Our Senior Analyst, Tina Lu, will be speaking at the 5G Americas Virtual Forum on 24th July, 2024.

Session: 5G FWA Growth in Latin America Date: 24th July, 2024 Time: 1.20 PM ET

About the Event: 5G Americas is an industry trade organization comprised of leading telecommunications service providers and manufacturers. The organization’s mission is to promote and foster the advancement and full capabilities of LTE wireless technologies and their evolution to 5G, across all networks, services, applications and connected devices in the ecosystem in the Americas.

They are committed to developing a connected wireless community while leading the development of 5G for the entire Americas. 5G Americas is headquartered in Bellevue, Washington, USA.

Generative AI (GenAI) is developing into more than a buzzword as various industries now realize its benefits and wide range of applications. The telecom industry can also gain from GenAI with use cases such as network optimization, enhanced customer experience, content personalization and AI chatbots. At the recently concluded Amdocs APAC Analyst Summit in Singapore, Neil Shah, VP of Research at Counterpoint Research sat down with Ofir Daniel, Head of Platforms Marketing at Amdocs, to talk about the strategy and use cases of GenAI for telcos.

The interview

Key takeaways from the discussion

• Beyond traditional AI, Amdocs sees GenAI as a powerful tool to accelerate day-to-day business processes. Amdocs has analyzed 600 ideas and mapped over 120 use cases across seven domains.

• Amdocs’ new ‘amAIz’ platform is designed to integrate telco workflows with GenAI capabilities. This includes customer care, sales, end-to-end service orchestration, inventory management and even troubleshooting.

• amAIz is a scalable platform that will allow telcos to bring GPTs to the telco domain.

• Initial GenAI use cases focus on sales and customer care where AI chatbots can manage routine customer enquiries and offer targeted recommendations.

• GenAI can also streamline B2B sales by generating proposals and optimizing the pricing based on customer profiles that suit their needs and usage patterns, including data usage and travel habits. This will help sales representatives to close more deals and increase revenue.

• Besides building the proprietary Copilot using its IP and software, Amdocs has also partnered with Microsoft to integrate Copilot assistant with its Customer Experience Platform (CEP), and to work with its OSS and BSS systems.

• Operators are in the initial stages of testing Copilot applications, and it will take a while before Copilot moves to autopilot.

Analyst takeaways:

• The biggest challenge faced by today’s telcos remains the same – monetization and cost savings in leveraging newer technologies whether its 5G, AI or Cloud.

• With 5G, the entire telco architecture has been transformed allowing telcos to cloudify everything beyond the RAN and drive various levels of automation to increase efficiency, scalability and drive costs down.

• However, the different levels of automation, right from RAN and Transport to Core networks, can be further enabled by AI advancement as the industry shifts to GenAI.

• Players such as Amdocs are innovating on GenAI capabilities to enable intelligent digital transformation with a platform approach by striking the right partnerships with hyperscalers as well as AI-enablers such as OpenAI, Mistral and NVIDIA.

• Amdocs is bringing its GenAI demos and use cases to telcos and potentially similar verticals. Its amAIz platform targets multiple domains such as customer care, CRM, billing, services orchestration and network troubleshooting.

• Amdocs is a one-stop shop and a leader for anything related to software, IT, services, automation if you are a telco (or any big enterprise) with unparalleled knowledge, capabilities and experience in their digitally transformational journey. This capability and experience expand across operations from billing and marketing to customer experience and analytics.

• The GenAI-led digital transformation is real and is bringing about some significant use cases.

Small cell solutions provider Picocom is making innovative use of RISC-V processors in the Open RAN market. Committed to open standards, Picocom’s innovative solution offers a unique value proposition. Gareth Owen, Associate Director at Counterpoint Research, sat down with Picocom CEO Peter Clayton at MWC 2024 in Barcelona to discuss the company’s product portfolio that includes PC802 and PC805, its differentiation strategy and target markets.

The interview

Key takeaways from the discussion

Picocom’s USP and product differentiation:

• Unlike incumbents like Huawei and Ericsson, who design their own SoCs for their RAN products, Picocom focuses on Open RAN, offering small cell SoCs to cater to the needs of smaller OEMs in the market.

• By leveraging RISC-V cores, Picocom offers open standard processors, which helps its customers avoid vendor lock-ins.

Product portfolio and software solutions:

• PC802 is Picocom’s first chip and has been in the market for around two years now, catering to the physical layer of baseband processing for several applications and use cases.

• PC805 is the newly launched SoC featuring an integrated radio transceiver, and initial samples have been shipped to the customers already.

• The PC805 development board comes with a complete Open RAN Radio Unit (O-RU) enabling high-power output.

• When it comes to software, Picocom offers both source code and binary code licensing, thus enabling customers to choose the level of customization to suit their specific needs.

Target markets:

• Picocom has global presence through partnerships and system integrators, but most of its OEM customers are in Asia, including China, Japan, Taiwan and South Korea. However, these OEMs sell their products globally.

• It is also seeing demand from European and North American markets.

• After launching the PC805, Picocom is also seeing significant interest in O-RUs for both indoor and outdoor applications.

Analyst takeaways:

• Picocom is pioneering a range of Open RAN-based small cell SoC solutions and to date have launched two RISC-V based chipsets.

• The PC802 is a flexible silicon solution that is equally suitable for traditional LTE/5G NR distributed architecture. It can be used for a wide range of applications, including indoor residential, enterprise and industrial networks, as well as neutral host network applications.

• The PC805 chip is the first SoC optimized for 5G O-RUs. It interfaces with a DU as part of O-RAN Split 7.2x via an open fronthaul eCPRI interface and supports seamless connections to RFICs, with the option of also using standard JESD204B high-speed serial interfaces.

5G technology offers a significant leap over 4G, unlocking low-latency, high-upload and high-download speeds in today’s connected era. But as we rely more on connectivity for new and immersive experiences for applications like Extended Reality (XR), connected cars and even generative AI applications, 5G Advanced will push the boundaries of what is possible.

5G Advanced Release 18 is nearing completion with finalization expected in June 2024, whereas Release 19 is estimated to be completed in the second half of 2025. From massive network capacity to ultra-low latency and speeds, 5G Advanced enhances network performance, reduces energy consumption, which is good for sustainability, and brings new use cases like non-terrestrial network (NTN) integration.

In the latest episode of The Counterpoint Podcast, host Gareth Owen is joined by Danny Tseng, Technical Director of Marketing at Qualcomm, to discuss 5G Advanced and current and future advancements in the 5G technology. The discussion focuses on how 5G Advanced will play a crucial role in network performance and energy efficiency, while also integrating new applications like IoT and AI. The conversation also briefly touches upon 6G and beyond.

00:58 – Gareth kickstarts the discussion by asking Danny about the status of Release 18 and Release 19.

03:03 – Danny talks about new capabilities and performance improvements of 5G Advanced that will benefit the operators.

04:53 – Danny on new energy-saving features that will be introduced in Release 18 and Release 19.

07:06 – Danny highlights the opportunities for both operators and the satellite industry.

11:22 – AI in air interface is a hot topic. Gareth asks Danny to give the latest information on Qualcomm’s tests on various AI-based air interface use cases.

17:47 – Danny wraps up thoughts on Release 20, followed by Release 21, which is when work on 6G is expected to start.

Artificial intelligence (AI) is rapidly becoming a ubiquitous technology. However, a major downside is that AI processing in the cloud requires a massive amount of power. In this regard, on-device AI can be a boon for sustainability as it processes data directly on a device, which translates into less energy consumption and a smaller carbon footprint. Qualcomm is already focusing on on-device AI, energy-efficient chipsets, and collaborating across industries to promote sustainable practices. At MWC 2024, Jan Stryjak, Research Director at Counterpoint Research had a quick chat with Angela Baker, Qualcomm’s Chief Sustainability Officer on the company’s sustainability efforts and initiatives in this area.

The Interview

Key takeaways from the discussion:

On-device AI for efficiency:

• On-device AI processing is a key driver for sustainability.

• Energy consumption can be reduced by processing data on the device, rather than sending it to the cloud.

• Qualcomm is already researching to quantify these efficiency gains.

5G for efficiency across industries:

• Beyond smartphones, various industries can benefit from Qualcomm’s tech.

• 5G is a good example as it is 90% more efficient than 4G networks.

• It can improve efficiency in agriculture, manufacturing, and connected vehicles.

• With future generations like 6G, Qualcomm will focus on building even more energy-efficient networks.

Balancing sustainability with growth:

• It is always a challenge to align business practices of selling new devices versus promoting sustainability.

• Qualcomm is addressing this by extending software updates for IoT devices (8-10 years).

• Qualcomm is also diversifying into new markets like automotive and IoT.

Adapting to regulations:

• New regulations around sustainability reporting (e.g. CSRD in Europe) are driving Qualcomm’s efforts.

• Qualcomm is conducting a double materiality assessment to align its ESG reporting with the financial strategy.

Analyst Takeaways:

• Qualcomm is at the forefront of AI innovation, and its key messages at MWC were around on-device AI, energy-efficient chipsets, and collaborating across industries to promote sustainable practices.

• There are two key questions around sustainability for tech companies in the AI era. The first is how to improve or even maintain energy efficiency given the vast requirements of 5G networks and AI processors. The second is how to balance sustainability (for example, by increasing device durability) with business growth (for example, through the sale of more devices).

• Qualcomm has a good answer to the first: 5G is more efficient than 4G, and combined with AI, it can bring about efficiency improvements in other sectors such as agriculture, manufacturing and connected vehicles, not just the mobile space. As for balancing sustainability versus growth, this is much more of a challenge, but diversification into new markets like automotive and IoT can help.

• To become truly sustainable, companies need to ingrain their eco targets into their business KPIs and not just a part of marketing or CSR/ESG reporting. Qualcomm is doing this better than many other companies, as sustainability appears to be more tightly aligned with the company’s goals and business models.

The recent surge in interest in generative AI highlights the critical role that AI will play in future wireless systems. With the transition to 5G, wireless systems have become increasingly complex and more challenging to manage. In particular, the heterogenous nature of 5G networks comprising multiple access networks, frequency bands and cells, all with overlapping coverage areas, presents operators with network planning and deployment challenges. This is forcing the wireless industry to think beyond traditional rules-based design methods and turn to AI and ML.

5G Advanced is set to expand the role of wireless AI across 5G networks introducing new, innovative AI applications that will enhance the design and operation of networks and devices over the next three to five years, particularly those demanding high data rates, low latency or massive connectivity such as Extended Reality (XR), Reduced Capex (RedCap), Non-Terrestrial Network (NTN), Unmanned Aerial Vehicles (UAV) as well as applications requiring precise positioning and synchronization.

This Technology Report provides an overview of the role of AI/ML in the 3GPP’s upcoming 5G Advanced standard and outlines the key technologies and use cases where it will be used.

Key Takeaway No. 1: AI will be transformative

Although the application of AI/ML is still in its infancy, its integration into 5G-Advanced networks signifies a transformative shift in the telecommunications market. This development promises not only improved network performance but also opens the door to a wide range of innovative use cases. As a result, the commercial launch of 5G-Advanced in 2025 should accelerate the monetization of 5G for operators.

Key Takeaway No. 2: A Bridge to 6G

The adoption of AI/ML in 5G Advanced provides a platform to experiment with new techniques and should be regarded as a trial for the full introduction of AI/ML in future 6G networks. For example, 6G will be the first opportunity where AI/ML-based optimization will be used in the fundamental design of an air interface from the very beginning. However, the impact of AI/ML will not only enable improved 5G/6G performance, it should also allow 5G-Advanced to evolve faster.

Analysing The Role of AI/ML in 5G Advanced

The full version of this insight report, including a complete set of Key Takeaways is published in the following report, available to clients of Counterpoint Research’s 5G Network Infrastructure Service (5GNI).

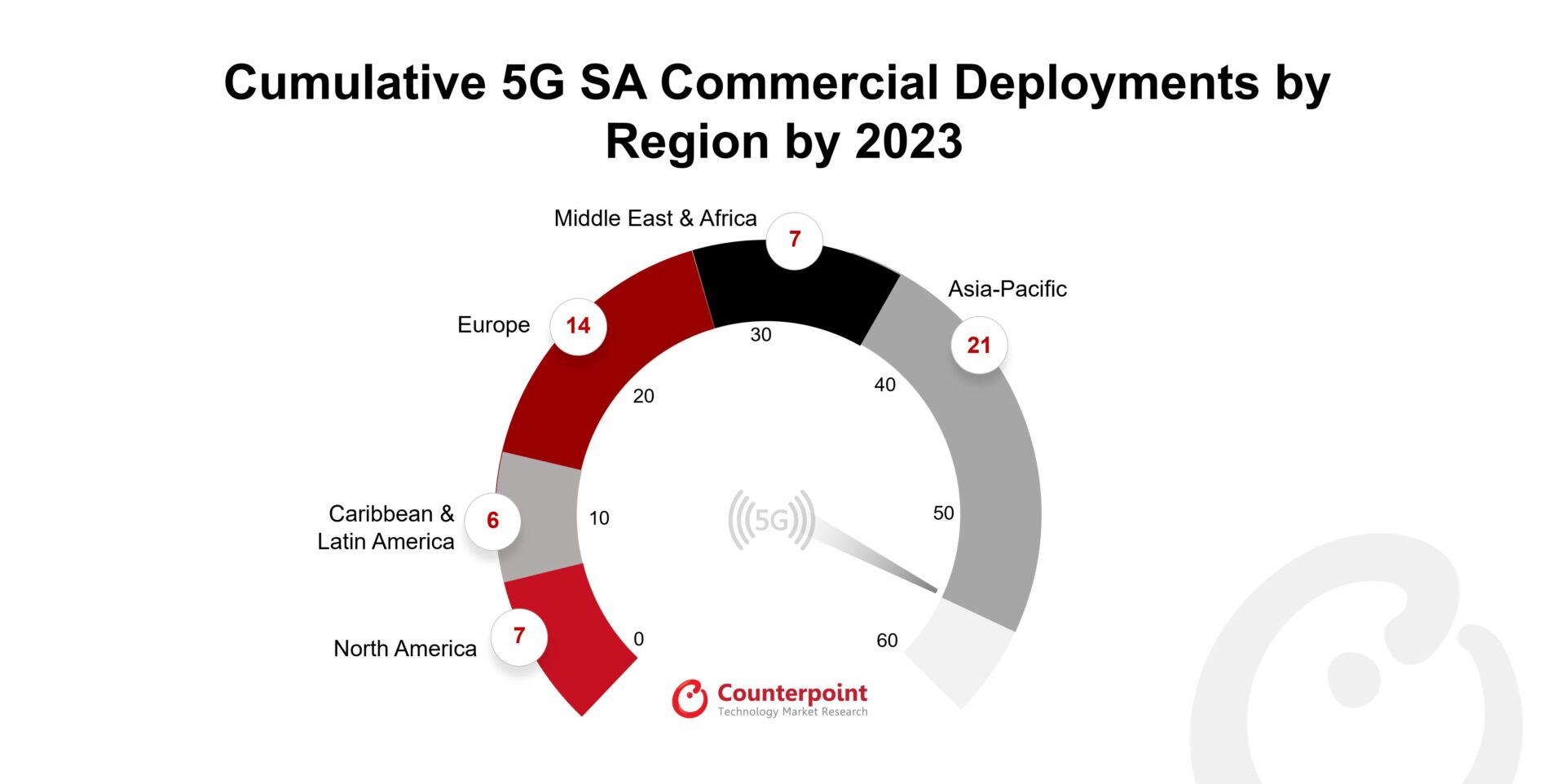

Operator migrations to 5G SA remained low in 2023, despite more than 60 operators investing.

Asia-Pacific continued to lead the deployment charts, while Europe gained momentum.

Total number of deployments between 2020 and 2023 reached 55.

Key deals in leading markets helped Ericsson maintain top spot, followed by Nokia, Huawei and ZTE.

Seoul, Beijing, Boston, Buenos Aires, Fort Collins, Hong Kong, London, New Delhi – February 29, 2024

The number of mobile operators transitioning to a dedicated 5G core decreased to 12 in 2023. Although numerous operators have been running 5G SA core pilots, they have yet to move forward with the transition because they believe the existing architecture is sufficient to meet the current network demand. Another reason for the staggered deployment is the prevailing macroeconomic headwinds and lack of monetization opportunities with 5G.

The transition should increase following the introduction of 5G Advanced starting in 2025, which promises a plethora of new features that will help improve device and network capabilities, lower OPEX costs and introduce new use cases. However, operators need to urgently prioritize the deployment of 5G SA cores to maximize the potential offered by 5G Advanced.

The delay in turning on 5G SA implies that we might see a bunch of rollouts in a shorter time starting H2 2024 and running into 2025, rather than steady rollouts spread out across the next three to four years.

The gradual penetration of 5G SA into Tier-2 operators and nations with smaller geographic areas appears to have begun as MNOs seek to improve user experience. According to Counterpoint Research, about 30 nations have at least one operator running a 5G SA network commercially. Counterpoint Research forecasts that transitions in H1 2024 will remain sluggish before gaining momentum in H2 2024, which will continue into 2025.

Exhibit 1: 5G SA Deployments by Region, by 2023

As indicated in Exhibit 1, the Asia-Pacific region had the highest number of deployments, followed by Europe. North America, Middle East and Africa, and Latin America trailing behind.

Key Points

Key points discussed in the report include:

Operators – 55 operators have commercially implemented 5G SA, with many more in the testing and trial stages. We are seeing a mix of countries adopting 5G Standalone, with some Tier-2 carriers in LATAM launching 5G SA services. The rate of deployment was slightly faster in H2 2023, with some important Tier-1 operators in developed nations shifting to 5G SA, although the list of MNOs currently in the trial phase is still quite extensive.

Vendors – Ericsson’s role as a leader in 5G SA is expanding, and the Swedish company has the largest market share among all cloud-native core providers. Nokia follows Ericsson in terms of the number of deployments of its 5G core. Both have a considerable number of vendor deals with operators that have not yet been commercialized. South Korea’s Samsung and Japan’s NEC are primarily focused on their respective domestic markets, but they are expanding their reach to Tier-2 operators as the focus shifts to vRAN and Open RAN solutions while emerging vendors Parallel Wireless and Mavenir are collaborating with operators in Europe, the Middle East, and Africa.

Spectrum – Most operators are installing 5G at mid-band frequencies (n78), which give higher speeds and better coverage. Some operators have also started offering commercial services in the mmWave wave n258 bands. FWA and other eMBB are currently the most common use cases, although edge services and network slicing are also gaining traction.

Use Cases – Operators are looking for ways to monetize 5G services, as they are struggling to make the ROI from their investments in 5G. Globally, operators are trying to extract better returns from consumer networks before taking their 5G services deeper into enterprises. Although FWA is a promising application for 5G SA monetization, there are many other use cases that operators can look into to increase their ROI, including network slicing, live broadcasting, XR applications, and private networks.

Report Overview:

Counterpoint Research’s 5G SA Core Tracker, January 2024is a culmination of an extensive study of the 5G SA core market. It provides details of all operators with 5G SA cores in commercial operation at the end of 2023, covering market share by region, vendor, and the most popular deployed frequency bands. Further, the tracker provides details about the 5G SA vendor ecosystem split into two categories – public operator and private network markets and touches on the potential monetization opportunities for telecom operators across different domains and use cases.

Table of Contents:

Overview

Market Update

5G SA Market Deployments

Commercial Deployment by Operators

Network Engagements by Region

Network Engagements by Deployments Status

Leading 5G Core Vendors

Mobile Core Vendor Ecosystem

5G Core Vendors Market Landscape

Outlook

5G Standalone Use Cases – Consumer and Enterprise

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Virtually all commercial open RAN deployments to date have used COTS server hardware based on Intel’s x86-based compute with or without FPGA hardware acceleration. While x86-based platforms are adequate for initial prototyping and low bandwidth deployments without acceleration, they are, however, expensive, power-hungry and highly inefficient for high-traffic, low-latency use cases requiring FPGA acceleration. Hence not the best choice for deployment at scale.

Open RAN’s Massive MIMO Challenge

Solving the massive MIMO performance deficit is one of the key issues inhibiting an industry wide transition to open RAN. This challenge must be resolved before mainstream adoption of massive MIMO radios can occur. However, this will require a new breed of merchant silicon solutions designed specifically to efficiently process real-time, latency-sensitive Layer-1 workloads such as beamforming, channel coding, etc.

In early 2023, a number of vendors demonstrated alternatives to Intel’s x86 platform at MWC in Barcelona based on ASICs, GPUs as well as RISC-V architectures. Late last year, an interesting new contender – LeapFrog Semiconductor – appeared on the market.

LeapFrog’s RISC-V Based Modular, Customizable And First Truly Software Defined Layer-1 Solution

LeapFrog Semiconductor is an early-stage fabless semiconductor company focused solely on developing next-generation Layer-1 silicon and software solutions for the mobile infrastructure and enterprise markets. Founded in 2020, it is funded and staffed by seasoned semiconductor veterans.

The San Diego-based start-up has developed a unique AI-enhanced DSP-based silicon platform based on the RISC-V architecture as well as a Network-on-Chip silicon design. The result is a multi-core, distributed 5G RAN silicon platform, which is modular, customizable and flexible, thus creating the first truly software defined, AI-enhanced RAN solution.

LeapFrog’s DSP Chip

Known as the LeapFrog Processing Unit (LPU), LeapFrog’s DSP core uses a specialized Instruction Set Architecture (ISA) developed in-house that natively supports fine-grain parallelism. This means that Layer-1 computation is broken down into a large number of small tasks, resulting in a high level of parallelism. Together with its programmable NOC architecture which minimises communication and synchronization overheads, LeapFrog’s Layer-1 chip results in several unique benefits:

Power and area efficient design – LeapFrog claims that its SoC is significantly smaller than rival designs and boasts single-digit (<10W) power consumption.

Software-based Layer-1 solutions – LeapFrog’s RU and DU Layer-1 solutions are 100% software-based and are thus fully programmable, with no requirements for hardware-based accelerators.

AI-enhanced L1 chip solution – the LeapFrog chip includes in-line processing of AI and L1 algorithms, which includes AI-based channel estimation and other L1 algorithms. This results in a low-latency chip solution and hence improved RAN system performance.

Tile and chiplet-based silicon design – resulting in a scalable, customizable and modular design which can be optimized for different deployment scenarios. For example, chiplets can be combined to make different functions such as L1, I/O, CPU, etc.

In contrast, many rival open RAN chip designs currently under development are based on coarse-grained parallelism, thus necessitating the use of hardware accelerators or hard IP blocks. These designs are not as scalable as LeapFrog’s solution and offer very little flexibility with respect to changes in the computation logic. As a result, a new chip tape-out would be needed if any architectural or logic changes are required.

LeapFrog Network-on-Chip (LNOC)

LeapFrog has also developed a highly power efficient, programmable LeapFrog Network-on-Chip (LNOC) chip design which connects multiple LPUs to create a multi-core, distributed 5G RAN silicon platform. Leveraging innovations in chiplet and Die2Die (D2D) technologies, this results in a highly scalable, modular and flexible chip design complying with all 5G O-RAN specifications (Exhibit 1).

LeapFrog believes that its LNOC design is currently the only chiplet-based 5G open RAN chip platform with a fully software-based RU and DU L1 solution that can be easily customized to suit different 5G deployment scenarios. In addition, the company claims that its AI-enhanced L1 solution results in 50% to 100% better system performance and 10x lower cost and power compared to existing open RAN RU and DU platforms. Another benefit is that software development and testing can be performed on an FPGA platform, which is then transferred to LeapFrog’s silicon platform. This allows a faster time-to-market compared to alternative designs from other vendors.

Target Markets

LeapFrog is targeting multiple markets with its unique LPU design. Chiplet based productization allows the same platform to scale all the way from small cell, fixed wireless access (FWA) to macro cell RU and DU market with a major focus on massive MIMO networks. Potential customers include small and large 5G infrastructure vendors, greenfield CSPs as well as hyperscalers. The company is also pursuing an IP licensing model for its general-purpose DSP targeting consumer/industrial IoT modems, wireless CPEs/gateways, automotive connectivity/sensor fusion as well as mobile handset modems. The IP is ready on FPGA now and was recently demonstrated at the India Mobile Congress and the RISC-V Summit in 2023. The chip design was tested in H2 2023 and delivery of samples to customers is expected to start in Q2 2024.

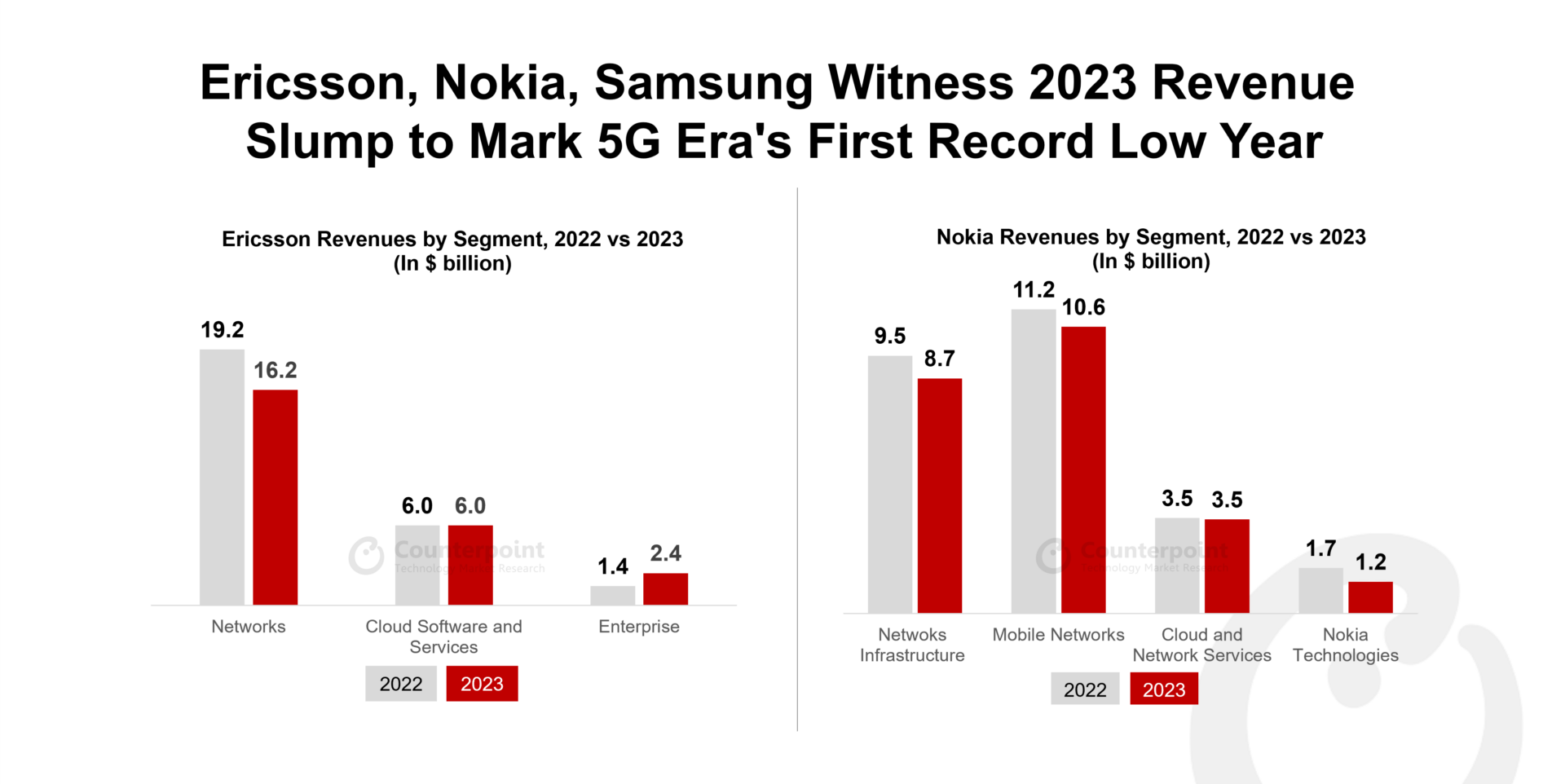

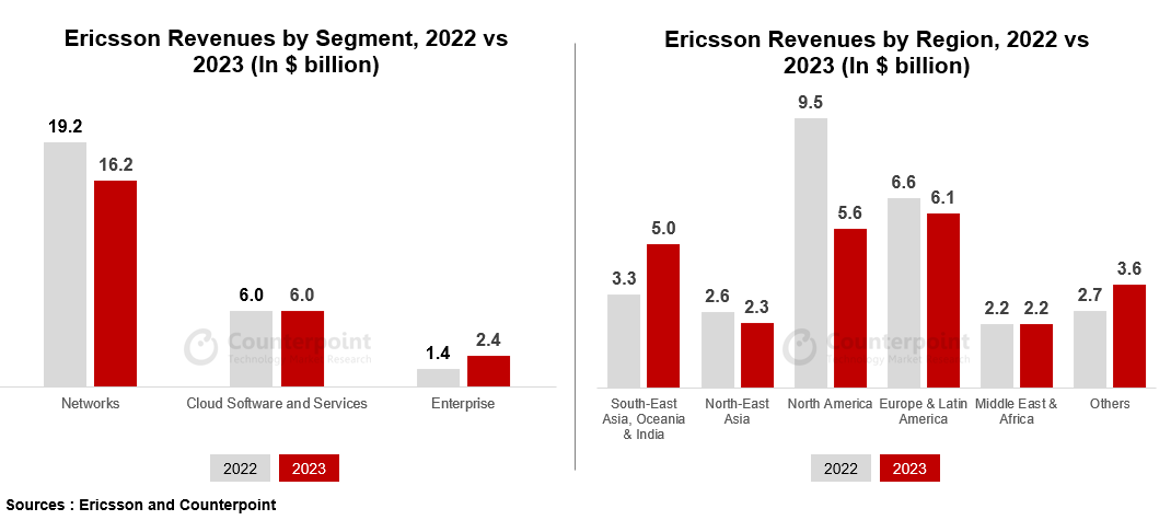

Ericsson, Nokia and Samsung reported a slump in 2023 revenue after hitting a peak in 2022.

Operators worldwide have been judicious in their spending and inventory management.

Uncertainty remains as the industry shows no immediate signs of revival in 2024.

Ericsson, Nokia and Samsung each announced a drop in overall 2023 sales in their earnings calls, citing macroeconomic challenges and a shrinking mobile network infrastructure market, as well as lower spending by operators, particularly in North America.

India was a silver lining for the Nordic vendors, as the unprecedentedly quick rollouts boosted their overall numbers. However, there was a slowdown among Indian operators during Q4 2023, as they plan to normalize their investments in 2024 following a capex-intensive 2023.

In 2023, suppliers made significant strategic decisions to reduce losses caused by external factors and transfer attention back to their core capabilities and cash-generating business sectors.

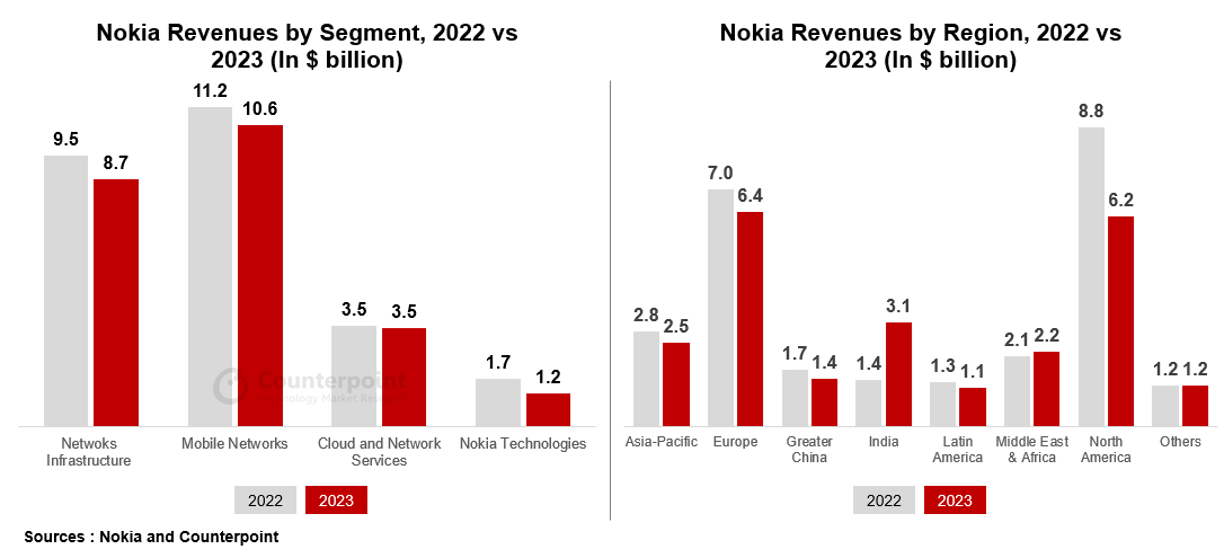

For the year 2023, Ericsson generated nearly $24.8 billion in revenue while its Finnish counterpart Nokia generated $24.1 billion in revenue. Samsung’s network division sales stood at $2.9 billion. Due to the changes in the business mix, its margin remained deflated.

Ericsson

Early adopters of 5G technology saw decreased sales, leading to a reported decline in revenue for Ericsson. MNOs in these areas continued to digest inventory and remained cautious with their spending.

Ericsson maintained its leadership in 5G Standalone deployments. Meanwhile, its cloud and network services business revenue remained unchanged YoY as the increase was offset in part by the decreased managed service revenues because of descoping and contract exits.

Enterprise Wireless Solutions (Cradlepoint) and the newly acquired Global Communication Platform Vonage helped drive growth in the enterprise category. Ericsson’s expansion into Enterprises will continue as it has made investments toward the development of the Global Networks Platform for Network APIs, which is viewed as a critical component in opening new revenue streams for customers.

Nokia

Nokia’s Mobile Network business had aimed for a resilient performance in 2023, despite the uncertain and challenging conditions in the worldwide RAN market. By the end of 2023, gross margin had improved significantly due to a shift in product mix towards software.

Nokia’s Cloud and Network Services business’ net sales were flat for the year but operating profit and margin improved due to digital asset sales and hedging. Nokia ranked second behind Ericsson in terms of the number of 5G Standalone core deployments.

The Network Infrastructure segment too saw revenue declines due to macroeconomic uncertainty and client inventory digestion. There was an increase in order intake in Q4 2023, which will be critical going into 2024. The performance of fixed, IP, and submarine networks deteriorated in 2023, while optical networks experienced small single-digit gains. Nokia anticipates some relief in H2 2024.

In 2023, revenue from enterprise customers increased by about 15% to $2.46 billion, with 151 new clients joining. Momentum in private networks continued with Nokia catering to more than 710 private wireless clients.

Samsung

In 2023, the South Korean technological leader reported $2.9 billion in revenue, down from $4.2 billion a year ago.

Samsung saw similar consequences as its Nordic peers, but it remains optimistic about landing key deals for vRAN and Open RAN networks in 2024. Samsung has been a big player in this area with a few greenfield and brownfield deployments in North America and Japan.

Key Takeaways

2023 was a challenging year for network equipment makers. Operators around the world are exercising extreme prudence and judiciousness when it comes to network expenditure.

The industry also saw a big event at the end of the year, with Ericsson signing a $14 billion deal with AT&T to become the provider of its Open RAN-compliant equipment, effectively reducing Nokia’s market share in the NAM region.

Suppliers are certain that demand will rise and market spending will stabilize as a result of capacity requirements, emerging use-cases, more data traffic, and the integration of more mid-band radios, but the timeline remains uncertain.

Operators and manufacturers are also putting a lot of effort toward enabling 5G Standalone, incorporating Open architecture into their network infrastructure, and monetizing 5G services. Tier-1 MNOs in several countries have risen to prominence as 5G FWA has grown in popularity, but they are yet to capitalize on URLLC or mMTC use cases.

Another significant aspect that has been identified as critical in effectively monetizing 5G networks is the ability to provide users with premium access while also improving their experience through network slicing and enhanced UE Route Selection Policy. However, these are actionable items for the future that will provide results in the long run.

The short-term gains will come from efficient cost reductions and relevant automation that can standardize operations to make them more efficient, continued investments in and divestitures from core competencies, and attempts to capture any new emerging markets that may open as a result of geopolitical sanctions on Chinese vendors.

On the other hand, operators will undoubtedly play a critical role in recovering the RAN market. However, these operators currently show no signs of an early revival in their market forecasts as they wait for the ecosystem to further develop before deploying their infrastructure.

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.