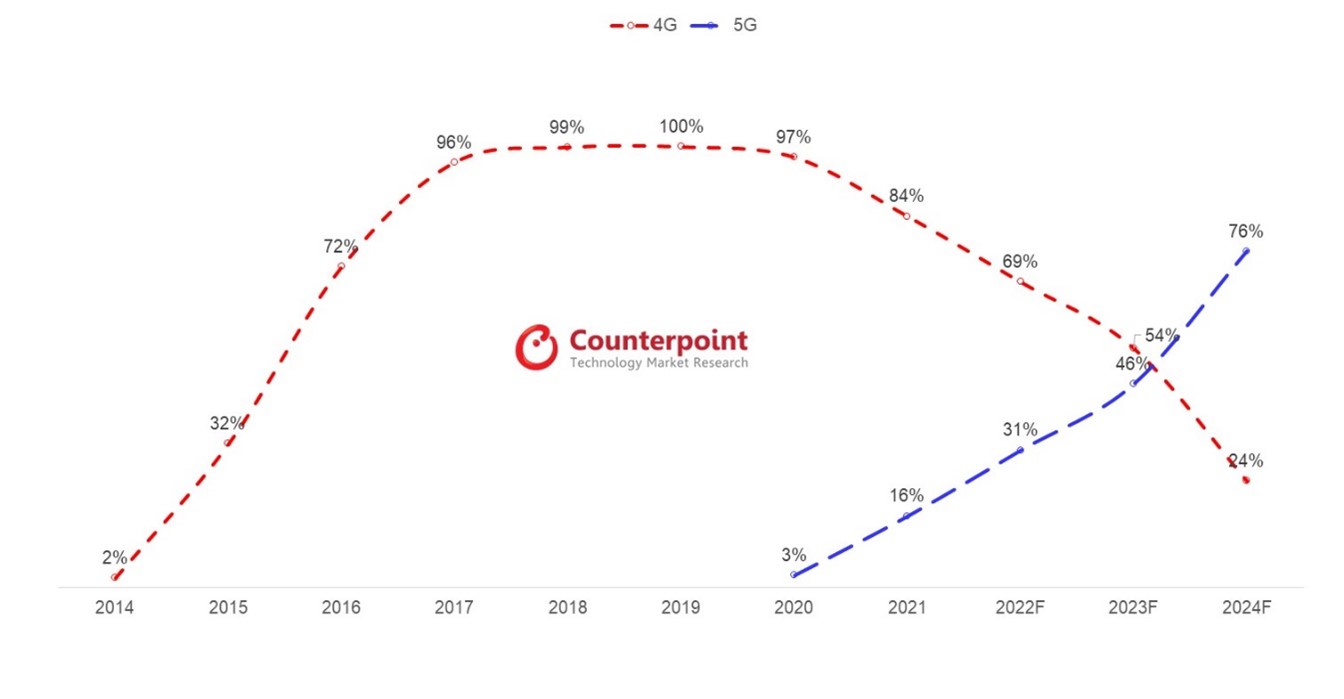

Cumulative 5G smartphone shipments will cross the 100-million mark in Q2 2023 and exceed 4G smartphone shipments by the end of 2023.

India’s 5G smartphone shipments are estimated to grow 81% YoY in 2022 driven by their expanding presence in lower price bands (<INR 20,000 or ~$244) and rollout of 5G networks.

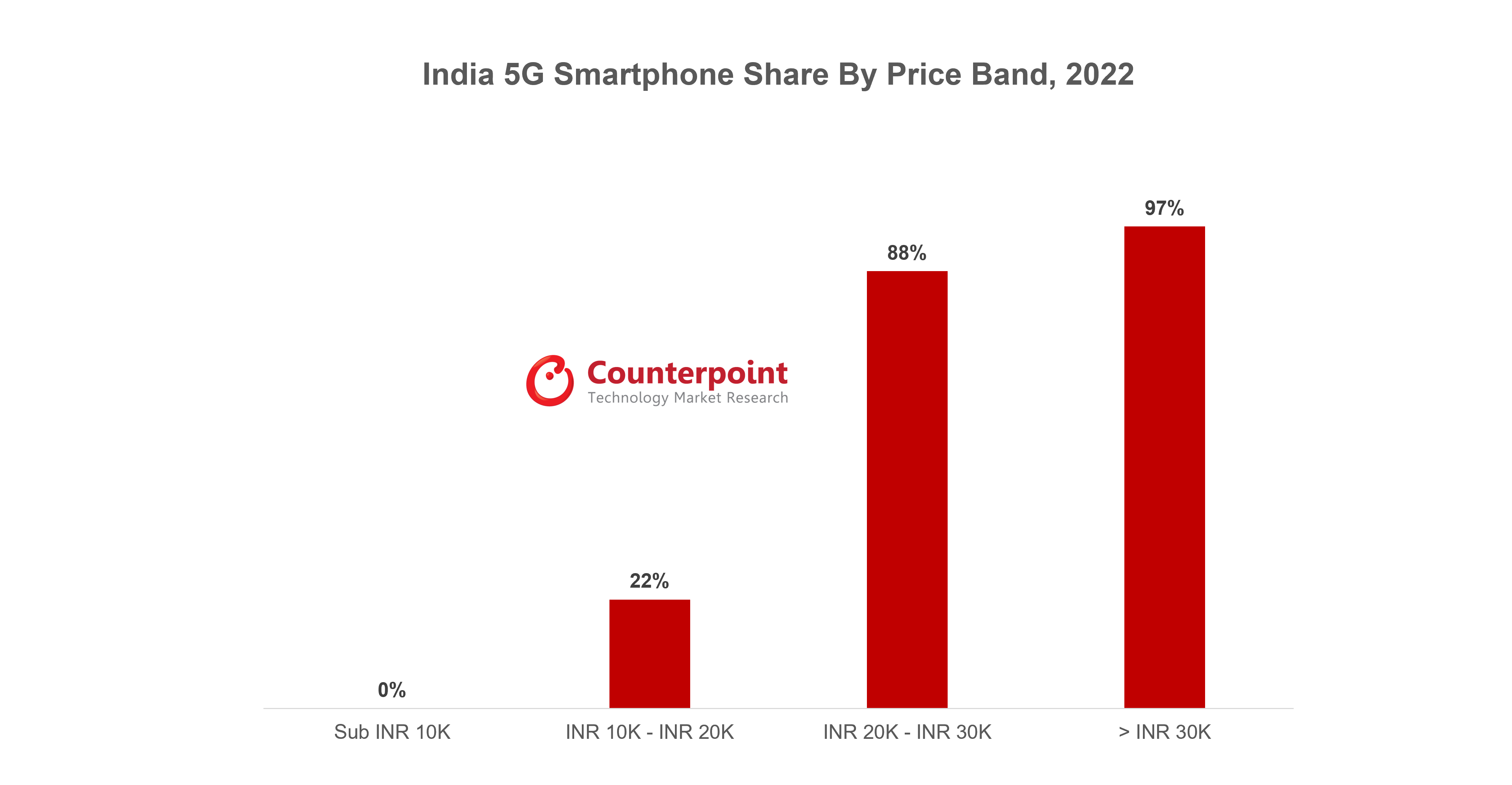

5G share in lower price bands (<INR 20,000 or ~$244) is gradually increasing, from 4% in 2021 to 14% in 2022.

India’s smartphone shipments are projected to witness a yearly decline in 2022 due to macroeconomic factors affecting consumer demand in the entry and budget segments. However, 5G has been a driving force and will continue to push smartphone demand in 2023 as well. India’s 5G smartphone shipments are estimated to grow 81% YoY in 2022 driven by their expanding presence in lower price bands (<INR 20,000 or ~$244) and rollout of 5G networks in the latter half of the year.

According to Counterpoint’s India Market Outlook, cumulative 5G smartphone shipments will cross the 100-million mark in Q2 2023 and exceed 4G smartphone shipments by the end of 2023. Our latest consumer study also reveals that 5G is the third most important factor for future smartphone purchases.

India 5G vs 4G Smartphone Shipment Penetration

Source: Counterpoint Research India Smartphone Outlook, November 2022

5G share in lower price bands (<INR 20,000 or ~$244) is gradually increasing, from 4% in 2021 to 14% in 2022. It is expected to reach 30% in 2023. The cost of an entry-level 5G smartphone came down to below INR 10,000 (~$122) in 2022 with the launch of the Lava Blaze 5G. The availability of cheaper 5G chipsets from Qualcomm and MediaTek has enabled OEMs to launch more 5G devices in the lower price segment, while the commercial rollout of 5G services has also driven demand for the same.

Source: Counterpoint Research India Smartphone Outlook, November 2022

However, the growth here has been limited due to component supply shortages, inflation, geopolitical conflicts and other macroeconomic issues, which have delayed 5G device launches in the budget segment. Though OEMs have brought more 5G devices for lower price bands (<INR 20,000 or ~$244), they have done so by dropping or downgrading other key features like display or fast charging to lessen the impact of increasing component costs. This, in turn, has affected the consumer demand for 5G within this price tier. The limited availability of 5G networks has also affected the demand.

We expect these constraints to ease by the end of 2023, leading to the mass adoption of 5G. Better availability of networks in major areas will also facilitate 5G smartphone growth in 2023, which is estimated to be 62% YoY.

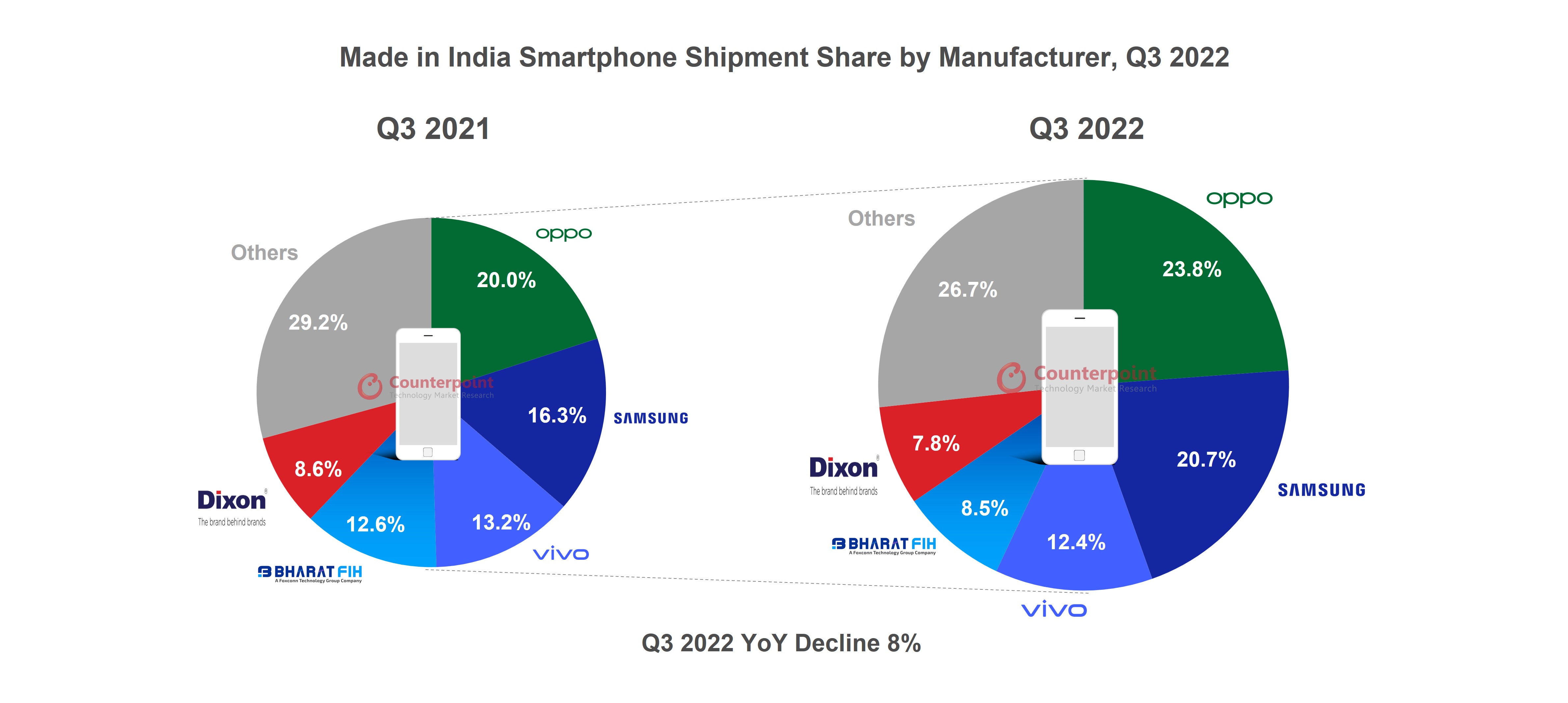

OPPO led the ‘Made in India’ smartphone shipments with a 24% share, followed by Samsung.

Bharat FIH remained the top EMS player in terms of smartphone shipments.

Among Indian players, Dixon emerged as the top smartphone EMS provider.

New Delhi, Hong Kong, Seoul, London, Beijing, San Diego, Buenos Aires – December 27, 2022

‘Made in India’ smartphone shipments declined 8% YoY in Q3 2022(July-September) to reach over 52 million units, according to the latest research from Counterpoint’s Made in India service. This is the first decline reported this year. Economic headwinds that led to a decline in consumer demand, and market uncertainties due to geopolitics were the prime reasons for the contraction.

Commenting on the local manufacturing ecosystem, Senior Research AnalystPrachir Singh said, “The Made in India smartphone shipments declined in Q3 2022 as compared to Q3 2021. Two major forces impacted the growth of such smartphone shipments. First, the decline in consumer demand, especially in the entry-level segment, due to the negative macroeconomic indicators. Second, the high channel inventory at the start of the quarter also impacted the manufacturing during the quarter. The country’s smartphone manufacturing ecosystem continues to grow with almost 63% of such shipments coming from in-house manufacturers and 37% from third-party EMS players. OPPO led the Made in India smartphone shipments in Q3 with a 24% share, followed by Samsung and vivo. BYD and Lava were the fastest-growing manufacturers in terms of smartphone shipments. Further, we will continue to see PLI disbursements in subsequent quarters, which will add to the local manufacturing landscape. Overall, the manufacturing trend is witnessing an upward trajectory with multiple partnerships happening in recent months, like the ones between Tata Group and Wistron and between Foxconn and Vedanta.”

Source: Counterpoint Made in India Research, Q3 2022 Note: Figures may not add up to 100% due to rounding

On the Indian government’s focus, Research Analyst Priya Joseph said, “On the regulatory front, despite the adverse global climate, the Indian smartphone market has remained resilient. The government’s efforts to bring about a supply chain shift and make India a manufacturing hub with constant policy interventions in the form of PLI schemes has helped the country to attract major global players across the value chain. Further, the government is actively pursuing the target of expanding the local value addition from the present 17-18% to 25% in the near future.”

Looking ahead, we believe that the manufacturing volumes will grow with an increasing focus of the OEMs to export to other countries. Increasing local value addition and exports have been the main focus points of the government under the ‘Make in India’ scheme.

Notes:

OPPO manufactures smartphones for OPPO, realme and OnePlus.

Bharat FIH manufactures smartphones for Xiaomi.

Dixon Technologies manufactures smartphones for Samsung.

Dixon Technologies’ share does not include Padget Electronics.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

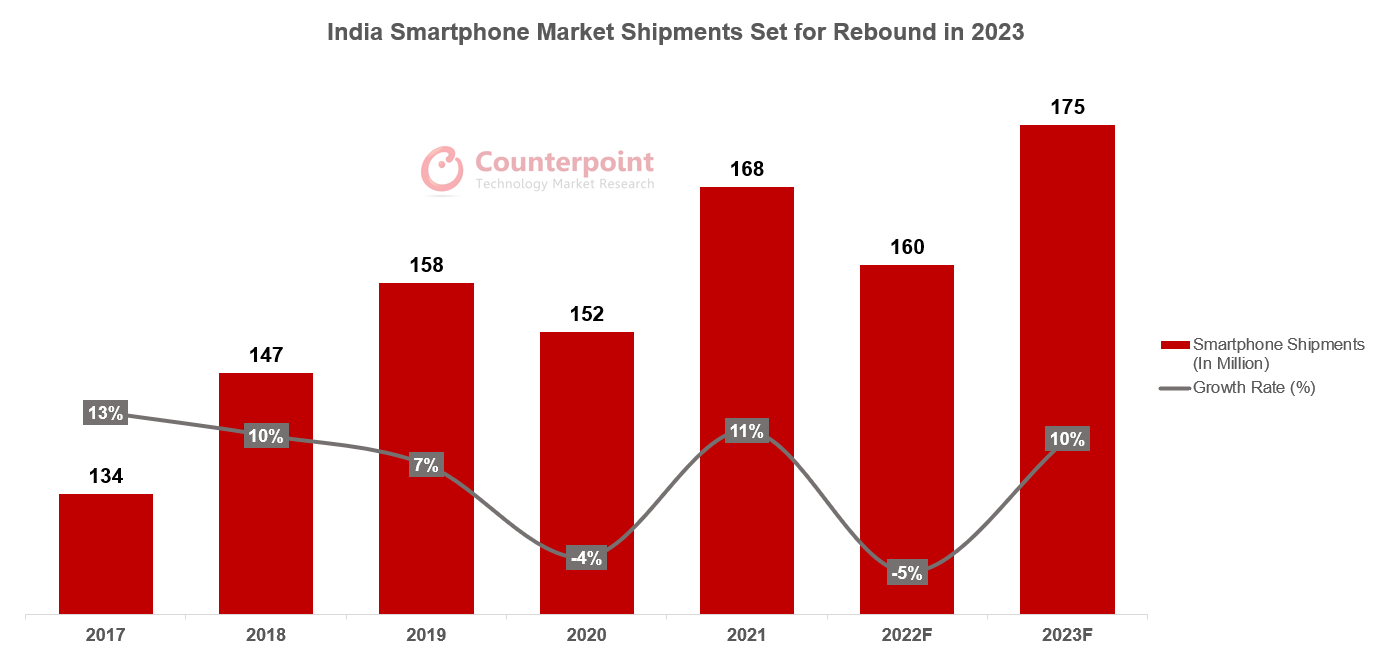

India’s smartphone shipments are expected to fall 5% YoY in 2022, dipping for the second time in the last three years.

Weak demand in entry-level segments hit sales even as the premium segment continued to grow.

The market is expected to grow by 10% in 2023 to reach 175 million units.

New Delhi, London, Hong Kong, Seoul, Beijing, San Diego, Buenos Aires – December 22, 2022

India’s smartphone shipments are expected to fall 5% YoY in 2022, according to Counterpoint Research’s latest projections. The inflationary macro environment, component shortages and rise in their prices, and wild cards like the Russia-Ukraine war and weakness in the overall global economy affected the smartphone market globally, including in India.

The Indian market has seen a steady rise in the last five years barring the COVID-19-hit 2020 to grow 1.5 times from 2016 to 2021. The market is projected to grow 10% in 2023 to reach 175 million units.

What happened in 2022?

The market failed to meet expectations in 2022. It started the year with component shortages. But even as the situation resolved on the supply side by the first half of 2022, the consumer demand did not improve as expected. The weak demand was especially felt in the entry and mid-level price bands owing to the increase in retail prices due to the rise in component prices and inflationary macro environment. The premium market continued to grow in 2022 with the >INR 30,000 ($400) price band reaching a new high. The continued premiumization of the market is the main reason why it saw positive revenue growth with the highest-ever average selling price (ASP) of close to INR 20,000 ($250).

High installed base: India currently has more than 600 million smartphone users, a number which is expected to grow over time as more feature phone users migrate to smartphones. The replacement demand from these users will drive the market in 2023 and beyond.

5G push: 5G networks are now live in multiple cities. Even though 5G smartphones have been making news in the market, they will account for just one-third of the market in 2022. 5G has been high on Indian consumers’ wish lists and with 5G networks now being available, many consumers will replace their 4G smartphones in 2023.

Government purchase of smartphones to push sales: The state of Rajasthan has rolled out a tender for the acquisition and distribution of smartphones among women in 2023.

Improvement in macro environment: We also expect the inflationary macro environment to get better next year. Therefore, consumers who postponed buying a new phone in 2022 will be able to buy a new one in 2023.

Long-term outlook remains positive

Despite the dip in 2022, India’s smartphone market has been resilient and performed better than many other regions. A large installed base, feature phone-to-smartphone migration, local smartphone production, development of supply chain and the emergence of newer use cases will continue to grow the market in the longer term.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

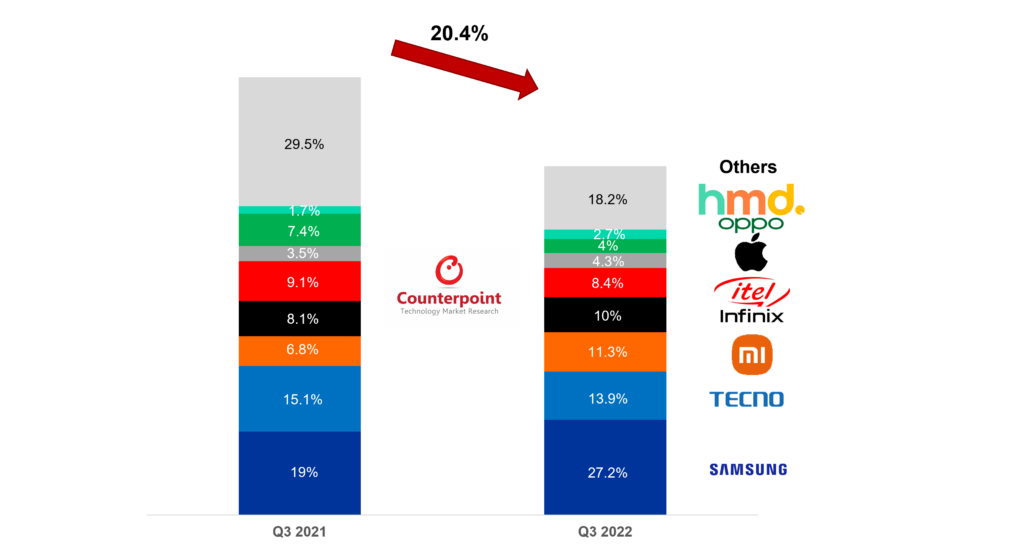

MEA smartphone shipments retreated 20.4% YoY and 12% QoQ in Q3 2022 to 35 million units.

This was the lowest level since Q2 2020, or since the start of the COVID-19 pandemic.

Samsung’s shipments and market share increased YoY as the new A-series models continued to gain momentum.

Transsion Group’s shipments led the market downturn, mainly due to TECNO and itel’s aggressive destocking efforts. Infinix, on the other hand, remained resilient to market headwinds.

Xiaomi returned to growth as product availability improved, while its exposure to the Middle East market benefitted from improving sentiment.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – December 19, 2022

Smartphone shipments in the Middle East and Africa (MEA) region fell 20.4% YoY and 12% QoQ to 35 million units in Q3 2022, according to the latest research from Counterpoint’s Market Monitor Service. Compared to the previous quarter, the macro situation continued to worsen as inflation undermined consumer sentiment, while OEMs became ever more cautious in areas such as distribution expansion, marketing efforts and stock management.

MEA Smartphone Quarterly Unit Shipments

Source: Counterpoint Research Market Monitor, Q3 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding.

Commenting on the market’s performance, Senior Analyst Yang Wang said, “The biggest issue in the smartphone market, and indeed any consumer market, this year has been macro issues. We saw no let-up in inflationary pressures and currency headwinds in the MEA market in Q3 2022. Consumer sentiment continued to be bleak, leading to OEMs and distributors cutting market spending. On the other hand, high inventory levels forced market participants to adopt destocking measures, hurting profit margins. Despite this, the 20% YoY drop probably exaggerated the gloominess in the market, as Q3 2021 was an especially successful period for the region.”

Within the MEA region, the Middle East fared better due to the GCC countries’ resilience. High inflows of energy revenues buttressed state coffers, which strengthened local currencies and kept inflation down. The region was also boosted by sales events associated with the World Cup, which is being held in Qatar since November. On the other hand, roughly 8 in 10 countries in Africa saw inflation accelerating in Q3, according to Counterpoint estimates. Persistent energy supply issues, as well as worries about another round of food shortages, kept consumers ever more cautious. We believe there is further room for inflation rates to rise in Africa towards the end of the year.

MEA Smartphone Unit Shipments Share, Q3 2022 vs Q3 2021

Source: Counterpoint Research Market Monitor, Q3 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding.

In terms of the MEA smartphone market’s competitive landscape, the biggest takeaway from the quarter was that while the economic downturn hurt most players, smaller brands disproportionately suffered more, as seen from the dramatic loss of market share. During this period of rising costs and worsening market sentiment, smaller brands faced mounting supply challenges. Maintaining cost discipline meant slashing spending elsewhere, such as marketing and distribution, and smaller players were unable to keep up with the bigger OEMs.

Market leader Samsung saw YoY volume and market share growth, as its supply issues subsided, while the Galaxy A series’ 2022 iterations continued to gain momentum. Samsung continues to be the best-placed OEM in the region as its broad product portfolio covers every customer segment. The brand is well-positioned to capture market volume when the economic issues ease.

Transsion Group brands continued to take the MEA region’s biggest share of smartphone shipments. However, its exposure to the lower-value segments, particularly in Sub-Saharan Africa, meant that it faced the strongest headwinds among the big brands. We noted aggressive destocking efforts during the quarter, mostly concentrated within the lower-end TECNO and itel brands. On the other hand, Infinix continued to perform well as its 2022 models ticked all the boxes. We believe Transsion may stage a rebound towards the end of the year, as the company prepares for higher-end launches for the TECNO and Infinix brands.

Xiaomi captured the third spot among OEMs, as supply issues disappeared in the rear-view mirror. The company’s affordable mid-range products, particularly the Redmi Note 11 and Redmi 10 series, remained popular among price-conscious customers, while its business received a boost due to favorable conditions in the Middle East region.

Apple continued to gain market share in the region, largely due to improving distribution across the region. The iPhone 13 series appeared regularly among the best-selling models in the region, even during the last months of the iPhone 13 cycle. We expect Apple’s volume and market share to increase further in the next quarter as the iPhone 14 sales begin to gain momentum.

While the end-of-year shopping season is expected to deliver a boost to the smartphone market, sales increases are unlikely to match the levels seen last year, as affordability will continue to be first and foremost among customers’ concerns. Macroeconomic headwinds and geopolitical uncertainties may well persist into 2023, but we do expect a small rebound in the MEA smartphone market next year. Economies in MEA have fared better than those in developed countries, and the second half of 2023 may see a release of pent-up demand, just as post-COVID-19 reopening spurred a period of consumer optimism.

Counterpoint Research’s market-leading Market Monitor, Market Pulse and Model Sales services for mobile handsets are available for subscribing clients.

Feel free to contact us at press@counterpointresearch.com for questions regarding our in-depth research and insights.

You can also visit our Data Section (updated quarterly) to view the smartphone market share for World, USA, China and India.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

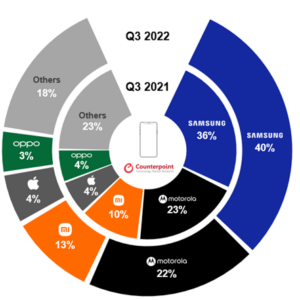

LATAM smartphone shipments decreased 13% YoY and 17.3% QoQ in Q3 2022.

All the top brands’ volumes declined QoQ, except for OPPO.

Samsung led the market with a 40% share, followed by Motorola with a 22% share.

The >$700 price band saw the highest growth.

Buenos Aires, New Delhi, Hong Kong, Seoul, London, Beijing, San Diego – December 12, 2022

The Latin American and Caribbean smartphone shipments fell 13% YoY and 17.3% QoQ in Q3 2022, according to the latest research from Counterpoint’s Market Monitor service. All the top brands’ volumes declined QoQ, except for OPPO.

Commenting on the market, Principal Analyst Tina Lu said, “Q3 2022 shipments were impacted by high inventories carried over from Q2 2022. During the previous quarter, several OEMs pushed high shipment volumes, but consumer demand was slowing down. Therefore, it resulted in excess inventories in most sales channels, and Q3 2022 mainly corrected it. But still, the issue has not been completely fixed and the sales channels will feel the pain of higher-than-acceptable inventories in Q4 2022 too.”

Lu added, “Consumer demand remains weak in LATAM. The regional economic crisis, triggered by high inflation, currency depreciation and a change in political power, resulted in a sharp decrease in consumer demand. OEMs, operators and retailers have all launched aggressive promotional bundles or double-digit discounts to increase sales.”

Research Analyst Andres Silva noted, “Samsung and Xiaomi were the biggest share gainers YoY during the quarter. Samsung remained the absolute leader in the region and all the individual countries. Xiaomi continued to grow by entering new countries and expanding both the operator and its own retail channels. This drove Xiaomi’s share and shipment volume growth in the region.”

Commenting on the price band performance, Silva said, “Despite the economic crisis, the >$700 price band saw the highest growth. Apple and Samsung’s flagships drove the growth of this segment. On the other hand, the <$150 price segment saw the biggest drop YoY, reflecting the lack of adequate entry-level smartphone supplies from the biggest brands, especially Motorola.”

Top Smartphone OEMs’ Market Share in Latin America, Q3 2021 vs Q3 2022

Source: Counterpoint Research Market Monitor, Q3 2022

Q3 2022 Market Summary

Amid weakened consumer sentiment and massive shipments in Q2 2022, Samsung’s high inventory impacted its shipments in Q3 2022. On the other hand, demand for low-end and low-to-mid-end devices remained robust, showing a flat YoY volume growth.

Motorola’s shipments fell 6% QoQ as its entry-level models were in short supply. Motorola also dropped YoY as it had an exceptional quarter in Q3 2021. The brand’s performance was particularly hit in Brazil, Argentina and Mexico. The recently launched Edge 30 flagship series also failed to click with consumers.

Xiaomi’s shipments rose 15% YoY driven by the Redmi Note 11, which has proven to be the rising star. However, high inventory in operator channels and low demand in certain countries like Peru resulted in a QoQ shipment drop.

Apple saw only a slight volume decrease YoY despite the launch of the new iPhone. But the iPhone 14 was launched late in the region even as Colombia imposed restrictions on 5G iPhone imports. The good demand for the iPhone 11 helped soften the fall. Apple is expected to improve its performance over the next quarter.

OPPO’s share rose one percentage point QoQ driven by the launch of the new Reno 7 in the region. Mexico and Colombia helped the brand navigate overall market softness.

The region’s smartphone market is becoming more concentrated. The top three brands represented 69% of the shipments in Q3 2021 and 75% in Q3 2022. While the new Chinese entrants are facing a tough time in such a market, it is the regional and smaller brands that are suffering the most.

The “others” category decreased in volume and share YoY. Big brands, with their deeper pockets for promotions and better negotiation power, are making it tough for smaller brands.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Source: Counterpoint Research India Smartphone Outlook, November 2022

Source: Counterpoint Research India Smartphone Outlook, November 2022 Source: Counterpoint Research India Smartphone Outlook, November 2022

Source: Counterpoint Research India Smartphone Outlook, November 2022