Ecosystem, Challenges, Opportunities

Generative AI has been a hot topic, especially after the launch of ChatGPT by OpenAI. It has even exceeded Metaverse in popularity. From top tech firms like Google, Microsoft and Adobe to chipmakers like Qualcomm, Intel, and NVIDIA, all are integrating generative AI models in their products and services. So, why is generative AI attracting interest from all these companies?

While generative AI and ChatGPT are both used for generating content, what are the key differences between them? The content generated can include solutions to problems, essays, email or resume templates, or a short summary of a big report to name a few. But it also poses certain challenges like training complexity, bias, deep fakes, intellectual property rights, and so on.

In the latest episode of ‘The Counterpoint Podcast’, host Maurice Klaehne is joined by Counterpoint Associate Director Mohit Agrawal and Senior Analyst Akshara Bassi to talk about generative AI. The discussion covers topics including the ecosystem, companies that are active in the generative AI space, challenges, infrastructure, and hardware. It also focuses on emerging opportunities and how the ecosystem could evolve going forward.

Click to listen to the podcast

Click here to read the podcast transcript.

Podcast Chapter Markers

01:37 – Akshara on what is generative AI.

03:26 – Mohit on differences between ChatGPT and generative AI.

04:56 – Mohit talks about the issue of bias and companies working on generative AI right now.

07:43 – Akshara on the generative AI ecosystem.

11:36 – Akshara on what Chinese companies are doing in the AI space.

13:41 – Mohit on the challenges associated with generative AI.

17:32 – Akshara on the AI infrastructure and hardware being used.

22:07 – Mohit on chipset players and what they are actively doing in the AI space.

24:31 – Akshara on how the ecosystem could evolve going forward.

Also available for listening/download on:

![]()

![]()

![]()

Guest post: AI Business Model on Shaky Ground

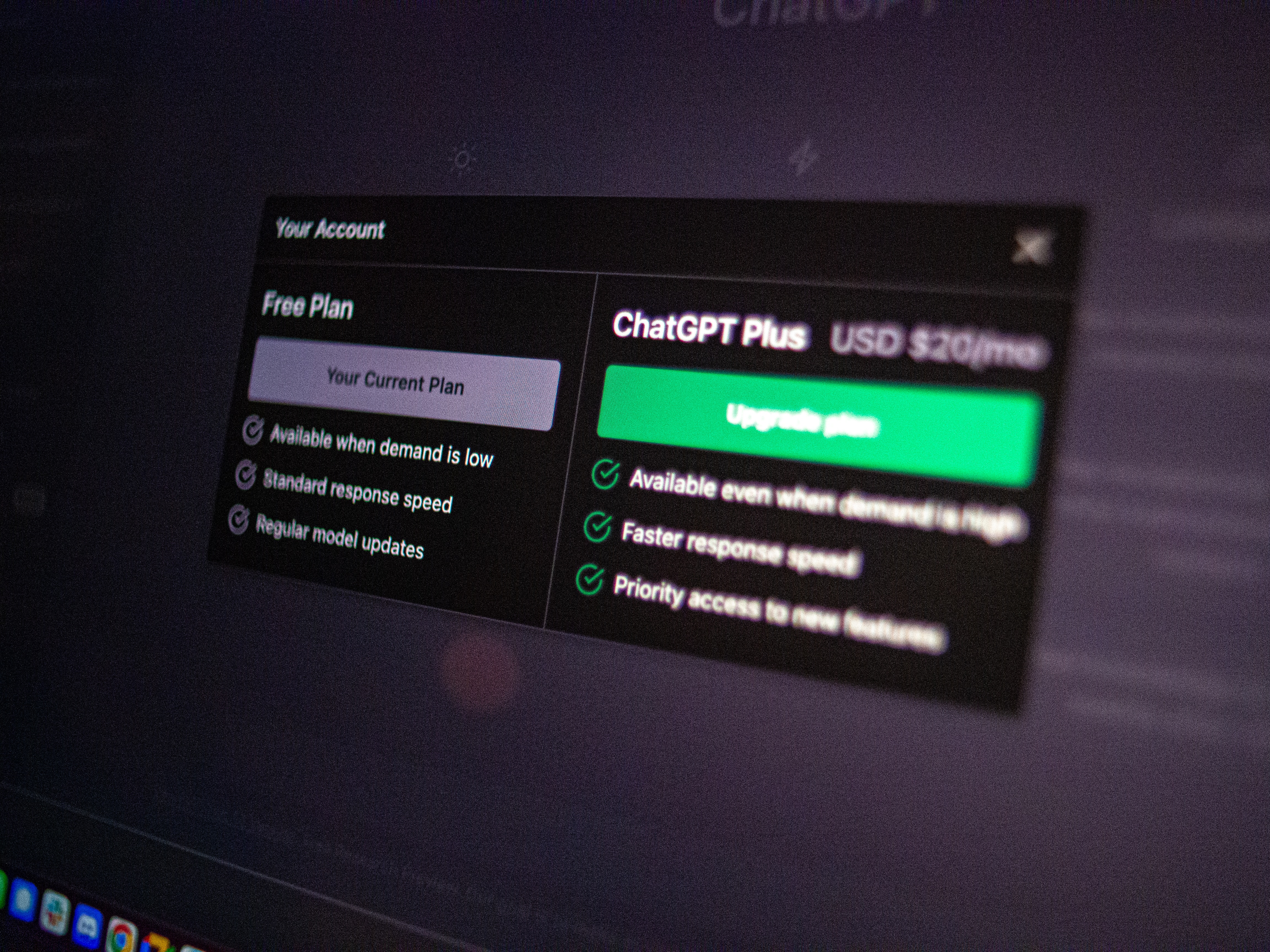

OpenAI, Midjourney and Microsoft have set the bar for chargeable generative AI services with ChatGPT (GPT-4) and Midjourney costing $20 per month and Microsoft charging $30 per month for Copilot. The $20-per-month benchmark set by these early movers is also being used by generative AI start-ups to raise money at ludicrous valuations from investors hit by the current AI FOMO craze. But I suspect the reality is that it will end up being more like $20 a year.

To be fair, if one can charge $20 per month, have 6 million or more users, and run inference on NVIDIA’s latest hardware, then a lot of money can be made. If one then moves inference from the cloud to the end device, even more is possible as the cost of compute for inference will be transferred to the user. Furthermore, this is a better solution for data security and privacy as the user’s data in the form of requests and prompt priming will remain on the device and not transferred to the public cloud. This is why it can be concluded that for services that run at scale and for the enterprise, almost all generative AI inference will be run on the user’s hardware, be it a smartphone, PC or a private cloud.

Consequently, assuming that there is no price erosion and endless demand, the business cases being touted to raise money certainly hold water. While the demand is likely to be very strong, I am more concerned with price erosion. This is because outside of money to rent compute, there are not many barriers to entry and Meta Platforms has already removed the only real obstacle to everyone piling in.

The starting point for a generative AI service is a foundation model which is then tweaked and trained by humans to create the service desired. However, foundation models are difficult and expensive to design and cost a lot of money to train in terms of compute power. Up until March this year, there were no trained foundation models widely available, but that changed when Meta Platforms’ family of LlaMa models “leaked” online. Now it has become the gold standard for any hobbyist, tinkerer or start-up looking for a cheap way to get going.

Foundation models are difficult to switch out, which means that Meta Platforms now controls an AI standard in its own right, similar to the way OpenAI controls ChatGPT. However, the fact that it is freely available online has meant that any number of AI services for generating text or images are now freely available without any of the constraints or costs being applied to the larger models.

Furthermore, some of the other better-known start-ups such as Anthropic are making their best services available online for free. Claude 2 is arguably better than OpenAI’s paid ChatGPT service and so it is not impossible that many people notice and start to switch.

Another problem with generative AI services is that outside of foundation models, there are almost no switching costs to move from one service to another. The net result of this is that freely available models from the open-source community combined with start-ups, which need to get volume for their newly launched services, are going to start eroding the price of the services. This is likely to be followed by a race to the bottom, meaning that the real price ends up being more like $20 per year rather than $20 per month. It is at this point that the FOMO is likely to come unstuck as start-ups and generative AI companies will start missing their targets, leading to down rounds, falling valuations, and so on.

There are plenty of real-world use cases for generative AI, meaning that it is not the fundamentals that are likely to crack but merely the hype and excitement that surrounds them. This is precisely what has happened to the Metaverse where very little has changed in terms of developments or progress over the last 12 months, but now no one seems to care about it.

(This guest post was written by Richard Windsor, our Research Director at Large. This first appeared on Radio Free Mobile. All views expressed are Richard’s own.)