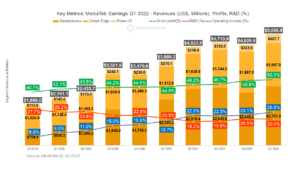

MediaTek recorded an impressive set of numbers for Q1 2022 with revenues growing 32% YoY and 10.2% QoQ to reach $4.8 billion. The company’s mobile phone segment achieved a revenue of $2.7 billion, growing 29% YoY. According to Counterpoint Research’sSmartphone, AP/SOC Shipment Tracker, the addition of the Dimensity 9000 to the premium segment has added meaningfully to the overall revenues that have also been driven by 5G AP/SOCs in the mid-tier segment. LTE AP/SOCs are still attracting high demand and will be in tight supply throughout 2022. Based on our data, LTE AP/SOCs contributed to one-third of the total AP shipments in Q1 2022.

MediaTek Revenue by segment

The smart edge segment contributed 39% to MediaTek’s Q1 2022 revenues. This segment is mainly driven by the Wi-Fi 6/6E migration and higher-end solutions for smart TVs and tablets. Technology migration trends in smart edge platforms have led to a higher blended ASP in this segment.

The power IC segment accounted for 8% of the total revenues, growing 52% YoY and 21% QoQ. A large part of the PMIC segment’s revenue is coming from displays and smartphones. Automotive and industrial applications contribute to 10% of the PMIC revenue and will drive growth for this segment in 2022.

MediaTek guided revenues to be in the range of $5-$5.3 billion in Q2 2022, up 3~10% QoQ and 17~25% YoY. The mobile phone segment will show the strongest growth due to the shifting of demand from LTE to 5G AP/SOCs. As the China market is slowing, the revenue growth will come from other regions like India and Europe. Also, the Dimensity 9000 and 8000 series will continue to add to the revenues in Q2 2022. However, due to the slowdown in China and deteriorating macroeconomic conditions, we have reduced our H2 2022 forecast for the Dimensity 9000.

Revenues from Wi-Fi 6, 5G SIM modem, 5G tablet, 10G-PON and 4K smart TV are also expected to grow strongly in H2 2022. Also, MediaTek’s mmWave SOC is on schedule to ship in the second half of 2022. It will pave the way for MediaTek’s further expansion in the global market.

According to Counterpoint Research’s Smartphone AP/SOC Shipment Tracker, MediaTek will continue to lead the smartphone AP SOC market with a volume share of 41% in Q2 2022, followed by Qualcomm with 27%. The company’s strategy of 5G, Wi-Fi 6, focused product migration, geographic expansion with global customers, and penetration into high-end and flagship segments will allow MediaTek to retain and even improve its strong market position.

China slowdown, COVID-19 lockdowns and macroeconomic conditions will affect the global smartphone market. MediaTek guides flat growth for the smartphone market in 2022 and 5G penetration (660-680 million units) reaching 50%. Further, 5G penetration is expected to reach 70% in the next two years.

Smartphone OEMs like OPPO, vivo and Xiaomi currently have inventories with distributors and also for components like AP/SOCs, PMICs and DDICs. This has led to a drop in AP/SOC orders for MediaTek for H2 2022. But MediaTek is keeping a high inventory reserve this quarter to sustain its OEM and ODM partners during the worsening COVID-19 situation. MediaTek normally runs with around 90 days of inventory. But it has now raised this to around 100 days to manage potential supply constraints.

MediaTek sought to reassure investors that it would not follow a low pricing strategy to counter slowing demand. Instead, it will invest in future growth. Its pricing strategy will also leverage its high capacity and will manage profitability by maintaining similar pricing as the previous quarter. We expect overall 5G AP/SOC ASPs to be flat compared to last year. If the competition reduces the prices, it will be challenging for MediaTek to maintain growth in H2 2022. Due to the strong demand for LTE AP/SOCs, the ASPs will not decline this year. Overall, 5G AP/SOCs will have a premium pricing over LTE. The company is now focusing on developing 5G AP/SOCs for low-end phones priced less than $150. We believe this will happen two years down the line. However, based on our estimates, LTE is going to dominate the less than $100 smartphones, driven by regions like LATAM, Africa and APAC.

Presently, MediaTek is not a big player in the PC business, having only a few Chromebook-type devices in the market. The company played down its expectations for substantial growth in the PC sector while confirming that it was interested in the potential of the Arm-based PC market.

Smartphones still contribute 53% of the revenues for MediaTek. For longer-term growth, MediaTek has to reduce dependence on smartphones and expand into areas like the smart edge, automotive, connected PCs and AR/VR.

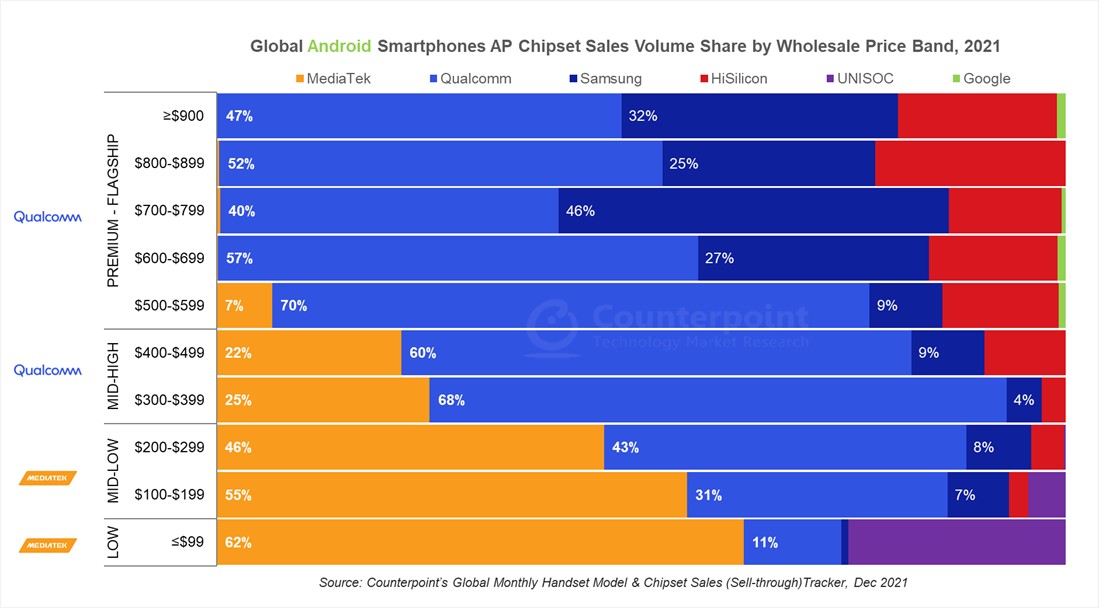

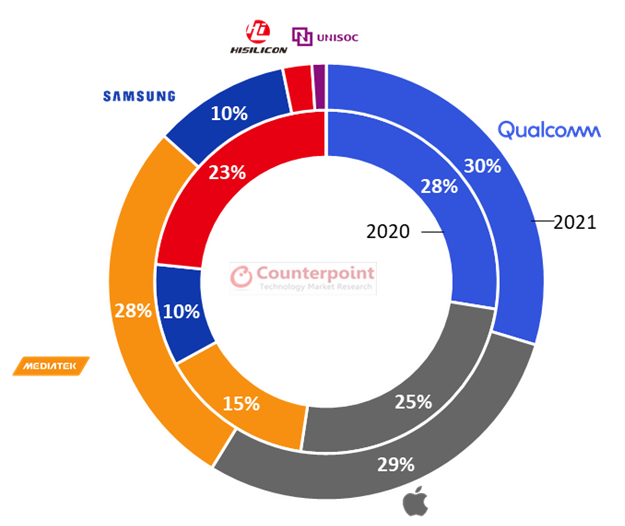

The global Android smartphone AP (Application Processor)/SoC (System on Chip) sales grew 3.6% YoY in 2021, according to the latest research from Counterpoint’s Global Handset Model Sales Tracker. MediaTek led the Android smartphone SoC market in 2021 with a 46% share, followed by Qualcomm with 35%. Most of the market share growth for MediaTek in 2021 came from the low-mid tier wholesale price segment (sub-$299), driven by strong demand for the Dimensity 700/800 series chipsets.

Qualcomm struggled with a tight supply throughout the year for its mid-tier solutions. The shift in focus away from 4G SoCs also didn’t help. However, in the high value $300+ segment, Qualcomm continued to dominate with its Snapdragon 7 and 8 series. The number of design wins for Qualcomm in the $399+ Android smartphones continued to climb not only for chipsets (AP/SoC) but also for RFFE (RF Front End) components, allowing it to capture a higher BoM (Bill of Materials) share and boost both its top and bottom lines.

AP Chipset Share for Android Smartphones by Price Band (%) in 2021

Qualcomm

With a supply crunch since the previous year, Qualcomm prioritized focus on ramping up supply for its 7 and 8 series Snapdragon chipsets, driving higher revenue and profitability.

Qualcomm is also in a very unique position to further make inroads into the premium Android smartphone market by supplying a leading-edge RFFE portfolio and other components such as ultrasonic fingerprint sensor and quick charge.

Qualcomm continued its domination of the mid-high ($300-$499) smartphone segment in 2021 with a 65% share, up from 53% in 2020. The Snapdragon 870, 720G, 750G and 778G were the key volume-driver chipsets for Qualcomm in this segment.

Qualcomm’s share in smartphones priced above $500 increased from 41% in 2020 to 55% in 2021 owing to the launch of flagships Snapdragon 888 and 8Gen 1.

The Snapdragon 8 series sets an industry benchmark when it comes to delivering premium flagship-grade smartphone experiences. It is the default choice for any smartphone OEM’s flagship series.

Qualcomm is generations ahead of its competition when it comes to premium experiences in a chipset, whether it is compute (CPU, DSP, GPU), AI (NPU), connectivity (4G, 5G sub-6GHz, 5G mmWave, Wi-Fi6/6E), security, or gaming capabilities. Besides, the highly optimized RFFE components are key to delivering advanced connectivity experiences, making it a system-level opportunity for Qualcomm.

Moving forward, dual sourcing of premium solutions from foundry will be the key to alleviating +any concerns over chipset shortages.

MediaTek

MediaTek’s growth came from smartphones priced less than $299 (wholesale price). MediaTek’s growth was driven by both LTE and 5G SoCs across this price band.

The volume in the ≤$99 price band was driven by LTE smartphones, where MediaTek captured a 62% share. LTE SoCs were most affected by the shortages in 2021, both for MediaTek and Qualcomm.

In Android smartphones in the $100-$299 price band, MediaTek dominated the market with a 52% share. This is where the Dimensity 700 and 800 drove the mass-market adoption of 5G smartphones in markets such as China, India and parts of the US and Europe. This allowed brands such as realme, Xiaomi, OPPO and vivo to launch 5G phones at price points below the $200 retail price.

The Dimensity 1100/1200 helped MediaTek increase share in the $300-$499 price band, where it captured a 24% volume share in 2021, compared to 6% in 2020.

Further, with the launch of the Dimensity 8100/8000, it is looking to strengthen its position in the $300-$499 price band. These chipsets support the R16 baseband with power efficiency and performance improvements. With the Dimensity 9000, MediaTek is looking to enter the premium segment ($500+) in 2022. Almost all Chinese smartphone OEMs, like OPPO, vivo, Xiaomi and HONOR, will launch phones with this chipset. According to our chipset tracker forecast, MediaTek is likely to capture around 10% of the premium smartphone segment.

Samsung

Samsung SOCs witnessed a decline in all smartphone price segments in 2021 compared to the previous year.

Drastic changes were seen in the low-mid segment ($100-$299), where its share decreased from 17% to 7%, and in the mid-high segment, where its share decreased from 13% in 2020 to 6% in 2021, as Samsung Mobile outsourced many of its models (A, F and M series) to ODMs which integrated mostly Qualcomm, MediaTek or Unisoc solutions in different models depending on target price bands. The lack of refreshes in the Exynos series SoCs for the mid-to-high tiers was a trigger for the ODM move. The absence of the Note series and Qualcomm’s design wins across the popular Samsung foldables led to further decline of the Exynos chipsets.

With the Galaxy S22 series, Qualcomm has a greater proportion of design wins across markets than before, thanks to its industry-leading offerings and also the low yields of the new premium Exynos chipsets.

UNISOC

UNISOC showed exciting growth in 2021 in smartphones priced less than $200. In 2020, UNISOC chipsets only catered to phones priced under $100. In 2021, realme, HONOR, Motorola and Samsung launched phones with the Tiger series SoC. UNISOC has expanded its customer base with design wins at ZTE and TECNO, and entry into the Samsung Galaxy A series.

UNISOC captured a 26% share in the ≤$99 band in 2021, followed by a 4% share in the $100-$199 price band.

For 2022, we expect UNISOC to maintain the momentum with its portfolio catering to LTE smartphones as MediaTek struggles with supply issues for 4G chipsets and Qualcomm focuses just on 5G solutions. Also, a few design wins with 5G chipsets will add to the overall volumes.

HiSilicon

HiSilicon’s SoCs had a 16% share in phones costing $500 and above in 2021, which was a decline from the 30% share in the previous year, due to the US trade ban. It is running on the inventory it added before the ban.

For 2022, we expect its volumes to drop as the inventory gets depleted. Huawei has already started using Qualcomm SoCs in its new launches, but they are limited to 4G.

Qualcomm’s share reached 30% driven by the premium tier.

UNISOC had a strong Q4 with its share reaching 11%.

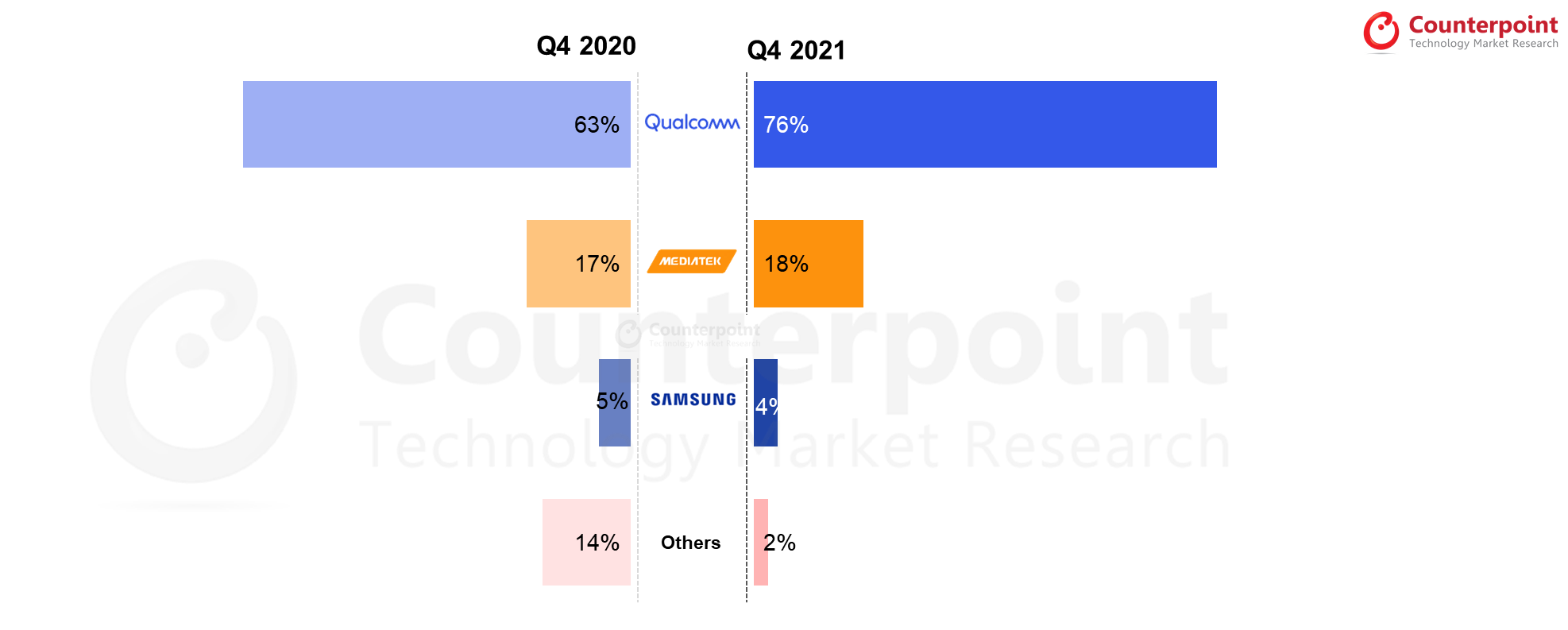

Qualcomm led the 5G baseband market with a 76% share.

Seoul, Taipei, Beijing, New Delhi, London, Boston, Toronto, Hong Kong – February 24, 2022

The global smartphone AP (Application Processor)/SoC (System on Chip) chipset shipments grew 5% YoY in Q4 2021, according to the latest research from Counterpoint’s Foundry and AP/SoC service. 5G smartphone SoC shipments were almost half of the total SoC shipments.

Research Director Dale Gai said, “MediaTek led the smartphone SoC market with a share of 33%. Its smartphone SoC volumes declined this quarter due to the high shipments in the first half and inventory corrections from Chinese smartphone OEMs. Many customers had built chipset inventories to manage uncertainties in the supply situation.”

On the growth outlook, Gai added, “We expect revenues to grow in Q1 2022 driven by the flagship chipset (Dimensity 9000) for smartphones. Higher 5G penetration will offset the lower seasonal demand. The increase in chipset prices after TSMC’s wafer price hike is reflected from Q4 2021 onwards. 5G migration in regions like APAC, MEA and LATAM and continued LTE demand will help MediaTek have a strong 2022.”

Global Smartphone AP/SoC Shipment Market Share (%), Q4 2020 vs Q4 2021

Source: Counterpoint Research Quarterly AP/SoC/Baseband Shipments Tracker, February 2022

Commenting on Qualcomm’s performance, Senior Analyst Parv Sharma said, “Qualcomm recorded a very strong quarter, growing 18% QoQ and 33% YoY despite component shortages and foundry capacity not being able to keep up with demand. Qualcomm was able to prioritize high-end Snapdragon sales, which come with higher profitability and less impact from shortages than mid-end and low-end mobile handsets. The company was also able to increase supplies from its major foundry partners by dual-sourcing key products. It captured a 76% share in the 5G baseband shipments driven by Apple’s iPhone 13 and 12 series and premium Android portfolio.”

Commenting on the growth opportunities, Sharma added, “Qualcomm’s Snapdragon 8 Gen 1 flagship mobile platform will start shipping from Q1 2022. The performance in Q1 2022 will be driven by design wins in the Samsung Galaxy S22 series and launches in the Chinese New Year. Overall, the next inflexion in growth will be in H2 2022 with the launch of 5G handsets by major OEMs. The share of revenues from Android is also growing as more OEMs are adopting Qualcomm’s modem-to-antenna RFFE solution across tiers.”

Global 5G Smartphone Baseband Shipment Market Share (%), Q4 2020 vs Q4 2021

Source: Counterpoint Research Quarterly AP/SoC/Baseband Shipments Tracker, February 2022

Summary:

MediaTek led the smartphone SoC market in Q4 2021 with a 33% share. Shipments declined due to inventory correction as many customers had built inventories due to supply chain constraints.

Qualcomm grew 18% sequentially due to the premium segment and dual-sourcing from foundries. It dominated the 5G baseband modem shipments with a 76% share, driven by basebands for Apple and premium Android.

Apple maintained its third position in the smartphone SoC market in Q4 2021 with a 21% share. The iPhone 13 launch and festive season drove the shipments.

UNISOC continued with shipment growth this year and reached an 11% share in Q4 2021. On an annual basis, its SoC shipments more than doubled in 2021. It has expanded its customer base, securing design wins with HONOR, realme, Motorola, ZTE, Transsion and Samsung.

Samsung Exynos slipped to the fifth position with a 4% share as Samsung is in the middle of rejigging its smartphone portfolio strategy of in-sourcing as well as outsourcing to Chinese ODMs. As a result, the share of MediaTek and Qualcomm has been growing across Samsung’s smartphone portfolio, from the mid-range 4G and 5G models manufactured by ODMs to the flagship ones.

HiSilicon was unable to manufacture Kirin chipsets due to the US trade ban against Huawei. The accumulated inventory of Kirin SoCs is on the verge of being exhausted. As a result, Huawei is launching its latest series with Qualcomm SoCs but is limited to 4G capabilities.

For our comprehensive research on foundries to chipsets to devices, feel free to get in touch with us at the contacts given below.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Seoul, Taipei, Beijing, London, Boston, Toronto, New Delhi, Hong Kong – May 3, 2021

MediaTek to lead global smartphone SoC market with 37% share whereas Qualcomm will lead the global 5G smartphone SoC market with 30% share.

The leading-edge nodes (7nm, 6nm and 5n) will account for almost half of the smartphone shipment volume during 2021.

5G AP/SoC chipset volumes will more than double annually in 2021.

The competitive dynamics in the smartphone AP/SoC market is changing fast for the fabless SoC vendors such as Qualcomm, MediaTek, Apple and others. The market outlook for these vendors is being shaped by not only the breadth and depth of the capabilities or tiering of the chipset portfolio but also by the choice, the share of the capacities across different edge-nodes at the foundries. Global smartphone AP (Application Processor)/SoC (System on Chip) chipset shipments will grow 3% YoY in 2021, factoring in the impact of supply constraint, rapid growth of 5G smartphones and related competitive dynamics according to the latest research from Counterpoint’s Foundry & Application Processor (AP/SoC) research.

Commenting on the research, Research Director Dale Gai said, “When we break down our forecast with respect to the current demand-supply dynamics, MediaTek is likely to continue its Q4 2020 momentum into 2021 and likely to capture 37% unit share of all the smartphone AP/SoC shipped for the full the year. This 20% potential annual uptick in demand is a function of competitive 5G portfolio powering sub-$150 5G smartphones manufactured at TSMC without any supply constraint and growing share in 4G segment. Further, MediaTek in the first half of 2021 will benefit from Qualcomm’s current supply constraints around RFICs (radio-frequency integrated circuits) from Samsung’s Austin fab, Power management ICs (PMIC), and relatively lower 5nm production yields.”

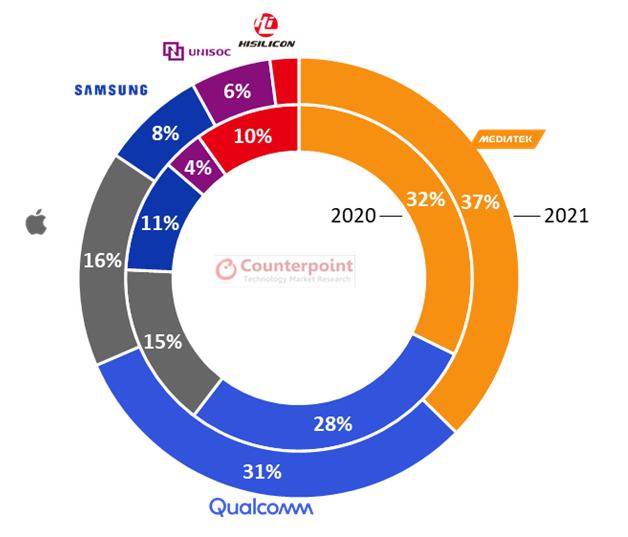

Exhibit 1: Global Smartphone AP/SoC Market Share (%) Outlook

Global smartphone chipset share

Source: Counterpoint Research – Foundry & SoC Outlook, Apr 2021

Mr Gai, added, “However, we believe Qualcomm to bounce back strongly in H2 2021, firstly by securing greater capacity at TSMC to boost its 5G-centric tiered Snapdragon portfolio. Secondly, taking key steps to improve the supply of PMICs and RFICs should alleviate the supply constraints in coming months. This will allow Qualcomm to maintain its leadership in 5G SoC market and overall market share of 31% still growing annually.”

Highlighting the importance of leading-edge nodes and securing capacities for the same, Mr Gai noted, “The leading-edge nodes, including 7nm, 6nm and 5nm, will account for almost half of the smartphone shipment volume in 2021. These leading nodes are mainly for 5G smartphone models, as advanced nodes (e.g., 11/12/14nm at TSMC and Samsung) will serve the mainstream 4G LTE chipsets in 2021.”

Exhibit 2: Global 5G Smartphone AP/SoC Market Share (%) Outlook

5G smartphone chipset forecast

Source: Counterpoint Research – Foundry & AP/SoC Outlook, Apr 2021

Commenting on the growth of 5G smartphone chipsets, Research Analyst Parv Sharma highlighted, “We estimate Qualcomm to increase its 5G SoC market share to grow to 30% mark in 2021, with 5G solutions across the tiers, from Snapdragon 8-series down to 4-series. If you include 5G baseband shipments to Apple, the overall 5G chipset market share jumps to 59% level. In an ideal scenario, Qualcomm’s market share in 5G segment would have been even higher if it did not face the unfortunate supply constraints in the first half of 2021. As Qualcomm turns to place more wafer orders on TSMC’s 6nm/5nm from Q2 2021, following the below-expectation wafer output of the Snapdragon 888 in the beginning of the year, we expect it to resume its 5G SoC shipment growth from H2 2021.”

Mr. Sharma further adds, “MediaTek leveraging TSMC and its affordable 5G portfolio is well-positioned to almost double its market share in 5G smartphone SoC/AP segment. Together, MediaTek and Qualcomm occupy nearly two-thirds of the 5G smartphone SoC market demand, but the gap between the two has narrowed. Having said that, the foundry capacity will continue to remain tight till early 2022, before the next wave of CAPEX realizes at the leading nodes.”

For our comprehensive research on foundry to chipsets to devices, feel free to contact us at the contacts below.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Analyst Contacts:

Dale Gai

Parv Sharma

Follow Counterpoint Research

press(at)counterpointresearch.com

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.