One of the major challenges to the adoption of open RAN in 5G networks in dense, urban environments is its sub-optimal support for massive MIMO radios. While there are several reasons behind this performance deficit, a key reason is that the O-RAN Alliance 7.2x open fronthaul specification was not originally designed to accommodate massive MIMO radio systems. Recently, the O-RAN Alliance announced a new fronthaul interface specification designed specifically for use with massive MIMO radio systems in dense, high-traffic environments.

This Technology Report provides an objective analysis of the O-RAN Alliance’s Next Generation Lower-Layer Split (LLS) and discusses the implications of the new interface on the adoption of open RAN massive MIMO radios.

Key Takeaway 1: Impact of Incumbents

With the availability of the new NG-LLS fronthaul split, it “appears” that the open RAN community has united around a single specification which will enable open RAN to be adopted in high-traffic urban regions. This should be welcome news as it means that operators will be able to use open RAN technology across all parts of their networks, from rural deployments to dense, high traffic urban environments. However, the NG-LLS standard has brought major incumbents such as Ericsson and Nokia into the open RAN limelight. While this brings scale and credibility to open RAN in the high-end 5G market, it also raises questions about open RAN’s goal of diversifying the radio supply chain and lowering barriers to smaller vendors.

Key Takeaway 2: Massive MIMO Use Cases Suitable for Split 7.2b

Although Split 7.2b has limitations when deployed in dense, high-traffic urban networks, Counterpoint Research believes that it will continue to be a good choice for other mMIMO use cases. For example, in uses cases with moderate traffic loads, where cell sizes are larger and where end-user mobility is low such as in Fixed Wireless Access applications. Radios based on Split 7.2b will also benefit from reduced complexity and lower costs compared to NG-LLS based radios. In future, the application of advanced AI/ML algorithms in the DU may narrow the performance differential between Split 7.2b and NG-LLS for some use cases.

In today’s rapidly evolving telecommunications landscape, the significance of digital transformation for Mobile Virtual Network Operators (MVNOs) cannot be overstated. As the industry witnesses a surge in technological advancements and changing consumer expectations, MVNOs face unprecedented opportunities as well as challenges. Digital transformation serves as the catalyst that empowers MVNOs to remain competitive, enhance customer experiences, streamline operations, and unlock new revenue streams.

This whitepaper looks at the changing MVNO landscape and how MVNOs can go “DIGITAL” – Differentiated, Intelligent, Growing, Integrated Telco that is Agile and always Listening.

• MVNO landscape • Why should MVNOs go digital? • Challenges faced by MVNOs for digital transformation • What can MVNOs do? • Test how DIGITAL is your MVNO?

In some markets, operators await evidence of successful use cases before switching to 5G SA.

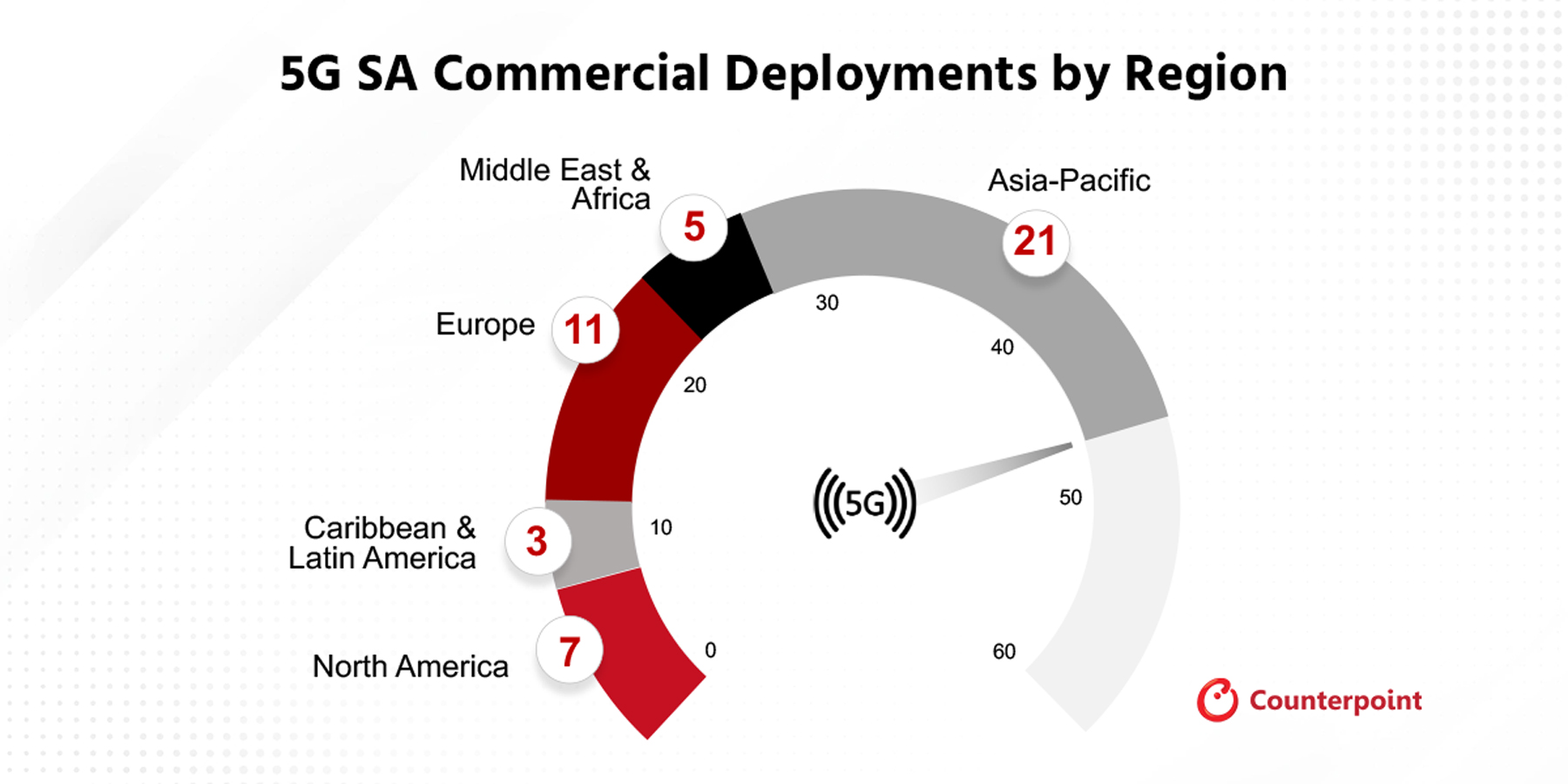

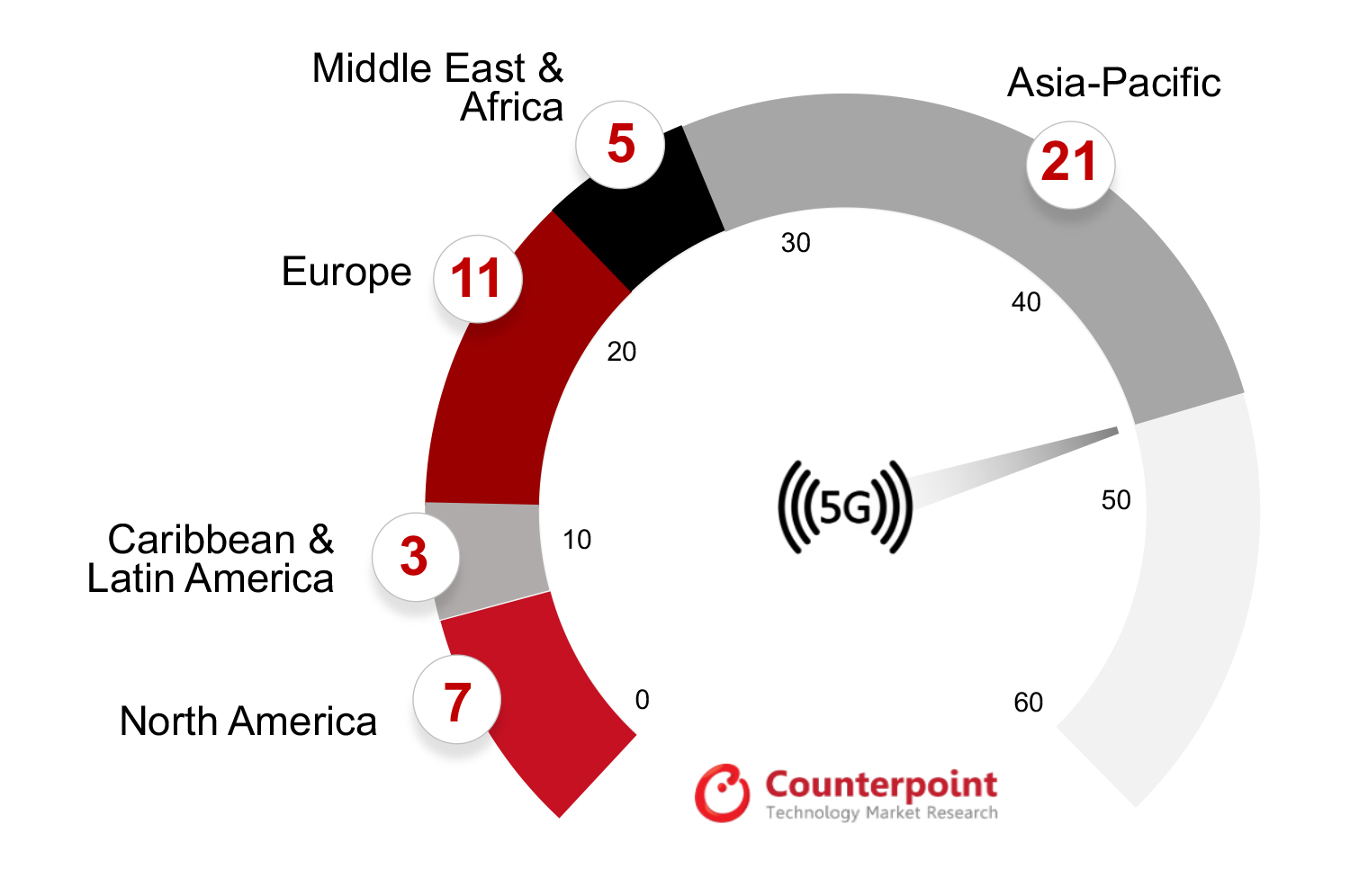

In H1 2023, the Asia-Pacific region continued to lead in terms of 5G SA Core deployments.

Ericsson led the overall market followed by Nokia, Huawei, ZTE, Samsung, and Mavenir.

Counterpoint Research’s recently published July update of the 5G SA Core Tracker is a culmination of an extensive study of the 5G SA market. It provides details of all operators with 5G SA cores in commercial operation at the end of H1 2023, including market share by region, vendor, and the popular frequency bands for deployments. Apart from that, it touches upon the potential monetization opportunities for telecom operators across different domains and uses cases.

Last year, there was steady growth in the commercial deployment of 5G Standalone (SA), with more than 20 operators moving to 5G standalone core. However, the pace slowed down in H1 2023 with the number of operators launching commercial 5G SA ranging in single digits. The primary reason for the slowdown in commercial deployment of 5G SA was the restraint arising from global macroeconomic factors and the lack of a clear picture of 5G monetization for operators. Although the pace of commercial deployment has slowed down in 2023, operators are working on monetization avenues, and are working on SA-specific use cases, including on-demand network slicing and FWA.

Most of the 5G SA commercial deployments have been in developed economies, and Counterpoint Research expects the next bulk of network rollouts will take place in emerging markets. This will drive the continuing transition from 5G NSA to 5G SA.

Exhibit 1: 5G SA Deployments by Region, H1 2023

As shown in Exhibit 1, the Asia-Pacific region led the segment, followed by Europe and North America, with the other regions – Middle East and Africa, and Latin America – lagging.

Key Points

Key points discussed in the report include:

Operators – 47 operators have deployed 5G SA commercially with many more in the testing and trial phase. Globally, most of the deployments are in developed economies with those in emerging economies lagging. Although the pace of deployment is steady in developed markets, it is progressing slowly in emerging markets, and in some markets, operators are biding their time and looking for evidence of successful use cases before switching from 5G NSA to SA. The ongoing economic headwinds also delayed the commercial deployment of SA, which was seen in H1 2023.

Vendors – Ericsson and Nokia lead the 5G SA Core market globally and are benefiting from the geopolitical sanctions on Chinese vendors Huawei and ZTE in some markets. South Korea’s Samsung and Japan’s NEC are mainly focused on their respective domestic markets but are expanding their reach to Tier-2 operators and emerging markets, while emerging vendors Parallel Wireless and Mavenir are working with leading operators in Europe, and Middle East and Africa.

Spectrum – Most operators are deploying 5G in mid-band frequencies, n78, as it provides faster speeds and good coverage. Some operators have also launched commercial services in the sub-GHz n28 and mmWave wave n258 bands. FWA seems to be the most popular use case at present but there is a lot of interest in edge services and network slicing as well.

Use Cases – Operators are looking for avenues to monetize the 5G services, as they are struggling to make the RoI from their investments in 5G. Although FWA is a promised application for 5G SA monetization, there are many other use cases that operators can look into to increase their RoI, including network slicing, live broadcasting, XR applications, and private networks. Although eMBB is the most widely used 5G use case currently, MNOs need to move to 5G SA to leverage URLLC and mMTC use cases.

Report Overview

Counterpoint Research’s 5G SA Core Tracker, July 2023 provides an overview of the 5G Standalone (SA) market, highlighting the key trends and drivers that are shaping the market, along with details of commercial launches by vendor, region, and frequency band. Additionally, the tracker provides details about the 5G SA vendor ecosystem split into two categories – public operator and private network markets.

Table of Contents:

Overview

Market Update

5G SA Market Deployments

Commercial Deployment by Operators

Network Engagements by Region

Network Engagements by Deployments Status

Leading 5G Core Vendors

Mobile Core Vendor Ecosystem

5G Core Vendors Market Landscape

Outlook

5G Standalone Use Cases

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

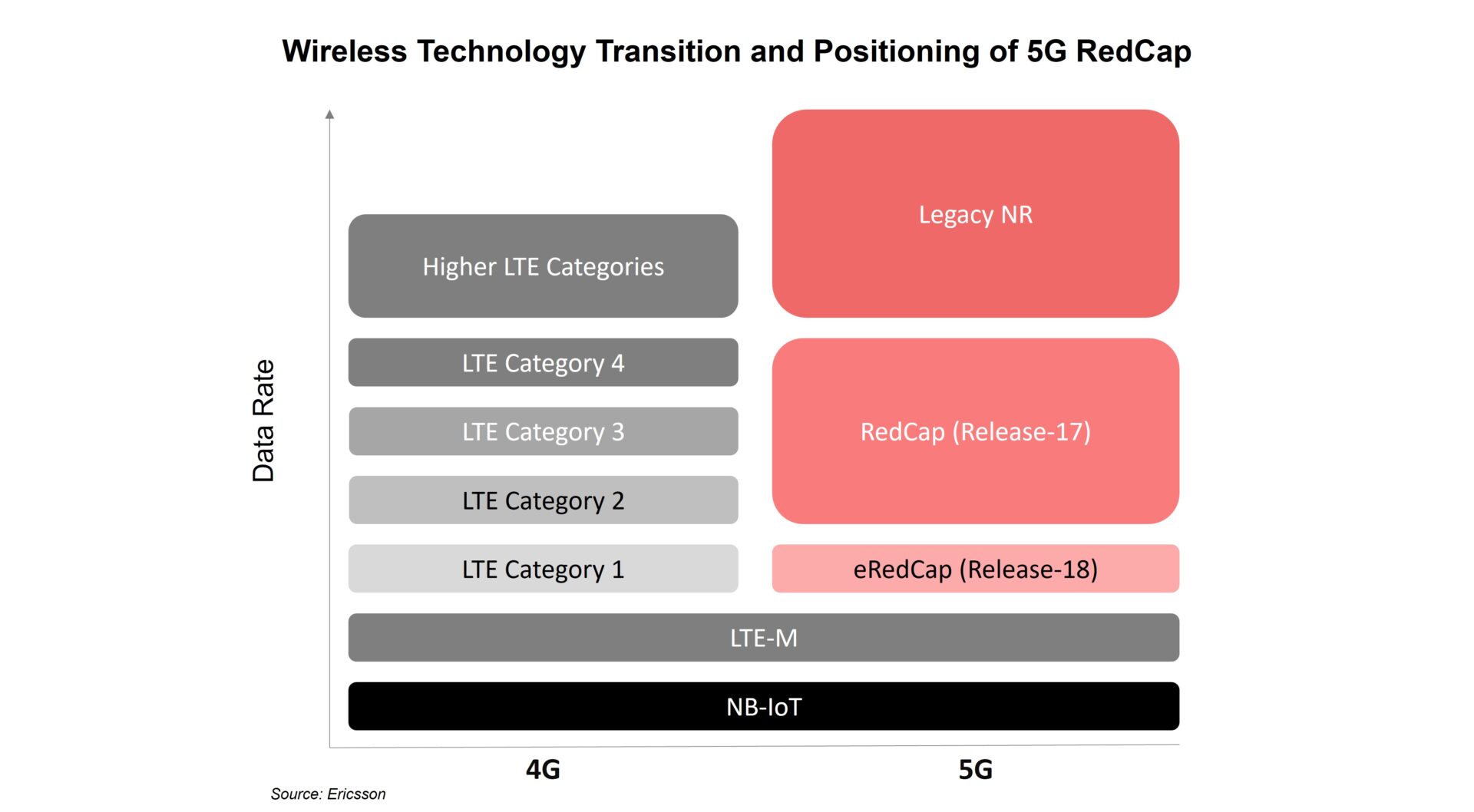

5G RedCap promises a mix of capabilities including improved throughput, extended battery life and less complexity to power diverse use cases cost-effectively.

5G RedCap (including eRedCap) modules are expected to contribute to one-fourth of total cellular IoT module shipments by 2030.

5G RedCap will serve use cases such as wearables, medical devices, video surveillance, industrial sensors and smart grid applications.

We have come a long way from the first generation (1G) to the fifth generation (5G) of cellular connectivity. Despite being in the initial stages of its rollout, 5G is poised for adoption at a speed not seen by previous cellular standards.

However, from the IoT perspective, 5G is being considered only for high-end applications due to the higher cost and existence of many use cases which need low power and low bandwidth, currently served by LPWAN. We can see the potential that 5G brings to IoT applications in terms of faster connectivity, low latency, reliability and large capacity compared to LTE networks. These benefits make 5G valuable for certain IoT use cases, creating a need for low-end 5G for the LPWAN application.

What are 5G RedCap and 5G eRedCap?

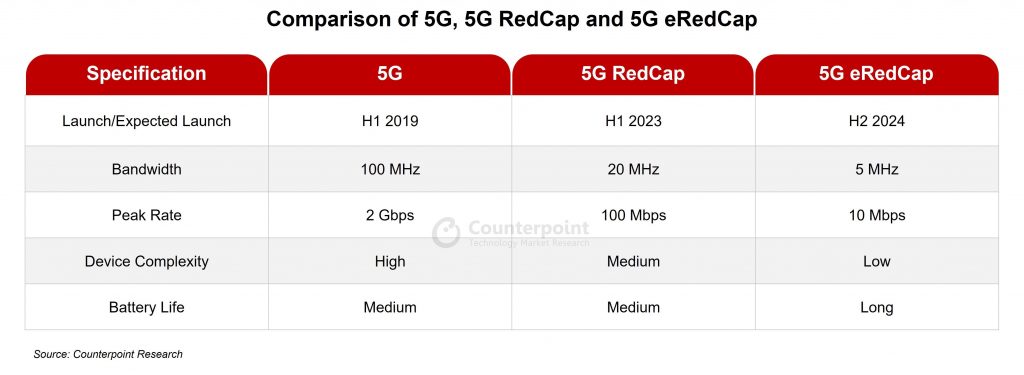

5G RedCap (Reduced Capacity), aka NR-Lite (New Radio-Lite), is a lighter version of the 5G standard that will cater to those use cases where ultra-low latency is not essential, but there is a need for reasonable throughput to support data flows in applications like router/CPE, mass-market automotive, POS and telematics devices, which are currently addressed by LTE Cat 4. In the upcoming 3GPP Release-18, there will be another version of 5G RedCap, called eRedCap (enhanced-RedCap), which will serve the use cases currently being served by LTE Cat 1 and LTE Cat 1 bis.

Market opportunity for 5G RedCap

5G RedCap addresses new use cases that cannot be served by advanced 5G standards like eMBB/URLLC and LPWAN. 5G RedCap chipset is already available in the market but we can expect commercial rollout by the first half of 2024. According to Counterpoint Research’s Global Cellular IoT Module Forecast, 5G RedCap modules will constitute 18% of total cellular IoT module shipments by 2030, indicating a significant market potential, particularly in developing nations where the cost is key to wide technology adoption for digital transformation.

The subsequent 5G eRedCap is planned for a 2024 introduction, with commercial availability likely by 2026. Expected to bring further innovations to the IoT segment, 5G eRedCap modules are projected to contribute 8% to the total cellular IoT module shipments by 2030.

During the transition phase, network operators will maintain IoT device support through the existing 4G network while focusing on 5G high-end applications like routers/CPE, XR/VR devices and automotive.

By the end of the decade, cellular IoT will generally migrate to 5G, driven by new use cases offered by the 5G network, with 4G serving as a fallback. The industry is already preparing for this shift, moving away from legacy technology towards newer standards.

5G RedCap ecosystem and applications

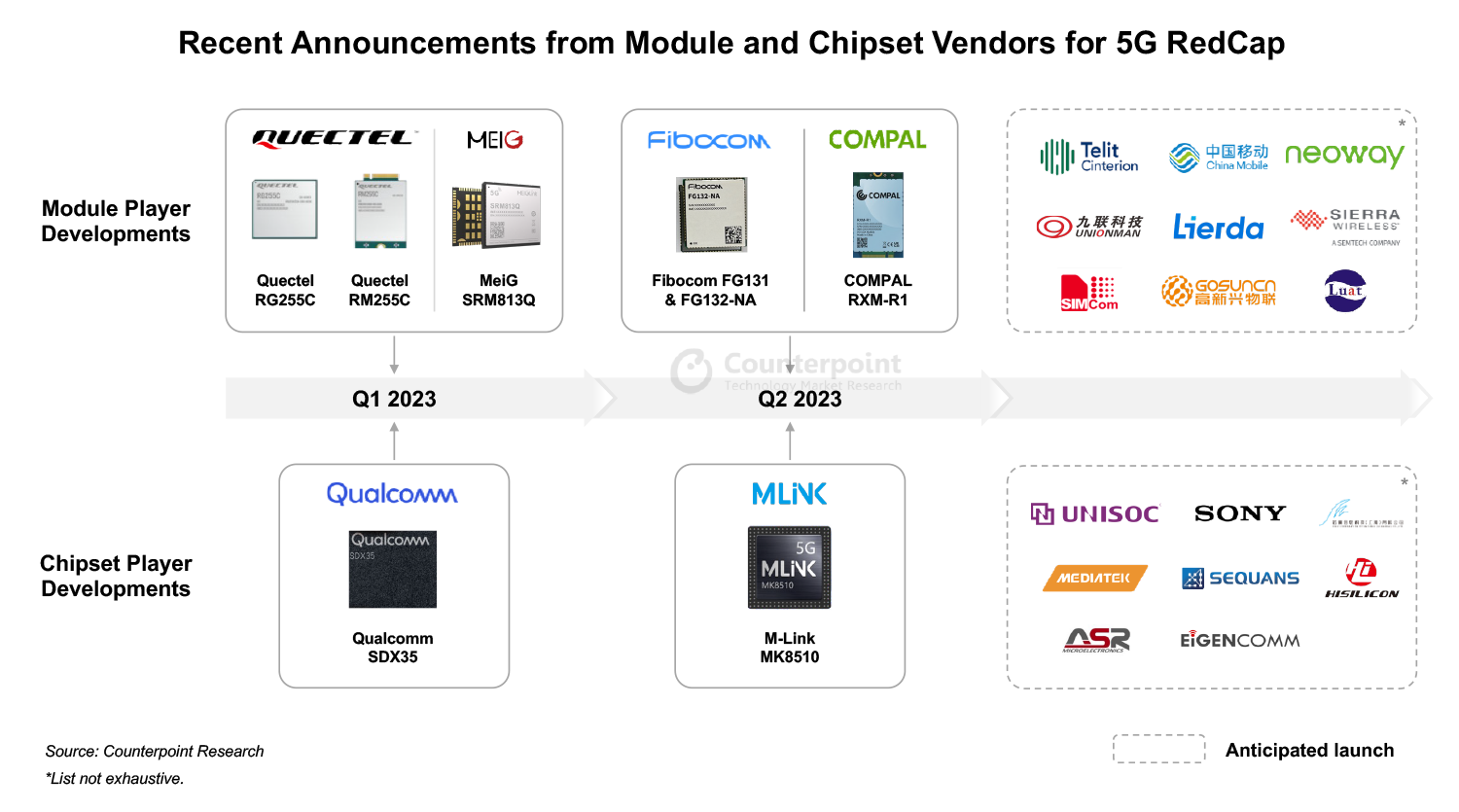

We can see a flurry of new announcements from ecosystem players to adopt the 5G RedCap standard. Module and chipset players are forging partnerships to capture the opportunity which will be created by 5G RedCap. Qualcomm always has been at the forefront when it comes to adopting new technologies with big potential. We can see that with its launch of the industry’s first SDX35 5G RedCap modem. Qualcomm’s early entry and partnerships with major module vendors will help it to grab more market share in 5G when the mass adoption of 5G RedCap will take place.

5G RedCap will serve the use cases in industrial, enterprise and consumer applications, like smart wearables, medical devices, XR glasses, health monitors, video surveillance cameras, wireless industrial sensors, utility/smart grid applications and even Fixed Wireless Access (FWA) and customer premises equipment (CPEs).

5G eRedCap is likely to be preferred for the applications served by 4G Cat 1, such as tracking devices, charging stations, micro-mobility and battery-powered sensors.

Conclusion

5G RedCap promises to broaden the 5G ecosystem, facilitating more connections. It fills the gap between LPWA and URLLC, simplifying 5G integration in IoT applications. 5G RedCap and eRedCap modules will be cost-effective, enabling OEMs to manufacture less complex, low-cost devices with lower power consumption, something that standard 5G cannot offer.

Though 5G at the IoT level is a few years out, vendors can create devices operable over LTE, with an easy switch to RedCap by changing the communication module. This allows immediate product deployment, with an easy future transition to 5G RedCap as the standard evolves.

5G RedCap’s flexibility and network advantages, including lowerlatency and higherspeeds compared to previous LTE generations, position it as a superior choice for future mass IoT deployment. Numerous potential connections across consumer, industrial and enterprise verticals such as FWA, CPE and vehicle connectivity will greatly benefit, accelerating IoT adoption on a massive scale.

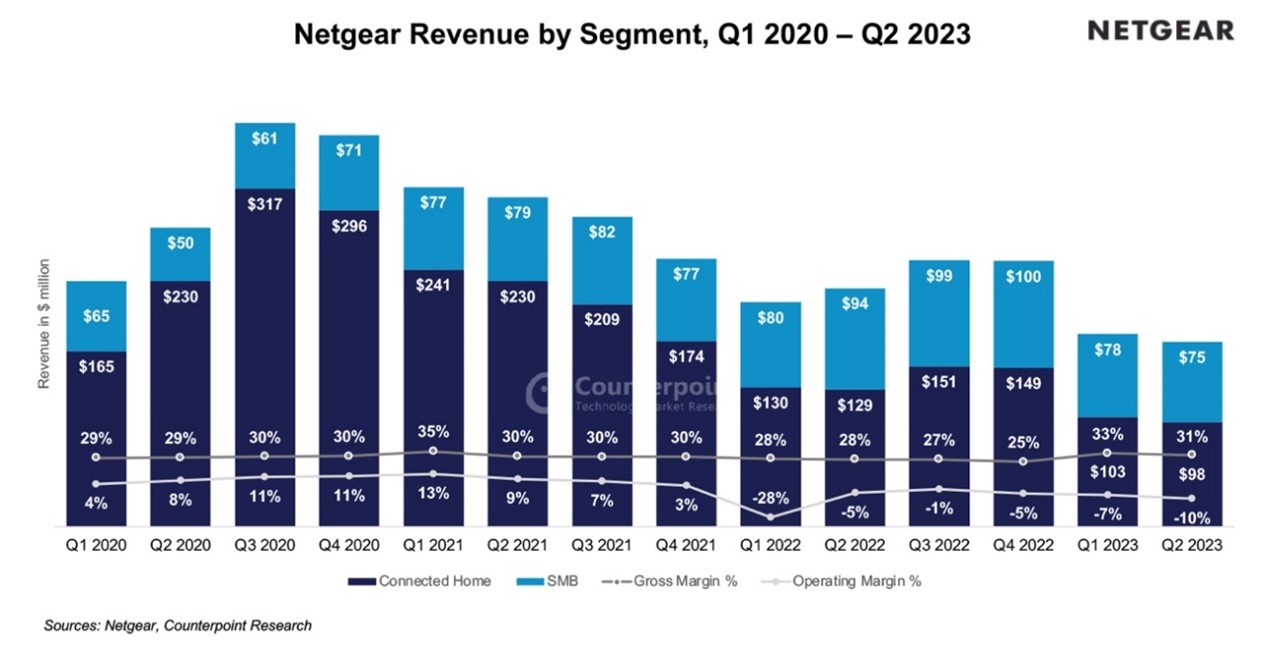

Netgear’s Q2 2023 revenue declined 22.3% YoY to $173.4 million.

Inventory correction in H1 2023 totaled $66 million.

Orbi, Nighthawk, 5G mobile hotspots and Pro AV will drive revenues in Q3 2023.

Netgear expects the Q3 2023 revenues to be in the range of $175-$190 million.

[rev_slider alias=”carousel”][/rev_slider]

Netgear’s revenue declined 22.3% YoY in Q2 2023 to $173.4 million, coming at the higher end of the guidance primarily due to an increase in orders from the service provider channel. The company experienced an inventory correction worth $29 million in Q2 2023, taking the H1 2023 inventory corrections to $66 million. As the inventory levels begin to stabilize, we expect the inventory spills will be 20% lower in H2 2023 compared to H1 2023.

Premium offerings, Pro AV switches shine amid revenue declines in both segments

Connected home and SMB (small and medium business) segments suffered declines of 24% and 21% YoY, respectively, in Q2 2023 primarily due to inventory corrections at channel partners.

Gross margin continued to be above 30% in the second quarter as premium product sales grew and freight costs went down.

However, the operating margin continued to be in the negative region as inventory correction amounted to over $29 million. It is expected to improve in Q3 with an improved mix of higher-ASP products in the connected home and SMB segments.

The retail market is starting to stabilize with consumer demand increasing toward premium networking equipment as the number of Wi-Fi-enabled devices continues to increase. As home networks become more crowded with bandwidth-hungry devices, the demand for Mesh routing devices will increase with time to ease out home networks.

The end consumer devices have become more feature-rich, especially with AI (artificial intelligence) which now requires more bandwidth, low latency and more reliable Wi-Fi connection. This has led to strong consumer demand for premium routers offering such features.

The Orbi and Nighthawk series of routers continued to perform well for Netgear along with 5G mobile hotspots and experienced a YoY increase in shipments in Q2 2023.

Pro AV-managed switches continued to outperform other end devices in the SMB segment to deliver a growth of more than 40% YoY in Q2 2023. Netgear is significantly committed to building leadership in IP-over-AV switches and continues to invest more to grow this segment.

Other SMB products experienced a major drop in sales due to macroeconomic headwinds affecting enterprise spending in the past couple of quarters, delaying the upgrades to newer Wi-Fi technologies.

Revenues from service providers, in APAC and Europe decline significantly

Though service provider revenue increased sequentially in Q2 2023 to $25 million, it suffered a decline of 30% YoY. Revenues were at the higher end of the guidance due to an increase in orders from a major service provider.

Netgear shipped around 6 million units of wired and wireless networking devices, compared to 2.2 million in the same period last year. It shipped around 426,000 units of all types of routers and gateways.

Sales in APAC and Europe declined 20% and 40% YoY, respectively, due to an economic slowdown in these regions, especially Greater China and South Korea.

Paid subscribers to reach 875,000 by year-end, inventory corrections to stabilize

Netgear is on the path to achieve a paid subscriber base of 875,000 by the end of 2023 as it touched 800,000 in Q2 2023. Revenue from subscriptions grew 8% YoY in Q2 2023 to end at $10.3 million.

With concerns about internet security on the rise, especially with a growing number of smart devices, online internet security software is expected to gain momentum in the second half of this year.

Netgear expects the revenue to be in the range of $175 million to $190 million in Q3 2023, as inventory correction is expected to ease out. However, it will still take two more quarters for Netgear to bring down inventory-carrying levels to less than 10 weeks.

Key takeaways

Counterpoint expects an increase in shipments for 5G mobile hotspots in H2 2023 as the consumer demand for such products is on the rise. Netgear is expected to launch a couple of Wi-Fi 7 Orbi Mesh routers and quadband Nighthawk routers in Q3 2023.

However, Wi-Fi 7 upgrade cycle is expected to begin sometime in mid-2024, as IEEE is yet to announce the schedule of the certification program for Wi-Fi 7. Therefore, Wi-Fi 6/6E is expected to form more than 50% of the market in the next two years.

Netgear is expected to open more company-owned premium retail outlets which will help it to provide a better customer experience and a competitive edge in the market.

Consumer awareness around online internet security remains low. Netgear can play a part in increasing consumer awareness through its D2C (direct-to-consumer) communication channels.

Macroeconomic headwinds have slowed down enterprise spending, thus delaying the Wi-Fi upgrade cycle toward Wi-Fi 6/6E.

5G FWA market has been performing well across most of the regions. With more regions opting to reduce the digital divide through FWA, the market promises to offer further growth and become a challenger to fixed broadband technologies.

The recent surge in interest in generative AI highlights the critical role that AI will play in future wireless systems. With the transition to 5G, wireless systems have become increasingly complex and more challenging to manage, forcing the wireless industry to think beyond traditional rules-based design methods.

5G Advanced will expand the role of wireless AI across 5G networks introducing new, innovative AI applications that will enhance the design and operation of networks and devices over the next three to five years. Indeed, wireless AI is set to become a key pillar of 5G Advanced and will play a critical role in the end-to-end (E2E) design and optimization of wireless systems. In the case of 6G, wireless AI will become native and all-pervasive, operating autonomously between devices and networks and across all protocols and network layers.

E2E Systems Optimization

AI has already been used in smartphones and other devices for several years and is now increasingly being used in the network. However, AI is currently implemented independently, i.e. either on the device or in the network. As a result, E2E systems performance optimization across devices and network has not been fully realized yet. One of the reasons for this is that on-device AI training has not been possible until recently.

On-device AI will play a key role in improving the E2E optimization of 5G networks, bringing important benefits for operators and users, as well as overcoming key challenges. Firstly, on-device AI enables processing to be distributed over millions of devices thus harnessing the aggregated computational power of all these devices. Secondly, it enables AI model learning to be customized to a particular user’s personalized data. Finally, this personalized data stays local on the device and is not shared with the cloud. This improves reliability and alleviates data sovereignty concerns. On-device AI will not be limited to just smartphones but will be implemented across all kinds of devices from consumer devices to sensors and a plethora of industrial equipment.

New AI-native processors are being developed to implement on-device AI and other AI-based applications. A good example is Qualcomm’s new Snapdragon X75 5G modem-RF chip, which has a dedicated hardware tensor accelerator. Using Qualcomm’s own AI implementation, this Gen 2 AI processor boosts the X75’s AI performance more than 2.5 times compared to the previous Gen 1 design.

While on-device AI will play a key role in improving the E2E performance of 5G networks, overall systems optimization is limited when AI is implemented independently. To enable true E2E performance optimization, AI training and inference needs to be done on a systems-wide basis, i.e. collaboratively across both the network and the devices. Making this a reality in wireless system design requires not only AI know-how but also deep wireless domain knowledge. This so-called cross-node AI is a key focus of 5G Advanced with a number of use cases being defined in 3GPP’s Release 18 specification and further use cases expected to be added in later releases.

Wireless AI: 5G Advanced Release 18 Use Cases

3GPP’s Release 18 is the starting point for more extensive use of wireless AI expected in 6G. Three use cases have been prioritized for study in this release:

Use of cross-node Machine Learning (ML) to dynamically adapt the Channel State Information (CSI) feedback mechanism between a base station and a device, thus enabling coordinated performance optimization between networks and devices.

Use of ML to enable intelligent beam management at both the base station and device, thus improving usable network capacity and device battery life.

Use of ML to enhance positioning accuracy of devices in both indoor and outdoor environments, including both direct and ML-assisted positioning.

Channel State Feedback:

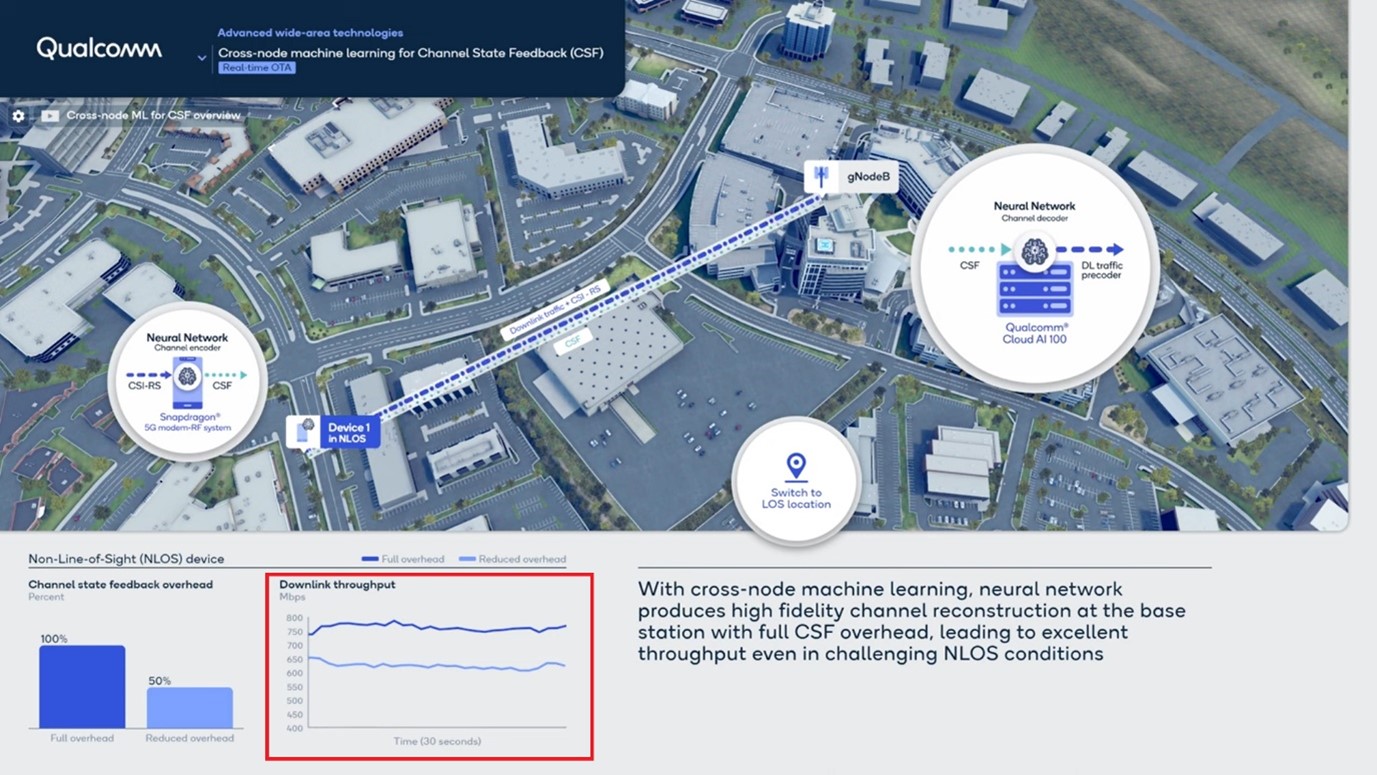

CSI is used to determine the propagation characteristics of the communication link between a base station and a user device and describes how this propagation is affected by the local radio environment. Accurate CSI data is essential to provide reliable communications. With traditional model-based CSI, the user device compresses the downlink CSI data and feeds the compressed data back to the base station. Despite this compression, the signalling overhead can still be significant, particularly in the case of massive MIMO radios, reducing the device’s uplink capacity and adversely affecting its battery life.

An alternative approach is to use AI to track the various parameters of the communications link. In contrast to model-based CSI, a data driven air interface can dynamically learn from its environment to improve performance and efficiency. AI-based channel estimation thus overcomes many of the limitations of model-based CSI feedback techniques resulting in higher accuracy and hence an improved link performance. The is particularly effective at the edges of a cell.

Implementing ML-based CSI feedback, however, can be challenging in a system with multiple vendors. To overcome this, Qualcomm has developed a sequential training technique which avoids the need to share data across vendors. With this approach, the user device is firstly trained using its own data. Then, the same data is used to train the network. This eliminates the need to share proprietary, neural network models across vendors. Qualcomm has successfully demonstrated sequential training on massive MIMO radios at its 3.5GHz test network in San Diego (Exhibit 1).

Exhibit 1: Realizing system capacity gain even in challenging non-LOS communication

AI-based Millimetre Wave Beam Management:

The second use case involves the use of ML to improve beam prediction on millimetre wave radios. Rather than continuously measuring all beams, ML is used to intelligently select the most appropriate beams to be measured – as and when needed. A ML algorithm is then used to predict future beams by interpolating between the beams selected – i.e. without the need to measure the beams all the time. This is done at both the device and the base station. As with CSI feedback, this improves network throughput and reduces power consumption.

6G will need to deliver a significant leap in performance and spectrum efficiency compared to 5G if it is to deliver even faster data rates and more capacity while enabling new 6G use cases. To do this, the 6G air interface will need to accommodate higher-order Giga MIMO radios capable of operating in the upper mid-band spectrum (7-16GHz), support wider bandwidths in new sub-THz 6G bands (100GHz+) as well as on existing 5G bands. In addition, 6G will need to accommodate a far broader range of devices and services plus support continuous innovation in air interface design.

To meet these requirements, the 6G air interface must be designed to be AI native from the outset, i.e. 6G will largely move away from the traditional, model-driven approach of designing communications networks and transition toward a data-driven design, in which ML is integrated across all protocols and layers with distributed learning and inference implemented across devices and networks.

This will be a truly disruptive change to the way communication systems have been designed in the past but will offer many benefits. For example, through self-learning, an AI-native air interface design will be able to support continuous performance improvements, where both sides of the air interface — the network and device — can dynamically adapt to their surroundings and optimize operations based on local conditions.

5G Advanced wireless AI/ML will be the foundation for much more AI innovation in 6G and will result in many new network capabilities. For instance, the ability of the 6G AI native air interface to refine existing communication protocols and learn new protocols coupled with the ability to offer E2E network optimization will result in wireless networks that can be dynamically customized to suit specific deployment scenarios, radio environments and use cases. This will a boon for operators, enabling them to automatically adapt their networks to target a range of applications, including various niche and vertical-specific markets.

The US remains the top market for Tesla followed by China and Europe.

Aiming to develop an in-house AI ecosystem, Tesla has started building its own Dojo training supercomputer.

With this growth trajectory, Tesla is expected to achieve sales of around 1.9 million units by the end of 2023.

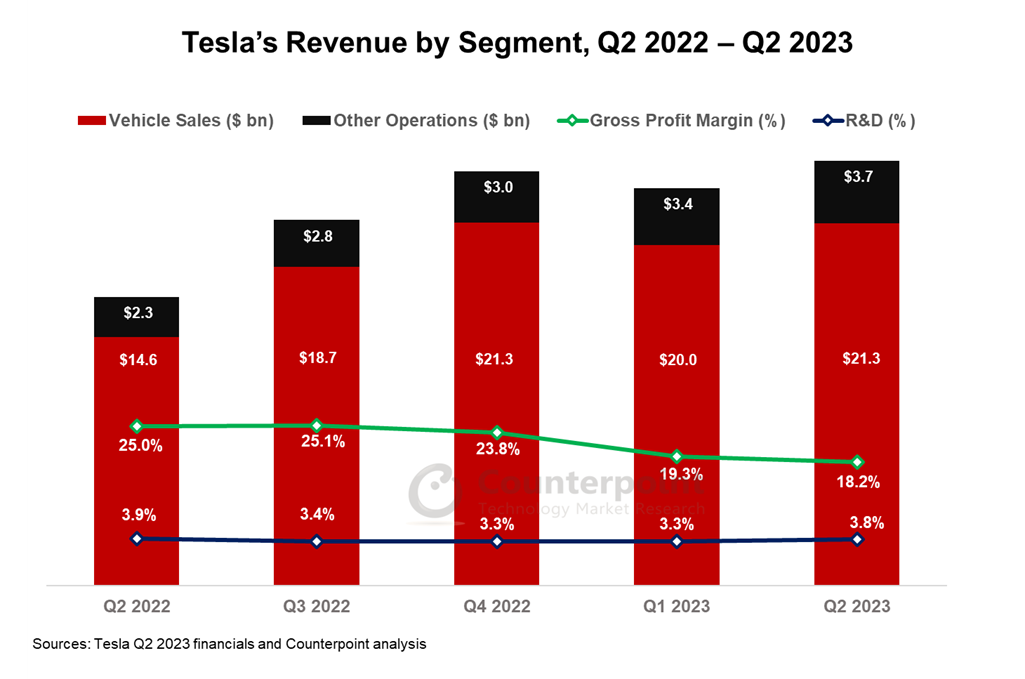

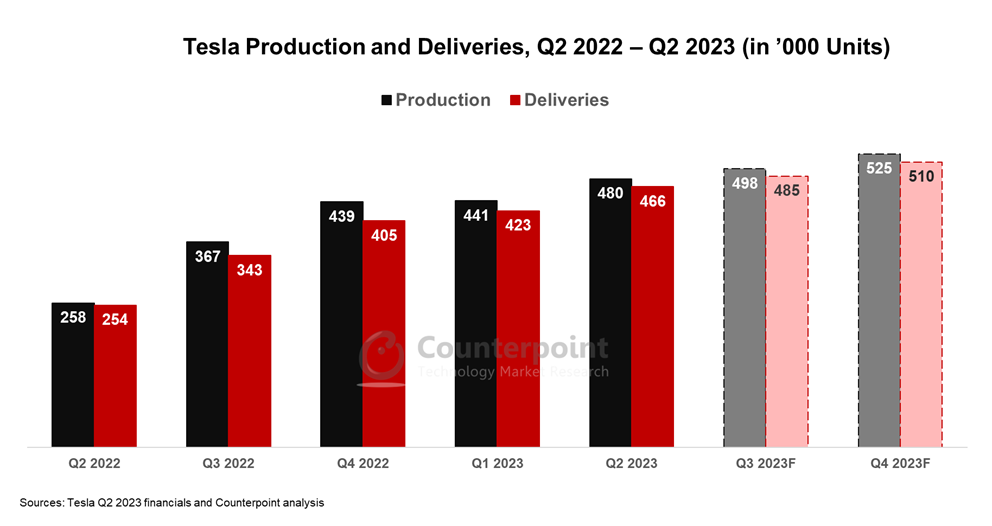

Tesla achieved remarkable results in Q2 2023, with its revenue growing 47% YoY to reach the record-breaking figure of nearly $25 billion. The company’s vehicle deliveries too hit a record at 466,915, growing 83% YoY. The US retained its position as Tesla’s largest market, contributing to 37.6% of the total sales, while China and Europe followed closely behind. Global price cuts for the Model Y and Model 3, along with tax subsidies in the US and China, were two of the biggest drivers for Tesla’s Q2 sales.

Tesla CEO Elon Musk, during the earnings call, discussed a few key things like the long-awaited Cybertruck deliveries, Tesla’s advantage in competitive pricing of vehicles and the possibilities of attaining complete FSD:

Cybertruck delivery outlook

CEO:“Demand is so – so far, off the hook, you can’t even see the hook. So, that’s really not an issue. I do want to emphasize that the Cybertruck has a lot of new technology in it. Like a lot… So, always very difficult to predict the – the ramp initially, but I think we’ll be making them in high volume next year, and we will be delivering the car this year.”

Soumen Mandal’s analyst take: “Musk is certainly hyping the Cybertruck, not that it needs to anymore, but there is also significant expectation setting with discussions on internal production and supply chain hurdles. Is this another Model Y? That’s a tough act to follow, but the Cybertruck does bring a slew of unique parts and processes. So, longer term, we expect to see another products flywheel off from it.”

Tesla’s price cuts for its vehicles

CEO: “And we, you know — we just — we just course according to what the mood of the of the public is, you know. Buying a new car is a — it’s a big decision for vast majority of people. So, you know, anytime there’s economic uncertainty, people generally pause on new car buying, at least to see to see what happens.

And, you know — and then, obviously, another challenge is the — the interest rate environment. As interest rates rise, the affordability of anything bought with that decreases, so effectively increasing the price of the car. So, when interest rates rise dramatically, we actually have to reduce the price of the car because the — the interest payments increase the price of the car. So — and this is at least — at least up until recently was to believe the sharpest interest rate rise in history. So, we had to do something about that. And if someone’s got a crystal ball for the global economy, I really appreciate it. If I could borrow that crystal ball.”

Soumen Mandal’s analyst take: “Tesla’s strong supply chain and reduced cost of production due to low raw material cost, especially for lithium, has encouraged the company to reduce prices of its vehicles. Alongside what Musk described as ‘interest rate rises’, Tesla’s price reduction has made all variants of the Model 3 and Model Y eligible for IRA tax credit in the US, where it will benefit in the long term. So, macroeconomic policies and geopolitical relations play a crucial role in deciding such price reductions, incentives or discounts.”

Autonomy (FSD): Timing

CEO: “…the reason I’ve been optimistic [on achieving full self-driving] is what it tends to look like is the — we’ll make rapid progress with the new version of — of FSD. But — but then, it will curve over logarithmically. So — so, at first, like, a logarithmic curve looks like, you know, just sort of fairly straight upward line, diagonally up. And so, if you extrapolate that, then you — you have a great thing. But then because it’s actually logarithmic, it curves over. And then, there have been a series of logarithmic curves. Now, I know I’m the boy who cried FSD, but man, I think — I think we’ll be better than human by the end of this year.”

Abhik Mukherjee’s analyst take: “Almost every auto OEMs are spending on autonomy. Tesla is also walking in the same direction and is building an in-house AI service that includes in-house real-time data sets, neural Net training, vehicle hardware and software. Tesla is expecting to reach perfect FSD soon and for this, it is also building a Dojo supercomputer. Early development of FSD will give Tesla a massive first-mover advantage over its competitors. We assume Tesla FSD might also get adopted by other automakers, like Tesla NACS is being adopted.”

Autonomy (FSD): Disruption

CEO:“It’s not about getting more share. It’s just that you can think of every car that we — that we sell or produce that — that — that has a full Autonomy capability as actually something that, in the future, may be worth as much as five times what it is today…If you’ve got an autonomous — if that vehicle is able to operate autonomously and — and use — be used in either dedicated or autonomous or partially autonomous like — like, Airbnb, like maybe sometimes you allow your car to be used by others, sometimes you want to use it exclusively, just like, you know, Airbnb, you know, doing Airbnb with a room in your house… So, I think it’s sort of it would be — I think it — it does make sense to sacrifice margins in favor of making more vehicles because we think, in the not-too-distant future, they will have a dramatic valuation increase. I think the Tesla fleet value increase to the point at which we can upload full self — you know, full self-driving and it’s approved by regulators, will be the single biggest step change in asset value maybe in history.”

Abhik Mukherjee’s analyst take:“Although we are excited about autonomous vehicles, Tesla currently is a bit far from achieving perfect FSD. Incidents involving Tesla vehicles are frequently reported. Currently, Tesla FSD is only available in the US and it will need a lot of approvals from regulators to ensure 100% safety before it can be rolled out to other regions, especially in Europe where regulations are much stricter. Though achieving complete FSD could disrupt the market in future, currently Tesla must work to make its FSD software incident-free.”

Financial highlights

In the automotive segment, Tesla achieved revenue of $21.26 billion, an annual growth of 7%. Around 4% of this revenue was derived from sales of regulatory credits and automotive leasing.

In addition to the automotive segment, Tesla experienced significant growth in its other businesses, such as energy generation and services, with revenues surging by 57% YoY to reach $3.65 billion in Q2 2023. Tesla deployed 7 GWh of energy storage and 66 MWh of solar panels during the quarter.

Tesla achieved a gross profit of $4.53 billion, a 7.1% YoY increase. High vehicle deliveries, low cost of production due to lower raw material costs and IRA tax credits for EVs in the US contributed to this result. But the low ASP of vehicles due to the voluntary global price cuts also hurt Q2 profitability.

Tesla’s Q2 operating profit was 62%, a decline of 1.8 percentage points sequentially. The reduction can be attributed primarily to the significant expenses incurred in ramping up the production for Cybertruck, Tesla’s in-house 4680 cells and the development of AI through its Dojo training computer. Other additional costs were associated with a new ‘Get to Know Your Tesla’ UI and facelifts for the Model 3 and Model Y.

Outlook

With the current growth trajectory, we expect Tesla deliveries will reach around 1.9 million by the end of 2023. Its robust supply chain and vertically integrated production have given Tesla a competitive advantage.

Other growth opportunities are arising from the adoption of Tesla’s NACS charging standard by several OEMs including Ford, GM, Rivian, Volvo, Polestar and Nissan for the North American market. This allows these auto companies to leverage Tesla’s extensive network of charging stations across North America, enhancing the convenience and accessibility of electric vehicle charging for their customers. But it also gives Tesla the option to increase its revenue by charging licensing fees from OEMs adopting its proprietary NACS ports.

Ericsson and Nokia’s Q2 2023 results are in line with their revised expectations.

The telecom gear manufacturers are convinced that a few short-term hurdles can be managed to drive growth.

The mobile network segment, the largest contributor to both firms’ revenues, witnessed some slowdown in Q2 2023 due to decreased demand from capex-saturated regions.

Nordic telecom giants Ericsson and Nokia announced their Q2 2023 results last week, which were in line with their revised expectations despite lower revenues. The overall market condition remains challenging due to macro uncertainty, but the telecom gear manufacturers are convinced that a few short-term hurdles can be managed to drive growth both in the short term and long term.

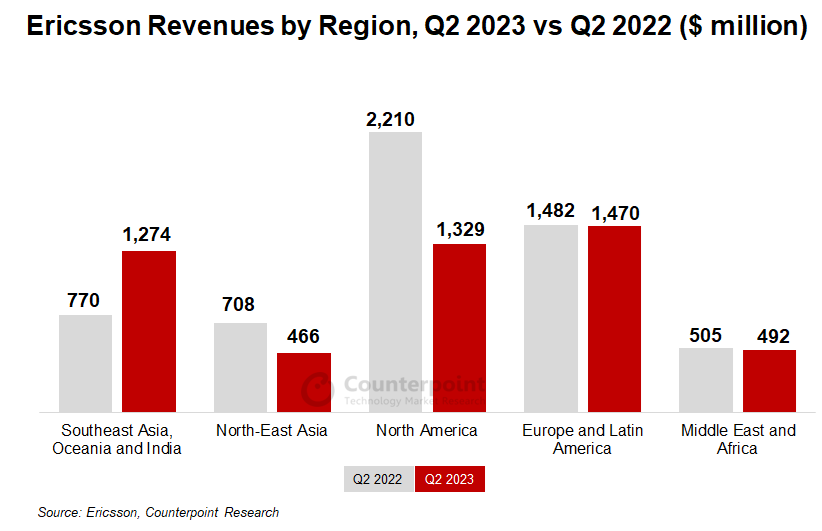

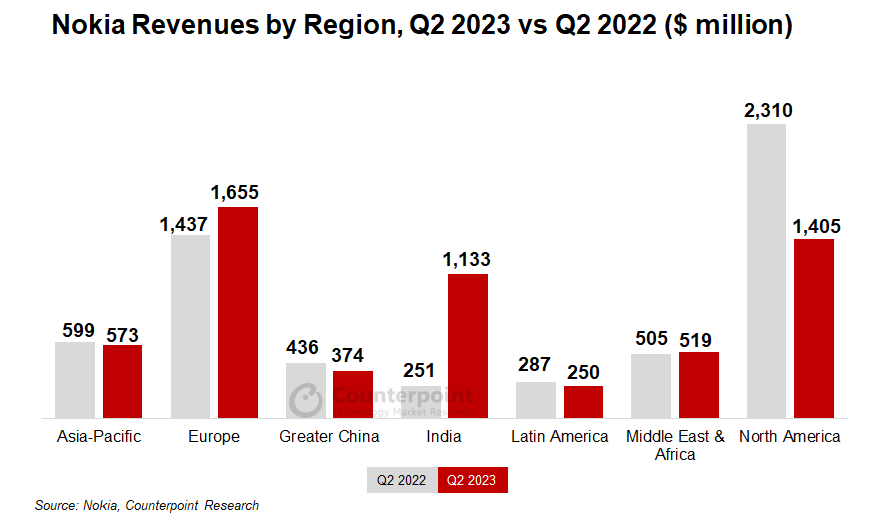

Fast 5G rollouts in emerging nations such as India were highlights for both the vendors as revenue growth in these regions was able to offset the sales decline in North America and North-East Asia where operators slowed down their network expenditures after several quarters of high investment.

Swedish giant Ericsson generated net sales of $5.9 billion for the quarter, reporting a 9% YoY decline in organic sales. Ericsson’s Finnish counterpart Nokia generated $6.2 billion in revenue for the quarter, which was flat YoY on a constant currency basis.

Mobile network segment

This segment is based on the core competence of these organizations and is also the largest contributor to both firms’ revenues. It witnessed some slowdown for the two companies in Q2 2023 on the back of decreased demand from capex-saturated regions. Operators in these regions continue to be selective in spending and are depleting their inventories that have been running high after the 2021-2022 boom.

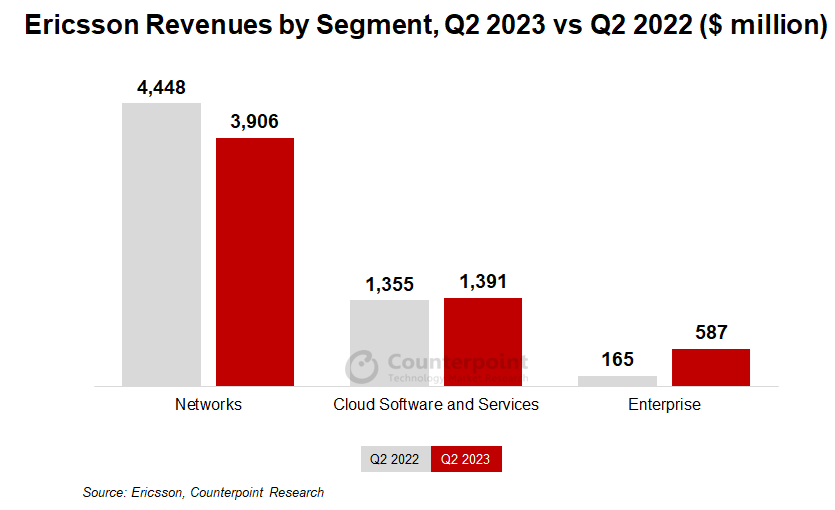

Revenue from Ericsson’s Networks division stood at $3.9 billion. It doubled for emerging markets like India and Southeast Asia but plummeted for regions like North America. India is now Ericsson’s second-biggest market. During the quarter, the company also marked the shipping of 10 million 5G-ready radios.

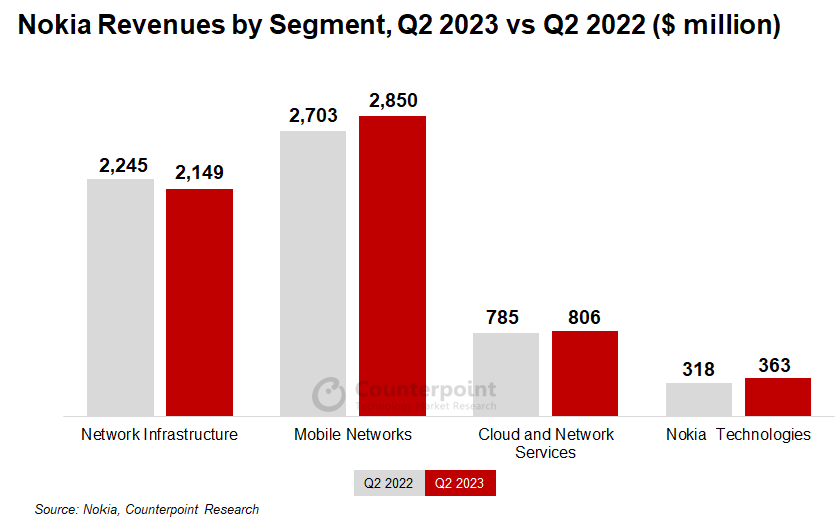

Revenue from Nokia’s Mobile Networks division stood at $2.85 billion, a slight growth YoY. The increase in revenue due to faster 5G rollouts in India and Europe was able to offset the decline in North America.

Gross margin was impacted for both operators as the sales mix changed drastically. Adapting to changing demand and expecting a recovery in the North American region, both manufacturing firms are looking forward to an improved gross margin by the end of this year.

Cloud software services

Telecom service providers too have been hit by cloud disruption as network evolution has witnessed operators migrating to the cloud. The two Nordic vendors have been at the forefront in assisting operators in transitioning to cloud-native operations, which helps in future-proofing and improving network performance and efficiency.

Ericsson’s revenues from its Cloud and Software Services division stood at $1.39 billion, a marginal increase over the previous year. The sales, for a change, were driven by 5G in the North American region. Ericsson currently leads the global market for 5G Standalone Core deployments with a majority of operators choosing the Swedish company for their cloud-native 5G SA Core. Ericsson’s managed services, however, took a hit.

Nokia registered $806 million in net sales for its Cloud and Network Services division. Unlike its Swedish counterpart, Nokia’s growth came from the Europe and Middle-East and Africa (MEA) regions, while it faced a decline in the North American region. Nokia too has been actively helping operators worldwide to deploy 5G Standalone Core (just behind Ericsson in the number of deployments), which alongside Enterprise Solutions helped boost its revenues in this segment, marginally offset by declines in the Cloud Services and Business Applications.

Ericsson’s enterprise segment, network APIs and IPR licensing

Last year, Ericsson acquired Vonage, which contributed revenues of nearly $390 million during the quarter, a 12% increase YoY. The company strongly believes that the enterprise segment will continue to grow as it redefines how the capabilities of 5G networks are utilized and paid for by the customers.

Ericsson will also continue to digitize the ecosystem for CSPs by maintaining its investments to build the Global Network Platform (network Application Program Interfaces or APIs). With time, a variety of global network APIs will complement the existing communication APIs like video, voice and SMS to help CSPs better monetize their 5G networks, accelerate 5G network rollout and improve network capex.

The company also signed a 5G IPR licensing agreement during this quarter to help validate its IPR portfolio strength.

Nokia’s diverse portfolio – Networks infrastructure and enterprise

Despite facing some short-term challenges and macroeconomic uncertainty, which resulted in a YoY revenue decline, Nokia’s Network Infrastructure segment generated $2.15 billion in revenues and continued to gain market share across the globe.

The IP networks grew in Europe with increasing sales to enterprise customers.

The optical networks unit registered a double-digit growth driven by increasing broadband penetration in India.

The fixed networks unit witnessed a decline on the back of slowing FWA deployments in North America.

Nokia’s revenue from its enterprise customers grew by almost 30% YoY. The company added 90 new enterprise customers this quarter. Its private wireless business reached more than 635 customers.

Nokia also signed a long-term patent license agreement with Apple. Multi-year revenue recognition might start in January 2024.

Nokia also struck an important deal with Red Hat this quarter, where the latter will serve as the primary reference platform to develop, test and deliver core network applications in an attempt to rebalance Nokia’s portfolio.

Analyst outlook

Network equipment vendors and software providers are looking to transform obstacles into opportunities. Both Ericsson and Nokia are expecting their business performance to improve towards Q4 2023 and to continue improving in the coming years. Inventory correction by operators has been the prime reason for the revenue decline this quarter. But network sales have been able to weather the slowdown as operators need to increase the capacity of their networks.

Counterpoint Research believes that 5G investment has not yet peaked. Over the next few years, the industry will witness the advent of 5G Advanced starting with 3GPP Release 18, operators transitioning to 5G SA, an increase in the number of monetizable 5G use cases, FWA going global, and increased 5G investments in mid-band and mmWave bands. The entire mobile industry is bullish about private networks, which present a significant opportunity for operators and vendors alike. Amid the growing geopolitical turbulence, with the West hardening its stand on the “rip and replace” of Chinese networking equipment, Nokia and Ericsson might even see other markets opening up for them. Reducing internal costs and streamlining internal operations remains a challenge for both suppliers. The two should benefit from growing confidence in the enterprise segment. Nokia expects to leverage its leadership in the network infrastructure business and attain market leadership in the fixed-broadband space with its wide variety of ONTs, OLTs and FWA CPEs.

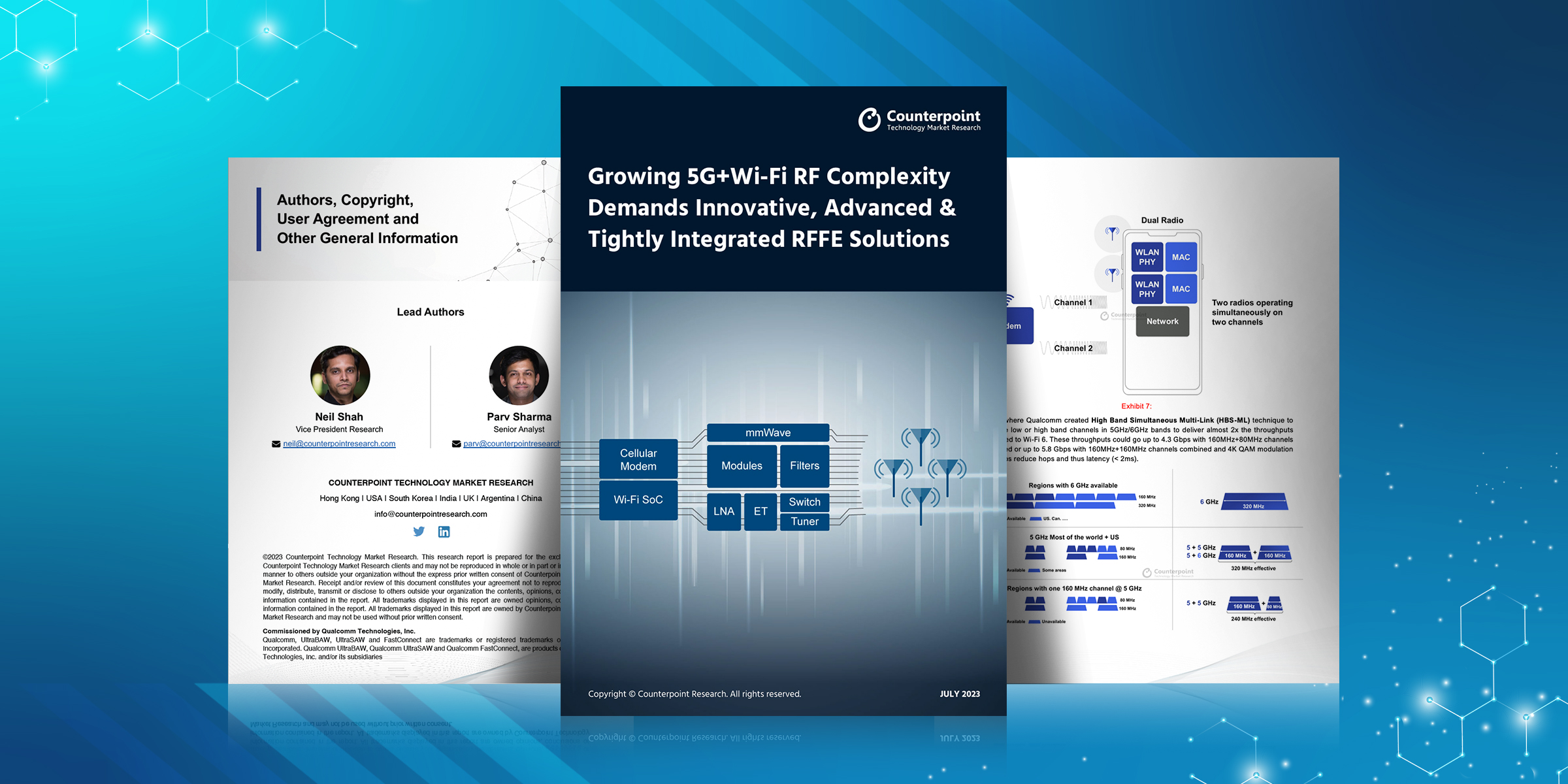

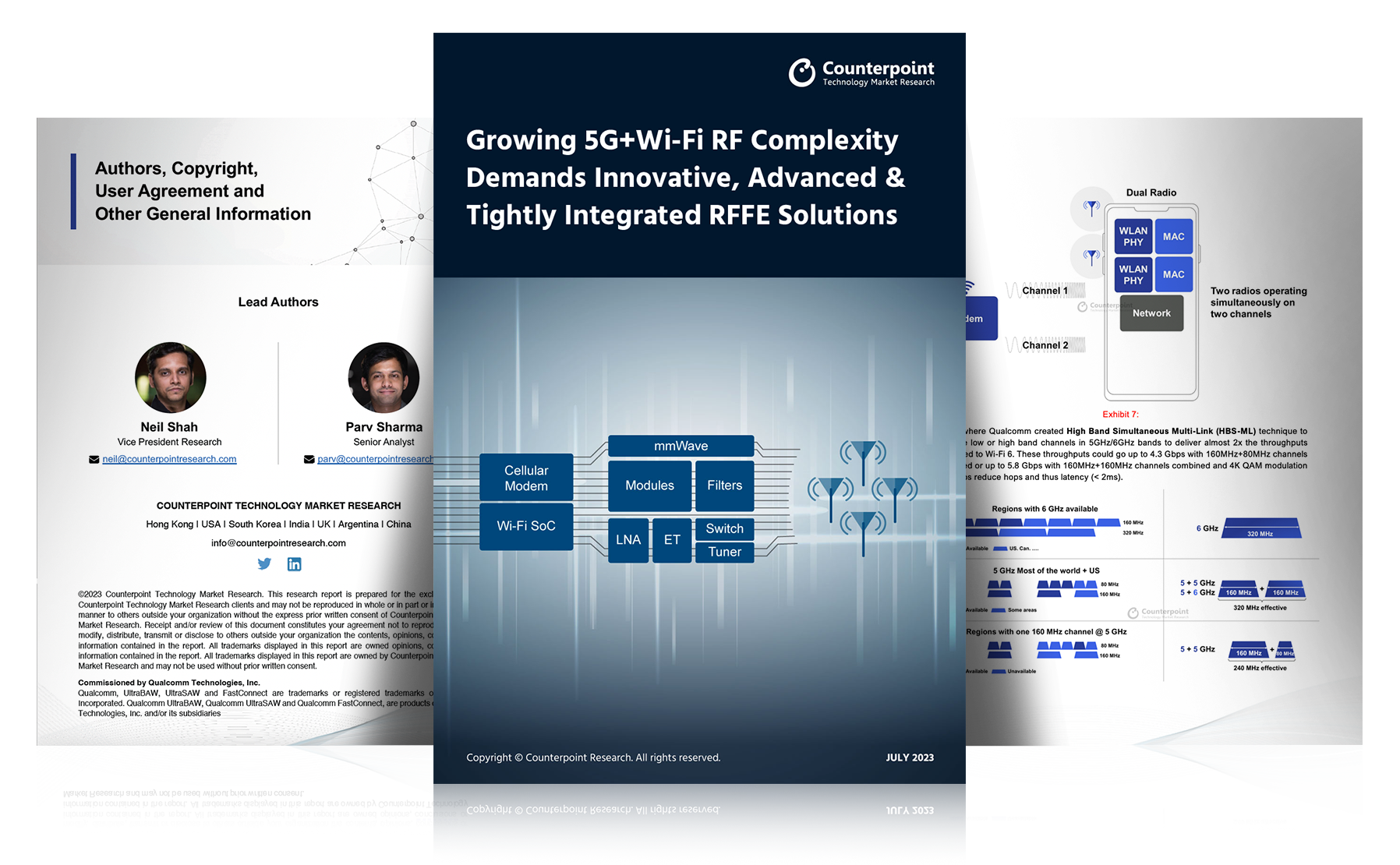

The rising adoption of advanced multimode cellular (5G, 4G) and wireless (Wi-Fi 6/6E/7) delivers powerful benefits while also driving significant RF complexity in smart connected devices. 5G and Wi-Fi 7 integration has multiple challenges that need cutting-edge RF design, components and end-to-end optimization. There are multiple players in the RF Front-End (RFFE) ecosystem, but most are specialists in only one or a few areas.

This paper highlights the technology potential of these powerful wireless technologies, complexity it brings and how product designers and manufacturers can solve these complexities with an advanced, end-to-end optimized and integrated RFFE solution.

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.